Understand how GST on foreign exchange impacts your business in India. Learn about rates, calculation methods, zero-rated exports, and how to optimize your cash flow with modern payment solutions.

GST on Foreign Exchange in India (2026): A Complete Guide

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

Quick Glance

| GST on Forex: 18% GST applies to the service fee for currency conversion, not the money itself—typically just 0.1-0.5% of the total amount Export Services: Zero-rated under GST (0% tax to foreign clients), but you can still claim Input Tax Credit on business expenses LUT is Critical: File Letter of Undertaking (Form RFD-11) annually to avoid paying IGST upfront and waiting months for refunds Calculation Methods: Banks use the RBI reference rate method or the slab-based method per Rule 32 of the CGST Rules Documentation: Maintain FIRCs/FIRAs, export invoices, bank statements, and LUT filings for at least 6 years Common Mistake: Never charge 18% GST to foreign clients—your export invoices should clearly state “Zero-rated supply under GST” |

If you’re running an online business, working as a freelancer, or building a startup that deals with international clients, understanding GST on foreign exchange can save you both money and headaches. Here’s what you need to know upfront: when you receive payments from abroad or convert foreign currency, GST applies to the service fee, not the actual money you receive. Your export services remain zero-rated under GST, meaning you don’t charge tax to foreign clients, but the banks and forex providers do charge 18% GST on their conversion services.

The good news? This GST is calculated on a small service value using government-prescribed methods, making the effective tax rate much lower than you might expect. With India’s cross-border payment market projected to reach $200 billion by 2026 and over 5 million freelancers and exporters navigating these rules, getting this right matters more than ever.

The Cross-Border Payment Landscape in India

India has emerged as a global hub for service exports, digital freelancing, and online businesses. According to recent data, India’s services exports crossed $340 billion in 2024, with software and IT services leading the charge. The freelance economy alone contributes over $20 billion annually, with platforms like Upwork, Fiverr, and direct client relationships driving growth.

For startups and online businesses, this represents a massive opportunity. But with opportunity comes compliance requirements. Every dollar, euro, or pound you receive from abroad needs to be handled correctly under India’s GST framework. The challenge isn’t just understanding the rules—it’s knowing how to apply them efficiently without disrupting your cash flow or operations.

What is GST on Foreign Exchange?

Let’s start with the basics. GST on foreign exchange refers to the Goods and Services Tax applied when you convert one currency to another or when a bank or authorised dealer facilitates your foreign currency transactions. Introduced in 2017 as part of India’s unified tax system, GST replaced the earlier service tax regime that governed forex transactions.

Here’s the critical distinction many business owners miss: GST is not charged on the foreign currency itself. Instead, it’s levied on the service value, the fee charged by banks or forex providers for facilitating the conversion or transaction.

Think of it this way: when your US client sends you $5,000, the money itself isn’t taxed under GST. But when your bank converts that $5,000 to rupees, they charge a service fee for that conversion, and 18% GST applies to that service fee.

A Brief History

Before GST was implemented on July 1, 2017, foreign exchange transactions attracted service tax at varying rates. The system was fragmented, with different states applying different rules, creating compliance nightmares for businesses operating across India.

GST brought uniformity. Under the current framework, foreign exchange services are classified as taxable supplies, with clear rules defined under Rule 32 of the CGST Rules, 2017. This standardisation has made it easier for businesses to understand their tax obligations, though the devil remains in the details.

How GST Works for Export Services

If you’re providing services to clients outside India, whether you’re a developer building apps, a designer creating websites, or a consultant offering expertise, your export transactions receive favourable treatment under GST.

Zero-Rated Supply Status

Export of services qualifies as a zero-rated supply under Section 16 of the IGST Act. This means you charge 0% GST on your invoices to foreign clients. But zero-rated doesn’t mean exempt, it’s actually better. With zero-rated supplies, you can still claim Input Tax Credit (ITC) on GST paid for business expenses like software subscriptions, office rent, or equipment purchases.

To qualify for zero-rated status, your service must meet five conditions:

- The supplier (you) must be located in India

- The recipient (your client) must be located outside India

- The place of supply must be outside India

- Payment must be received in convertible foreign currency

- The supplier and recipient cannot be merely branches of the same legal entity

The Letter of Undertaking (LUT)

Here’s where it gets practical. To export services without paying IGST upfront, you need to file a Letter of Undertaking (Form RFD-11) on the GST portal. This simple document, valid for one financial year, allows you to send zero-rated invoices to clients without blocking your cash flow.

