Explore the 15 best vehicle financing platforms in India for 2026. Compare NBFCs, banks, and fintech lenders for cars, EVs, and commercial vehicles.

15 Best Vehicle Financing Platforms in 2026

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

India’s auto loan market is on a serious tear. Valued at USD 46.33 billion in 2026 and projected to hit USD 63.82 billion by 2031, the vehicle financing space has evolved far beyond the branch-visit-and-paperwork era. Today, it is powered by AI-driven underwriting, Aadhaar-based e-KYC, co-lending partnerships, and mobile-first platforms that can disburse loans in under 24 hours.

Whether you’re a consumer looking to buy your first hatchback, a fleet operator financing 50 electric three-wheelers, or a fintech company building lending infrastructure, choosing the right vehicle financing platform can make all the difference. NBFCs, banks, and fintech startups are each carving out distinct niches — and the competition has never been more fierce.

This guide rounds up the 15 best vehicle financing platforms in 2026, with a strong focus on Indian players who are reshaping how the country buys, sells, and finances vehicles.

Quick Glance

| S.No | Platform | Best For |

|---|---|---|

| 1 | Rupyy (CarDekho) | End-to-end digital used car & EV financing |

| 2 | CARS24 Financial Services | Pre-owned vehicle loans with AI pricing |

| 3 | Shriram Finance | Commercial & used vehicle financing at scale |

| 4 | Mahindra Finance | Rural & semi-urban vehicle credit |

| 5 | Cholamandalam Investment & Finance | Commercial vehicles & new car loans |

| 6 | Tata Capital (Motor Finance) | Full-spectrum vehicle lending |

| 7 | Bajaj Finance (Auto) | Consumer & EV vehicle financing |

| 8 | Hero FinCorp | Two-wheeler & used car loans |

| 9 | RevFin | EV financing for commercial fleets |

| 10 | Kuwy Technology Service | Automated dealership lending |

| 11 | Sundaram Finance | South India-dominant vehicle finance |

| 12 | HDFC Bank (Vehicle Loans) | Bank-backed vehicle loans at competitive rates |

| 13 | TVS Credit Services | Two & three-wheeler financing |

| 14 | CarWale Finance | Loan comparison & multi-lender marketplace |

| 15 | Droom Credit | Digital-first used car financing |

Rupyy (CarDekho Group)

Founded: 2022 (financial services arm active since 2016)

Headquarters: Gurugram, India

Rupyy is the digital lending arm of CarDekho Group — one of India’s leading automotive unicorns. Built specifically to democratize vehicle financing, Rupyy covers new cars, used cars, two-wheelers, EVs, and loans against cars. It partners with more than 37 lenders including HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra, and YES Bank — and its dealer network reaches 90% of India’s pin codes.

As of mid-2023, Rupyy clocked an annualised loan disbursement run rate of INR 12,000 crore with 88% year-on-year revenue growth. It commands a 15% market share in the pre-owned vehicle loan segment, making it one of the most dominant digital vehicle financing platforms in the country.

Top Features

- End-to-end digital loan journey from application to disbursement

- 37+ lending partners covering banks, NBFCs, and Rupyy’s own NBFC book

- Pan-India distribution across 1,500+ locations and 9,000+ distributor touchpoints

- EV financing partnerships with Hero Electric, Ampere, Tork, Pure EV, and others

- Loan-against-car and personal loan products for broader financial inclusion

- Proprietary credit underwriting for thin-file and non-metro borrowers

Pros

- Deepest distribution network among digital auto-lending platforms

- Covers new, used, two-wheeler, and EV financing under one roof

- Real-time loan quotes from multiple lenders enable competitive comparisons

- Strong Tier II and Tier III city penetration

Cons

- Primarily a marketplace; borrowers may receive varying rates based on lender

- EV financing portfolio still maturing compared to used car stronghold

Market Share

~15% in pre-owned vehicle loans; targeting 10% share in EV two-wheeler financing over the next 5 years.

