APIs are redefining financial infrastructure. See how they power secure, instant payouts at scale—perfect for settlements, subsidies, and emergency relief.

Why APIs Are the Future of Bulk Payments & Disbursements

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

Every year, billions of dollars are paid out in bulk through lawsuit settlements, insurance claims, disaster relief, and government subsidies. But behind these critical transfers lies an inconvenient truth: most of them still run on outdated, manual systems.

Even in the last few years, despite all the advancements in tech, many people are still filling out forms, waiting for checks in the mail, and wondering if their payment has been “processed yet.” For victims of harm or people in crisis, this is unacceptable. We’ve reached a breaking point, and API-powered financial infrastructure is quietly stepping up as the answer.

According to data by Value Market Research, the API sector is set to grow at a CAGR of 22.55% between 2025 and 2033. In the U.S., as of 2023, 70% of SMEs have adopted API banking. India does lag behind these numbers, but the RBI did note that 2-23 saw a 60% increase in API-based transactions. Today, let’s find out why APIs are the best answer that exists for bulk distributions.

Why Are Manual Disbursements Failing?

Manual disbursement systems have always been slow, but scale and complexity have made them outright dysfunctional. When thousands or even millions of recipients need to be paid, legacy systems struggle to keep up.

Recipients are asked to:

- Submit physical documents.

- Wait for manual verification.

- Deal with poor communication

- Rely on slow, traditional bank transfers or mailed checks.

Each of these steps adds friction, not just in time, but in cost. For organizations, this means more manpower, more paperwork, and more room for error. For recipients, it often feels like being stuck in a system designed to delay rather than deliver.

The cracks are already visible in many areas. In the ongoing lawsuit for Depo Provera, a hormonal birth control injection allegedly linked to brain tumors, there are over 130 cases still pending.

According to TorHoerman Law, if settlements are approved, the disbursements may range from $100,000 to $500,000 per claimant. The logistical challenge of managing such a payout through traditional processes is likely to be cumbersome.

And it’s not just about slowness, because traditional payout processes are also vulnerable. In the 2023 Thomson Reuters privacy lawsuit in California, more than 21 million bot-generated claims were flagged and disqualified. When so much of the process is manual and unprotected, fraud can easily slip through.

In emerging markets like India, the problem becomes even more pronounced. Bank access, digital literacy, and identification issues can make manual disbursement nearly impossible for certain segments.

The result? A system that fails the very people it’s supposed to help. When public trust breaks down in this way, people stop engaging with these systems altogether because the process feels inaccessible or broken.

Why APIs? Well, They are the Missing Link for Fast and Fair Disbursements

Application Programming Interfaces (APIs) might sound technical, but their value is simple. What they enable is the instant and secure communication between different digital systems, such as banks, verification tools, and payment processors.