The alternative? You’d have to pay IGST on your export invoices and then claim a refund—a process that can take months and seriously impact working capital. Most businesses file their LUT at the start of each financial year (April) and forget about it until the next renewal.

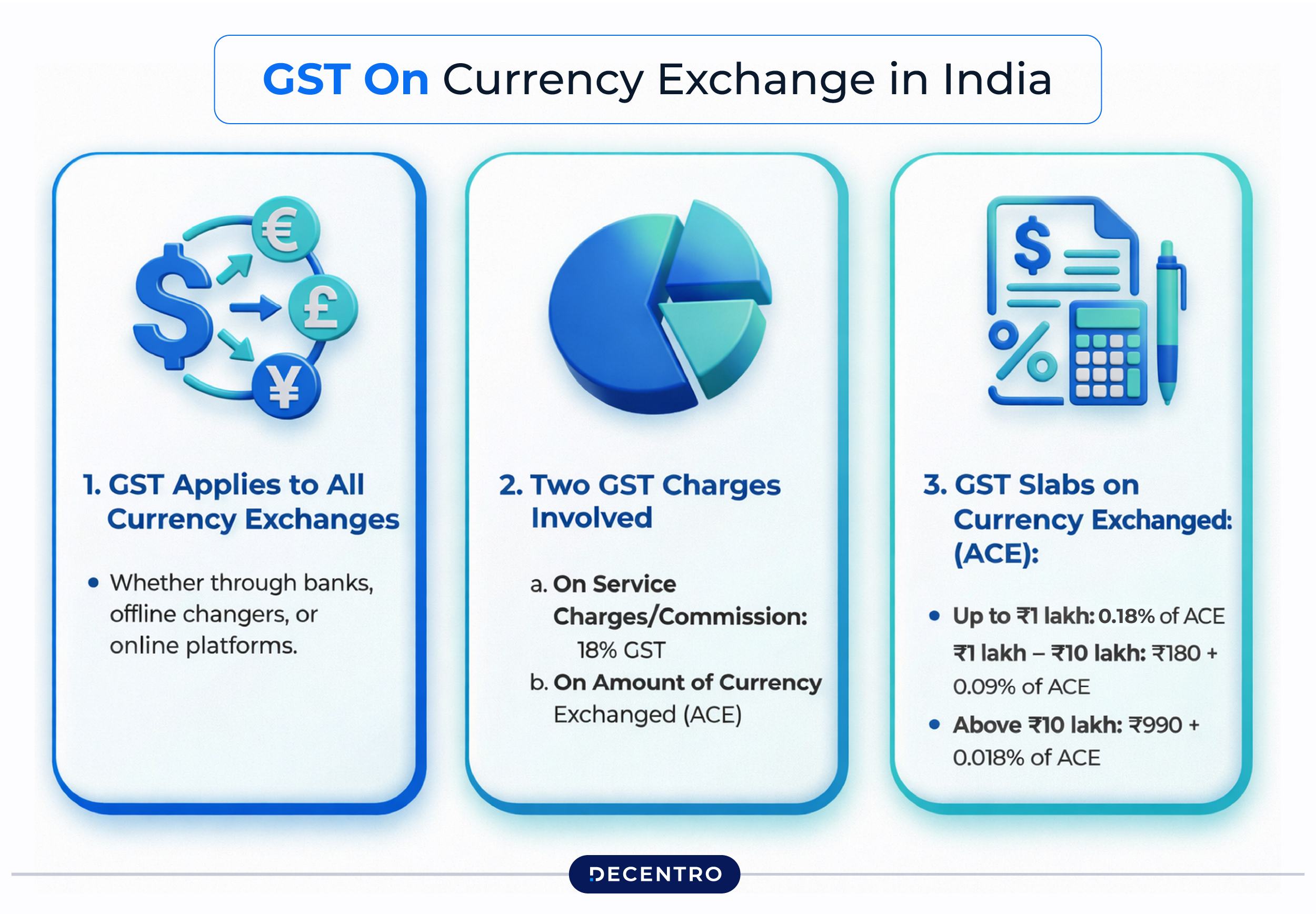

Understanding GST Calculation on Forex Conversions

Now we get to the numbers. When you convert foreign currency to INR, banks and authorised dealers use one of two methods prescribed under Rule 32 of the CGST Rules to calculate the taxable service value.