CARS24 Financial Services

Founded: 2015 (NBFC arm launched subsequently)

Headquarters: Gurugram, India

CARS24 is one of India’s most recognized auto-tech companies, spanning used car buying, selling, and financing. Its NBFC arm — CARS24 Financial Services Private Limited — is registered with the Reserve Bank of India and processes loans using a Smart AI Pricing Engine alongside 140 vehicle quality checks. Operating in India, UAE, Australia, and Thailand, CARS24 brings end-to-end transparency to used car transactions.

Top Features

- AI Pricing Engine combined with 140-point vehicle quality inspection

- RBI-registered NBFC ensures regulatory credibility

- Integrated buy-sell-finance platform eliminates third-party dependencies

- Doorstep car evaluation and same-day loan disbursement in metro cities

- Digital loan origination with minimal physical documentation

Pros

- Fully integrated used car ecosystem — inspect, buy, sell, and finance in one place

- Strong consumer trust built on transparent pricing and quality checks

- International presence gives it scale advantages

Cons

- Financing primarily restricted to pre-owned cars transacted within the CARS24 ecosystem

- Interest rates may be higher for borrowers with lower credit profiles

Shriram Finance

Founded: 1974 (as Shriram Transport Finance; merged and rebranded 2023)

Headquarters: Chennai, India

Shriram Finance is India’s largest retail NBFC by assets under management in the vehicle financing segment. After the landmark merger of Shriram Transport Finance, Shriram City Union Finance, and Shriram Capital in 2023, the entity crossed INR 2.5 trillion (₹2.5 lakh crore) in AUM, cementing its dominance in commercial vehicle (CV) and used vehicle finance. In January 2025, Montra Electric partnered with Shriram Finance for customised EV loan products.

Top Features

- Specialises in used commercial vehicle (CV) financing — trucks, buses, and cargo vans

- AUM exceeding ₹2.6 trillion across vehicle, MSME, gold, and tractor loans

- Deep penetration in Tier II, III, and rural markets

- AI-driven risk scoring and digital paperless loan journeys

- EV credit line: USD 150 million ADB facility targeting MSME and EV expansion (March 2025)

Pros

- Unmatched rural and semi-urban presence for commercial vehicle loans

- Post-merger scale enables lower cost of funds

- Consistently strong collection efficiency and portfolio quality

Cons

- Primarily suited for commercial vehicle operators; less competitive for personal passenger car loans

- Gross NPA in mid-tier NBFC vehicle loans can be a watch area

Market Share

Largest NBFC vehicle lender by AUM in India; dominates the used commercial vehicle segment with an estimated 18–20% share in its focused categories.

Mahindra Finance

Founded: 1991

Headquarters: Mumbai, India

Mahindra Finance is the go-to lender for vehicle buyers in rural and semi-urban India. A subsidiary of the Mahindra Group, it reported AUM of INR 1.15 trillion in Q3 FY2025, reflecting 19% year-on-year growth with 95% collection efficiency. It finances passenger cars, SUVs, tractors, commercial vehicles, and — increasingly — electric vehicles. Its ‘Used Car Digi Loans’ platform, launched in partnership with Car&Bike and Rupyy in March 2023, marked a significant digital pivot.

Top Features

- Strong presence in 375,000+ villages across India

- Financing for passenger cars, SUVs, tractors, commercial vehicles, and EVs

- ‘Used Car Digi Loans’ digital platform with instant underwriting

- Quiklyz: digital vehicle leasing and subscription service launched 2021

- EV loan disbursements growing rapidly as Mahindra pivots to EV mobility

Pros

- Unmatched last-mile reach in rural India — a genuine differentiator

- Diversified product mix covering all vehicle types

- Strong government and OEM partnerships

Cons

- Digital infrastructure still catching up with pure-play fintech players

- Rural NPA volatility tied to monsoon cycles and agricultural income

Market Share

AUM of INR 1.15 trillion (Q3 FY25); among the top 3 NBFC vehicle lenders in India.

Cholamandalam Investment and Finance Company (Chola)

Founded: 1978

Headquarters: Chennai, India

Cholamandalam, part of the Murugappa Group, is a leading NBFC with 575 branches and a twin-hub model that pairs centralized risk analytics with district-level loan origination. It covers new and used cars, commercial vehicles (LCV/HCV), and home equity, with an increasingly aggressive push in the used commercial vehicle segment. Chola’s vehicle finance book is one of the most consistently high-quality portfolios among Indian NBFCs.