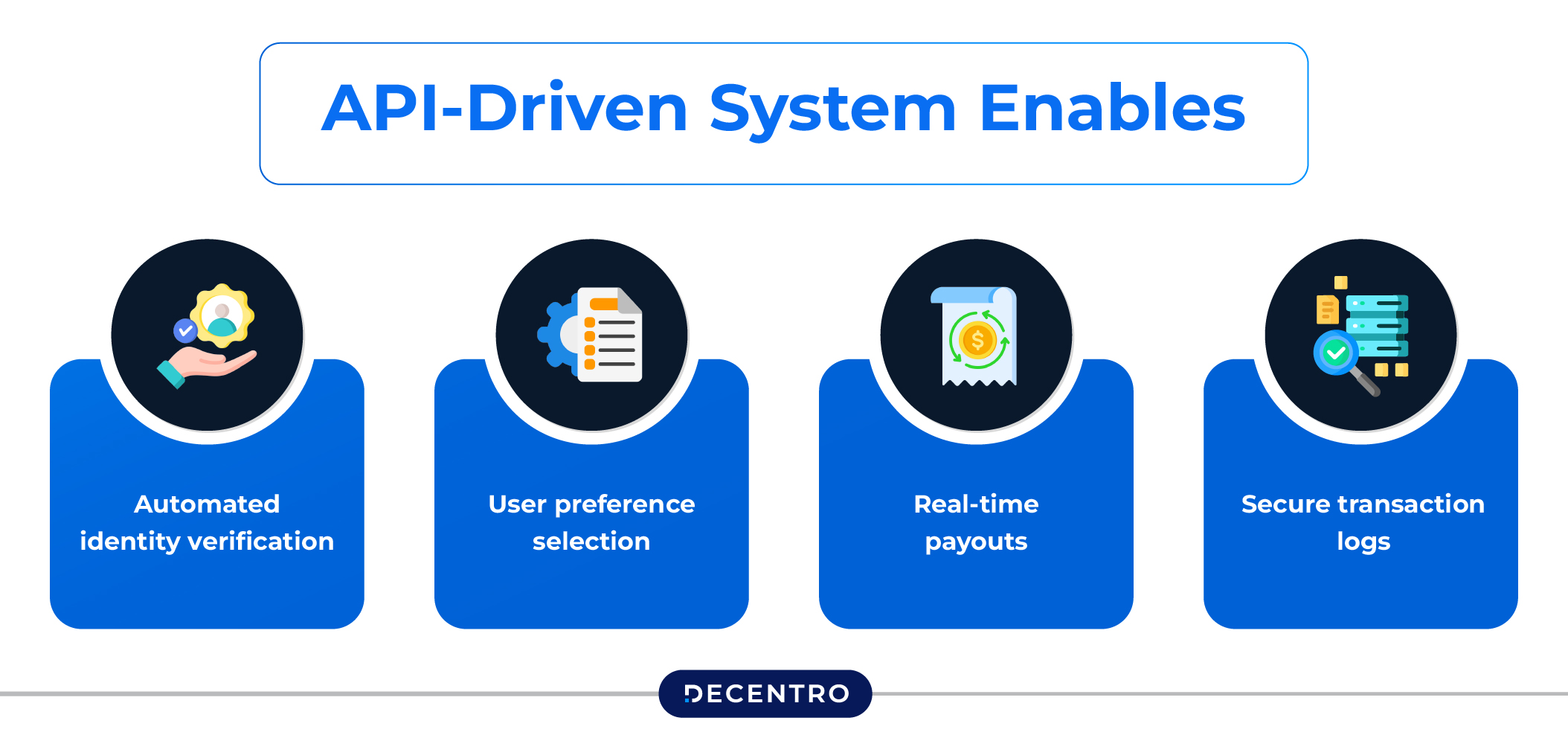

In a bulk payout scenario, here’s what an API-driven system enables:

- Automated identity verification through eKYC (no paperwork)

- User preference selection for receiving funds (bank, UPI, wallet, prepaid card)

- Real-time payouts with full tracking

- Secure transaction logs to reduce fraud and disputes

Decentro makes it incredibly easy to automate disbursements at scale. With plug-and-play APIs, it becomes possible to verify users instantly, disburse funds via Payouts, UPI, or wallets, and track every transaction. All of this is done while staying compliant with financial regulations.

Similarly, Citizens Bank is another great example. In April 2025, they launched an open banking API for their commercial clients. Within weeks, the bank reported a 95% reduction in screen scraping attempts—a major leap in digital security and control.

This kind of model is especially powerful in high-pressure scenarios, like mass torts or disaster relief, where delays can feel like a second injustice.

APIs Also Improve Trust

When people win a settlement or become eligible for relief, they expect dignity and respect, not red tape. Unfortunately, the current system often erodes trust. Victims feel ignored, forgotten, or cheated by a system they already had to fight to access.

An API-based solution changes that. Everything becomes trackable. Payments can be confirmed via mobile. Status updates are transparent. Funds arrive quickly and securely. This is already happening in fintech. Now, it’s time for the legal, insurance, and public systems to catch up.

According to Juniper Research, open banking API calls are projected to hit 137 billion in 2025. What’s more, they are also projected to rise to 722 billion by 2029. This represented a 427% growth, which is massive. This isn’t a tech fad. It’s a financial infrastructure upgrade happening across every major sector.

Governments are exploring APIs for delivering subsidies. Relief organizations are exploring them for emergency aid. Even courts and law firms are testing API-backed systems to distribute class action settlements in a more organized, trackable way.