Method 1: Calculation-Based Method

This method applies when one currency is INR and the RBI publishes a reference rate for the foreign currency.

How it works: The taxable value equals the difference between the transaction rate and the RBI reference rate, multiplied by the amount of currency exchanged.

Example: You receive $10,000 from a client. Your bank offers an exchange rate of ₹84.50 per dollar, while the RBI reference rate for that day is ₹84.00.

- Difference: ₹84.50 – ₹84.00 = ₹0.50

- Service value: ₹0.50 × 10,000 = ₹5,000

- GST at 18%: ₹900

So even though you’re converting $10,000 (₹8,45,000), the GST charged is only ₹900—barely 0.1% of the total amount.

When the RBI rate is unavailable: For currencies where the RBI doesn’t publish rates, the service value is calculated as 1% of the gross INR amount received or paid.

Method 2: Slab-Based Method

This method uses fixed slabs based on the INR value of the transaction:

| Transaction Amount (INR) | Service Value Calculation |

| Up to ₹1,00,000 | 1% of the amount (minimum ₹250) |

| ₹1,00,001 to ₹10,00,000 | ₹1,000 + 0.5% of amount above ₹1 lakh |

| Above ₹10,00,000 | ₹5,500 + 0.1% of amount above ₹10 lakh (max ₹60,000) |

Example: You convert ₹5,00,000 worth of foreign currency.

- Service value: ₹1,000 + (0.5% of ₹4,00,000)

- Service value: ₹1,000 + ₹2,000 = ₹3,000

- GST at 18%: ₹540

Banks must choose one method and stick with it for the entire financial year, ensuring consistency in how they calculate your charges.