Top Features

- New and used car loans, LCV/HCV commercial vehicle loans under one platform

- 575 branches and rising — strong geographic coverage

- AI-powered credit underwriting with centralized risk analytics

- 100% financing options on select used vehicles

- Dedicated used car digi-loan platform for faster paperless approvals

Pros

- Proven balance sheet quality and stable collection efficiency

- Competitive interest rates for commercial vehicle operators

- Strong dealer relationships across India

Cons

- Less consumer-facing digital marketing compared to fintech rivals

- Processing times for non-pre-approved customers can lag behind pure-play digital platforms

Market Share

Among the top 5 NBFC vehicle lenders in India, approximately 6–8% of the organised vehicle finance market. Used vehicles accounted for 27%+ of its vehicle finance book in recent years.

Tata Capital (Motor Finance)

Founded: 2007 (Motor Finance division strengthened post May 2025 merger with Tata Motors Finance)

Headquarters: Mumbai, India

Following its landmark IPO in October 2025 and the merger with Tata Motors Finance Ltd (TMFL) in May 2025, Tata Capital has emerged as a full-stack, pan-India vehicle financier. With a total loan book of INR 2.33 lakh crore (as of June 2025), 1,516 branches across 27 states, and 7.3 million customers, it offers car loans, two-wheeler loans, commercial vehicle loans, and construction equipment financing under a single platform. Its Motor Finance segment hit PAT breakeven in Q3 FY26.

Top Features

- Full-spectrum lending: two-wheelers, cars, CVs, and construction equipment

- Tata Group brand synergy for better loan terms with Tata Motors dealer networks

- 1,516 pan-India branches with digital origination capabilities

- Post-TMFL merger: expanded product suite, geography, and supply chain financing

- Digital platforms, including mobile app and web-based lending journeys

Pros

- Tata brand trust and strong corporate governance

- Post-IPO capital structure enables competitive pricing

- Cross-sell opportunities across 7.3 million customers

Cons

- Motor Finance segment only recently reached PAT breakeven — still maturing

- Smaller branch network compared to Bajaj Finance and Shriram Finance

Market Share

Third-largest diversified NBFC in India; vehicle loans form a significant and growing segment of its INR 2.33 lakh crore loan book.

Bajaj Finance (Auto Division)

Founded: 1987

Headquarters: Pune, India

Bajaj Finance is India’s largest and most profitable NBFC, with an AUM of ₹4.44 lakh crore and 4,192 branches. Its auto lending arm covers two-wheeler loans, new and used car loans, and increasingly EV financing — bolstered by a USD 400 million IFC facility earmarked for EV portfolios. Toyota Kirloskar and Honda Cars India both partnered with Bajaj Finance for retail auto financing in 2023, underscoring OEM confidence in its platform.

Top Features

- Largest NBFC by AUM; unmatched scale and pricing power

- Two-wheeler and passenger car loans with zero-processing-fee festival offers

- IFC-backed USD 400 million EV lending facility

- e-Mandate EMI debits for seamless repayment collection

- Embedded finance integration with OEM dealer CRM platforms

Pros

- Best-in-class profitability (PAT of ₹16,638 crore in FY25) enables competitive rates

- Digital and physical scale unmatched among NBFCs

- Pre-approved loan offers for existing Bajaj customer base

Cons

- Primarily strong in two-wheelers and mass-market vehicles; less focused on commercial vehicles

- High valuation (6.4x book) reflects premium positioning — may not be the cheapest lender

Market Share

India’s largest NBFC by AUM at ₹4.44 lakh crore; significant auto loan portfolio within the broader consumer finance book.

Hero FinCorp

Founded: 1991 (as Hero Honda FinLease Ltd)

Headquarters: New Delhi, India

Hero FinCorp is the financial services arm of Hero MotoCorp — India’s largest two-wheeler manufacturer. Its flagship product is two-wheeler financing, covering 95% of the vehicle’s on-road price for Hero MotoCorp bikes. The NBFC has grown to annual revenue of ₹9,900 crore (FY25) and has raised $417 million in funding, with Apollo Global Management as a key investor. It recently launched ‘Project Dhruv Tara,’ an AI lending platform, in March 2026. Maruti Suzuki also inked a partnership with Hero FinCorp for vehicle financing solutions in March 2025.