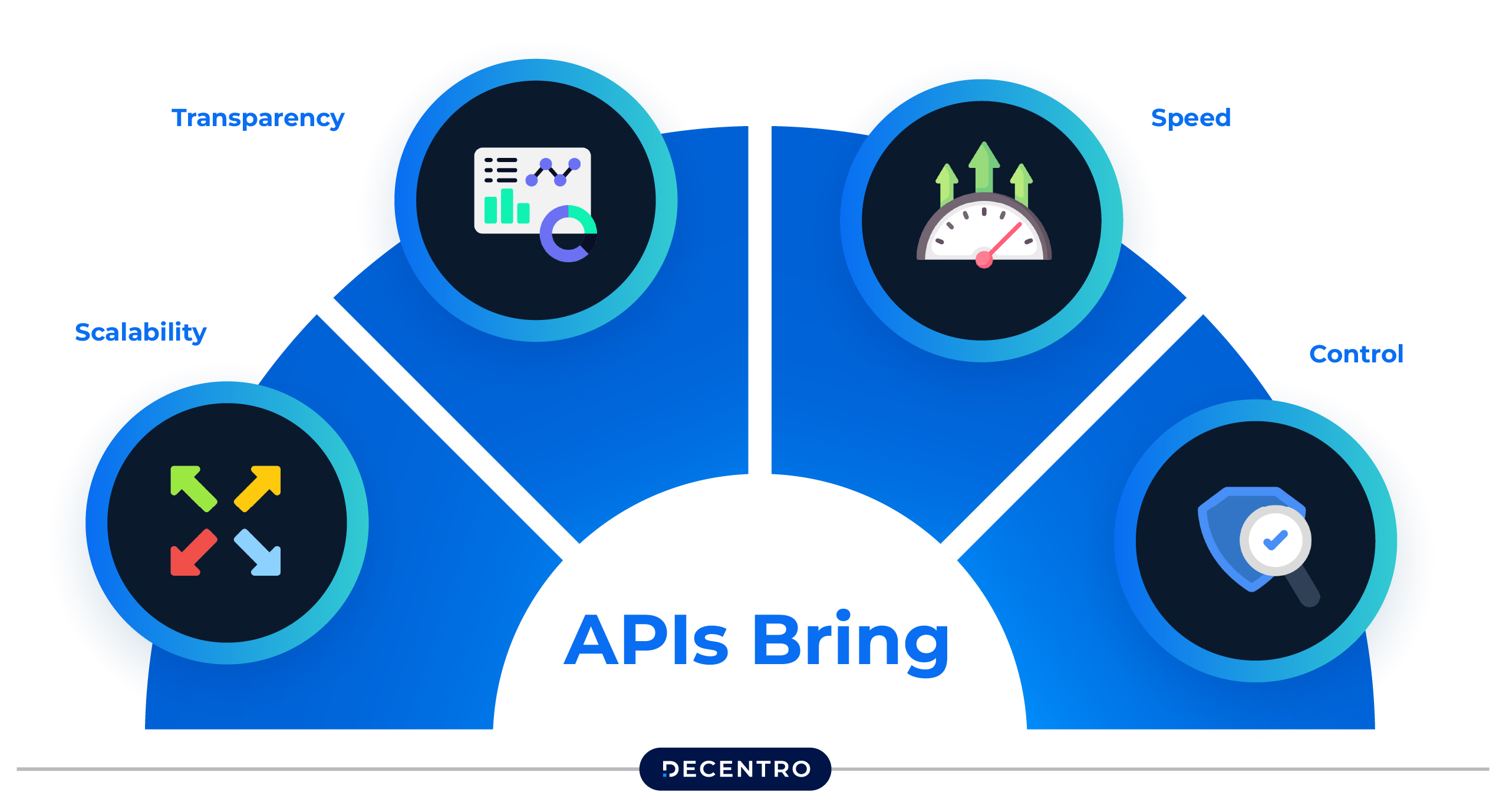

APIs bring:

- Scalability (payouts to 10 or 10 million)

- Transparency (real-time dashboards)

- Speed (payments in hours, not weeks)

- Control (automated auditing and fraud detection)

India’s Direct Benefit Transfer (DBT) system is also increasingly using API integrations with Aadhaar and banking networks to send subsidies directly to citizen accounts. This approach not only reduces leakage and fraud but also improves delivery speed and accountability.

As governments adopt digital infrastructure, the next step is to make these systems more modular and API-first.

This is exactly what modern finance should look like. The point of all of this is that bulk payments really don’t have to be so messy. All it requires is a shift to a more modern and robust process.

Frequently Asked Questions

1. What does API stand for in finance?

API stands for Application Programming Interface. In finance, it’s essentially a digital tool that enables different apps and banking systems to communicate securely, sharing data or triggering actions such as payments without requiring manual intervention.

2. What is an example of a banking API?

A good example is when a budgeting app connects to your bank account to track your spending in real-time. The API allows the app to securely pull your transaction data, so you can see where your money is going, without ever logging into your bank.

3. What is the difference between API and bulk API?

A regular API handles one request at a time, like checking a balance or sending a single payment. A bulk API, on the other hand, is designed to process a large number of requests simultaneously, such as sending payouts to thousands of people in one transaction.

To put it simply, we’ve innovated nearly every corner of finance except the part that matters most to real people in real pain: getting paid. With fintech adoption accelerating globally, we’re standing at the edge of a complete transformation.

The infrastructure is ready, and the demand is real. Now it’s a matter of whether organizations and institutions are ready to retire outdated systems and embrace the tools that will define the next decade of financial services.

Bulk disbursements shouldn’t feel like navigating a broken bureaucracy. Thankfully, with APIs, we finally have the tools to make speed, fairness, and dignity the new standard.

Looking for a stable banking infrastructure to enable seamless disbursements for your business?