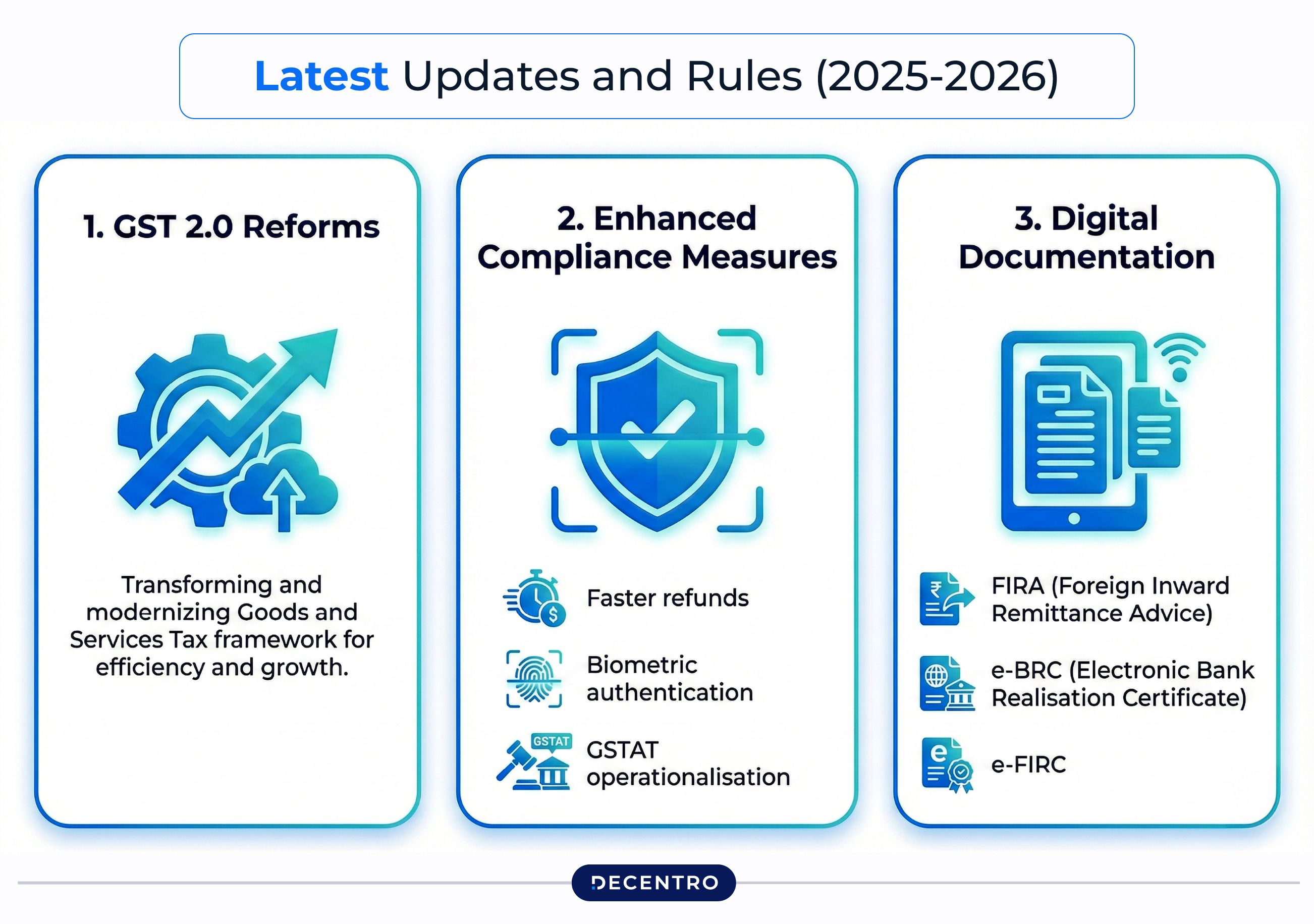

Latest Updates and Rules (2025-2026)

The GST landscape continues to evolve. While the core structure for foreign exchange transactions remains stable, 2025 has brought significant reforms to the broader GST system.

GST 2.0 Reforms

In September 2025, India launched its most significant GST reform since 2017. The 56th GST Council meeting simplified the tax structure from four slabs (5%, 12%, 18%, 28%) to primarily two slabs (5% and 18%), with a new 40% rate for luxury and sin goods.

What this means for you: While foreign exchange services continue to attract 18% GST, the overall simplification makes compliance easier. With fewer slabs to manage, businesses can focus on core operations rather than wrestling with classification disputes.

Enhanced Compliance Measures

Starting in 2025, several compliance improvements rolled out:

- Faster refunds: Eligible businesses now receive 90% of claimed refunds as provisional refunds, subject to system-driven risk evaluation

- Biometric authentication: Company directors must complete biometric verification at GST Suvidha Kendras for new registrations

- GSTAT operationalisation: The GST Appellate Tribunal provides faster dispute resolution, with hearings set to commence by December 2025

Digital Documentation

The shift toward digital documentation accelerated in recent years. Physical FIRCs (Foreign Inward Remittance Certificates) have largely been replaced by:

- FIRA (Foreign Inward Remittance Advice): Digital proof of receiving foreign payments

- e-BRC (Electronic Bank Realisation Certificate): Available through the DGFT portal, linking payments to specific export invoices

- e-FIRC: Digital certificates issued by banks for inward remittances

These documents serve as crucial proof when claiming GST refunds or demonstrating compliance during audits.

Why This Matters for Your Business

Understanding GST on foreign exchange isn’t just about compliance—it’s about protecting your bottom line and maintaining healthy cash flow.

Cost Implications

Every forex transaction carries a GST component. While the effective rate is small (typically 0.1% to 0.5% of the converted amount), these costs add up. If you’re processing $50,000 in monthly receipts, you could be paying ₹3,000-₹5,000 in forex-related GST charges.

Knowing how these charges are calculated helps you:

- Compare forex providers accurately

- Budget for transaction costs

- Negotiate better rates with your bank

- Choose the right payment channels

Compliance and Audits

GST authorities can scrutinise your export claims during audits. Without proper documentation, invoices marked as zero-rated, FIRCs/FIRAs, bank statements, and LUT filings, you risk:

- Delayed refunds on input tax credits

- Penalties for non-compliance (₹25,000 per return)

- Interest charges on disputed amounts

- Blocked working capital

The compliance burden might seem heavy, but it’s manageable with the right systems in place.

Cash Flow Management

Here’s where many businesses trip up: paying IGST upfront instead of filing an LUT. The cash flow impact can be devastating, especially for growing businesses operating on tight margins.

The Math That Matters

If you export ₹10 lakh worth of services monthly without an LUT:

Annual Impact:

- Total IGST paid upfront: ₹21,60,000

- Average capital blocked at any time: ₹8,10,000 (4.5 months in refund pipeline)

- Refund processing time: 3-6 months minimum

That’s over ₹21 lakh annually that could fund growth, hire talent, or invest in marketing—instead stuck in the refund processing pipeline.

Real-World Example: SaaS Startup’s Cash Crunch

Rahul runs a B2B SaaS company earning ₹15 lakh monthly from US and European clients. He didn’t file an LUT, assuming refunds would come quickly.

Month 1 Impact:

- Revenue received: ₹15,00,000

- IGST paid upfront: ₹2,70,000

- Net cash available: ₹12,30,000

- Planned buffer: ₹2,80,000

- Actual buffer: ₹80,000

Result: One unexpected expense (critical bug fix, server outage) puts him in the red.

Month 6 Compounding:

- Total IGST blocked: ₹16,20,000

- Growth plans requiring ₹11.5 lakh (sales hire, conference, ad campaign)

- Available reserves: ₹2,50,000

Forced to:

- Delay sales hire by 2 months

- Skip industry conference (lost networking opportunities)

- Cut ad budget by 60%

Year End:

- Total IGST paid: ₹32,40,000

- Still in refund pipeline: ₹18,00,000

- Opportunity cost: ₹2,00,000+ in delayed payments and missed growth

Working Capital Impact Breakdown

1. Cash Conversion Cycle

Without LUT: 210-270 days (includes 3-6 month refund wait) With LUT: 30 days (standard payment terms only)

Difference: 180-240 extra days your money is unavailable.

2. Borrowing Capacity

Banks don’t count pending GST refunds as available assets.

Example Impact:

- Without LUT: ₹8L available → ₹5.6L max loan (70% of cash)

- With LUT: ₹24L available → ₹16.8L max loan

3× higher borrowing capacity just by filing an LUT.

3. Growth Investment Lost

Digital agency billing ₹8 lakh/month loses ₹17.28 lakh annually to blocked IGST.

What ₹17.28 lakh could fund:

- 2 junior developers (6 months): ₹7,20,000

- Premium tools and software: ₹1,20,000

- Client acquisition campaign: ₹6,00,000

- Conference + networking: ₹1,50,000

- Emergency reserves: ₹1,38,000

4. Vendor Payment Chain Reaction

Cash constraints trigger cascading failures:

- Late AWS payments → service interruption risk

- Delayed freelancer dues → talent refuses future work

- Skipped SaaS subscriptions → productivity drops

- Salary delays → employee attrition

Calculate Your Impact:

Monthly Working Capital Blocked = Monthly Export Revenue × 0.18 Average Capital Stuck = Monthly IGST × 4.5 months

For ₹10 lakh monthly exports:

- Monthly IGST: ₹1,80,000

- Average blocked: ₹8,10,000

The 10-Minute Solution: File Your LUT

Simple Steps:

- Log into GST portal

- Navigate to Services > Furnish Letter of Undertaking

- Fill Form RFD-11 (basic details, export estimate)

- Upload signed LUT on letterhead

- Submit

Common Mistakes to Avoid

After working with hundreds of businesses, we’ve seen these errors repeatedly:

1. Charging GST to Foreign Clients

Many freelancers and startups mistakenly add 18% GST to invoices for international clients. This is wrong. Export services are zero-rated. Your invoice should clearly state “Export of Service , GST not applicable (Zero-rated under IGST).”

2. Skipping the LUT Filing

Forgetting to file your LUT means paying IGST upfront on every export invoice. File it in April, mark your calendar for next year, and save yourself the cash flow headache.

3. Poor Documentation

Not maintaining proper records of forex transactions, FIRCs, and bank statements creates problems during audits. Keep organised files, digital copies work best, for at least 6 years.

4. Using Unauthorised Channels

Some businesses use informal channels or non-RBI-authorised platforms to save on fees. This not only violates FEMA regulations but also means you can’t claim legitimate GST refunds because you lack proper documentation.

5. Not Reporting Zero-Rated Exports

Zero-rated doesn’t mean unreported. You must still declare your export income in GSTR-1 (Table 6A) and GSTR-3B, even though the tax rate is 0%.

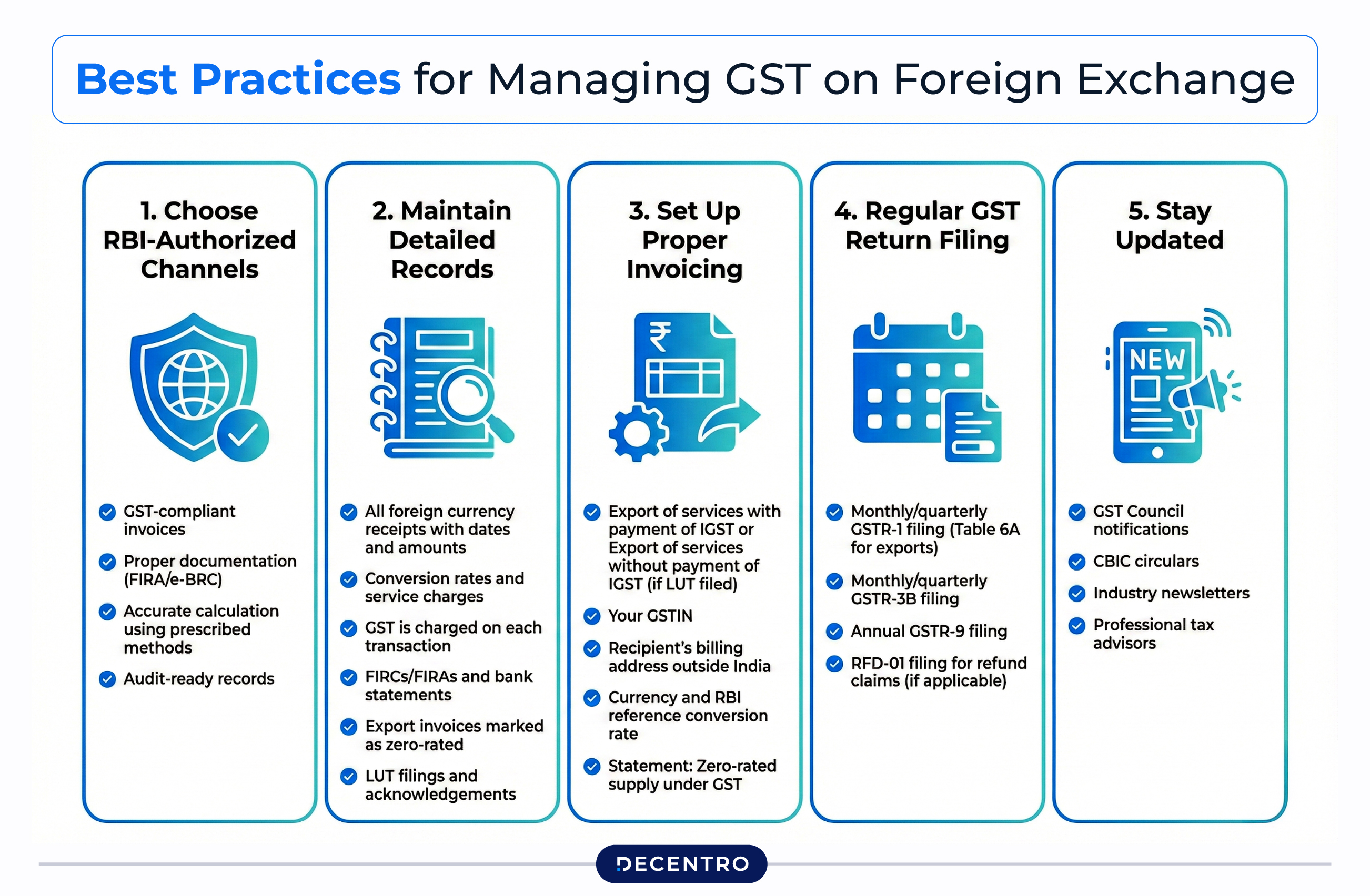

Best Practices for Managing GST on Foreign Exchange

Here’s how successful businesses handle forex-related GST compliance:

Choose RBI-Authorized Channels

Always use RBI-authorised banks or payment aggregators. They provide:

- GST-compliant invoices

- Proper documentation (FIRA/e-BRC)

- Accurate calculation using prescribed methods

- Audit-ready records

Maintain Detailed Records

Create a system for tracking:

- All foreign currency receipts with dates and amounts

- Conversion rates and service charges

- GST is charged on each transaction

- FIRCs/FIRAs and bank statements

- Export invoices marked as zero-rated

- LUT filings and acknowledgements

Set Up Proper Invoicing

Your export invoices should include:

- “Export of services with payment of IGST” or “Export of services without payment ofIGST” (if LUT filed)

- Your GSTIN

- Recipient’s billing address outside India

- Currency and RBI reference conversion rate

- Statement: “Zero-rated supply under GST”

Regular GST Return Filing

Even zero-rated exports require reporting:

- Monthly/quarterly GSTR-1 filing (Table 6A for exports)

- Monthly/quarterly GSTR-3B filing

- Annual GSTR-9 filing

- RFD-01 filing for refund claims (if applicable)

Stay Updated

GST rules evolve. Subscribe to updates from:

- GST Council notifications

- CBIC circulars

- Industry newsletters

- Professional tax advisors

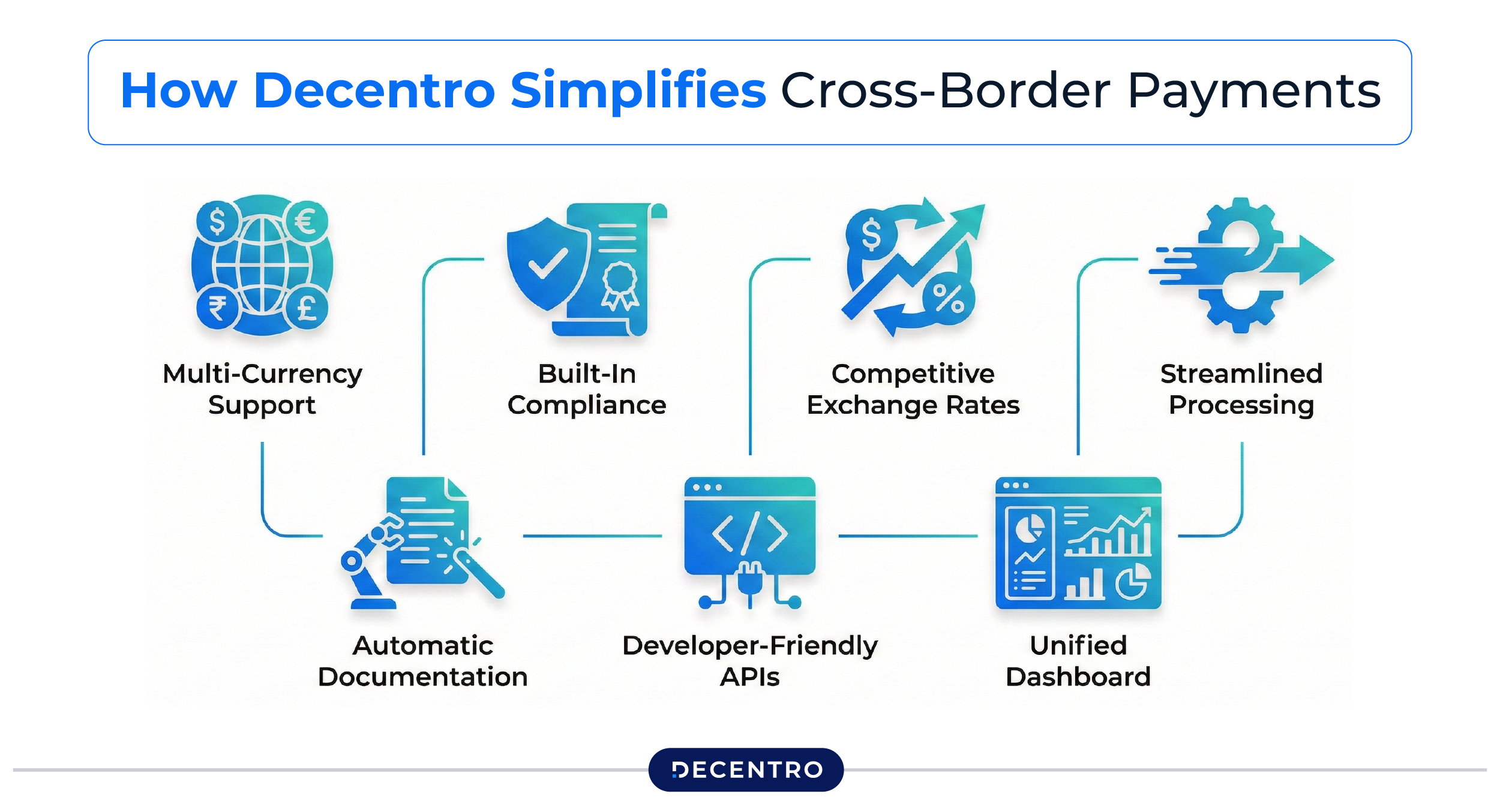

Simplifying Cross-Border Payments with Modern Solutions

Managing GST compliance, forex conversions, and international payments doesn’t have to be complicated. Modern fintech platforms are transforming how Indian businesses handle cross-border transactions.

What to Look for in a Payment Solution

When choosing a platform for receiving international payments, consider:

- Transparent pricing: Clear breakdown of forex rates, service fees, and GST charges

- Automatic documentation: Digital FIRCs/FIRAs generated automatically

- Competitive rates: Better than traditional banks, with savings of 2-4% on conversion

- Fast settlements: T+1 or T+2 settlement in INR to your Indian bank account

- Compliance support: GST-compliant invoicing and reporting

- Multi-currency support: Ability to accept payments in various currencies

The Decentro Advantage

This is where solutions like Decentro’s cross-border payment functionality make a real difference. Built specifically for Indian businesses dealing with international transactions, Decentro offers:

Seamless Cross-Border Collections: Accept payments from clients worldwide with automatic conversion to INR, eliminating the need to manage foreign currency accounts.

Competitive Rates: Exchange rates that are significantly better than traditional banking channels, helping you retain more of your hard-earned revenue.

Developer-Friendly Integration: APIs that integrate with your existing systems, whether you’re running an e-commerce platform, SaaS business, or freelance marketplace.

For startups and online businesses scaling globally, having a reliable cross-border payment infrastructure isn’t optional; it’s essential. The right platform handles the complexity of GST compliance while you focus on growing your business.

Conclusion

GST on foreign exchange might seem complex at first glance, but it boils down to a few key principles: export services are zero-rated, forex conversion services attract 18% GST on the service value (not the full amount), and proper documentation is non-negotiable.

As India’s cross-border economy continues to grow, with services exports projected to reach $500 billion by 2030, getting your GST compliance right becomes increasingly important. The reforms of 2025 have simplified the broader GST structure, making compliance easier while maintaining the favourable treatment of exports.

The businesses that thrive in this environment are those that:

- File their LUT on time every year

- Maintain meticulous records of all forex transactions

- Use RBI-authorised channels for currency conversion

- Mark export invoices correctly as zero-rated supplies

- Choose modern payment platforms that handle compliance automatically

Remember, GST on foreign exchange isn’t a burden, it’s a small cost for participating in the global economy. With the right understanding and tools, you can navigate these requirements efficiently while focusing on what really matters: building great products, serving clients worldwide, and growing your business.

Whether you’re a solo freelancer receiving your first international payment or a scaling startup processing millions in cross-border transactions, understanding GST on foreign exchange empowers you to make informed decisions, avoid costly mistakes, and keep more of your revenue where it belongs, in your business.

Looking to streamline your cross-border payments while staying GST-compliant?

Frequently Asked Questions

1. Do I need to charge GST to my international clients?

No. Export of services is zero-rated under Section 16 of the IGST Act, meaning you charge 0% GST to foreign clients. Your invoice should clearly state “Export of services – Zero-rated supply under GST” or “Export of services without payment of IGST under LUT”. Never add 18% GST to international invoices—this is one of the most common and costly mistakes.

2. Is the LUT valid for multiple clients and transactions?

Yes. A single LUT covers all your export transactions for the entire financial year (April to March), regardless of the number of clients or transaction volume. You don’t need separate LUTs for each client or invoice. Just file Form RFD-11 once at the start of the financial year and you’re covered until March 31st. Remember to renew it every April.

3. What’s the difference between zero-rated and exempt supplies?

Both result in 0% GST to customers, but they’re fundamentally different for your business. Zero-rated (exports): you can claim Input Tax Credit (ITC) on business expenses like software, equipment, and rent. Exempt (like education or healthcare): you cannot claim ITC. For exporters, zero-rated status is far more beneficial as it allows you to recover GST paid on inputs, improving your margins.

4. How is GST calculated on forex conversion, and can I negotiate it?

GST is calculated on the service value using Rule 32 methods: either the spread between bank rate and RBI reference rate, or a slab-based formula (1% up to ₹1L, 0.5% from ₹1L-₹10L, 0.1% above ₹10L with ₹60K cap). The GST itself (18%) is non-negotiable, but you can choose forex providers with better exchange rates and lower spreads. Digital payment platforms often offer rates 2-4% better than traditional banks, reducing the base on which GST applies.

5. What documents do I need for GST compliance on foreign payments?

Essential documents include: FIRA/e-FIRC (proof of foreign receipt), export invoices marked zero-rated, bank statements showing forex conversion, LUT filing acknowledgment (Form RFD-11), GST returns (GSTR-1 Table 6A showing exports, GSTR-3B), and contracts/purchase orders from foreign clients. Keep all documents for minimum 6 years. Digital copies are acceptable and recommended for easier retrieval during audits or refund claims.