Top Features

- 95% on-road price financing for Hero MotoCorp two-wheelers

- 2,000+ retail touchpoints and partnerships with 2,000+ corporate clients

- AI lending platform (‘Project Dhruv Tara’) for faster decisioning

- Certified and non-certified used car financing

- Loyalty personal loan product for EMI-timely two-wheeler customers

- New partnership with Maruti Suzuki for four-wheeler financing (2025)

Pros

- Deep OEM integration with Hero MotoCorp ensures high loan attachment at point of sale

- Quick decisioning — initial eligibility verdict within 15 minutes

- Strong trust brand among first-time vehicle buyers

Cons

- Historically limited to Hero MotoCorp ecosystem for two-wheelers; diversification still ongoing

- IPO-bound; reported 80% rise in losses from bad loans in early FY25 (since monitored closely)

Market Share

Dominant in Hero MotoCorp’s two-wheeler financing universe; annual revenue of ₹9,900 crore as of FY25.

RevFin

Founded: 2018

Headquarters: New Delhi, India

RevFin is a purpose-built digital lending platform focused on electric vehicle financing for commercial fleets — think electric three-wheelers, two-wheelers, and four-wheel cargo vehicles. Founded by Sameer Aggarwal, it uses biometrics, psychometrics, and gamification to underwrite borrowers who would traditionally be turned away by banks. By the end of 2024, RevFin had financed 75,000+ EVs and disbursed over ₹1,000 crore in total loans, targeting ₹5,000 crore by March 2026.

Top Features

- AI-driven credit scoring using biometrics, psychometrics, and gamification — no traditional credit history required

- Focused entirely on EV commercial vehicle financing

- Partnerships with Zappit (airport EVs), Sun Mobility, Pure EV, Hero Electric, Piaggio EV, and more

- EV leasing division creating a secondary market for used EVs

- Target: finance 20 lakh vehicles and disburse ₹20,000 crore in 5 years

Pros

- Uniquely designed for underbanked EV operators in Tier II/III cities

- Non-traditional data ensures high financial inclusion

- First-mover advantage in commercial EV financing — a fast-growing segment

Cons

- Smaller scale compared to established NBFCs; still in growth mode

- Concentration risk in the commercial EV segment, which is subject to policy changes

Kuwy Technology Service

Founded: 2015

Headquarters: Chennai, India

Backed by Volkswagen Finance, Kuwy is an automotive fintech platform that powers automated lending for both direct and indirect channels. In February 2023, it launched KUWYLaaS (Lending-as-a-Service), an end-to-end digital lending infrastructure for online car sellers, dealers, and OEMs. With a presence across 70+ locations, Kuwy connects consumers, dealers, OEMs, and lenders in a single automated workflow.

Top Features

- KUWYLaaS: Lending-as-a-Service platform for dealers and OEMs

- Automated loan origination, verification, and credit scoring

- Strategic partnerships with OEMs, online car platforms, and financial institutions

- Digital retail solutions enabling enhanced buyer experience and data insights

- 70+ location coverage with pan-India ambition

Pros

- Unique B2B positioning — helps dealers and OEMs embed financing into their platforms

- Volkswagen Finance backing lends credibility and capital access

- Automated end-to-end process reduces loan processing times

Cons

- Less consumer-facing visibility compared to Rupyy or CARS24

- Scale (70+ locations) still limited relative to market leaders

Sundaram Finance

Founded: 1954

Headquarters: Chennai, India

One of India’s oldest and most respected NBFCs, Sundaram Finance has 620+ branches and is the dominant vehicle financier in South India. It covers new and used cars, commercial vehicles, tractors, and construction equipment. The company is known for its conservative risk culture, transparent processes, and consistently low NPA ratios. It also offers a Drive Assure insurance plan bundled with car loans.

Top Features

- Financing for all major car brands including imported vehicles

- 620+ branches with strong South India dominance

- Drive Assure insurance bundled with vehicle loans

- NRI vehicle financing — a rare offering among NBFCs

- Special loan products for women, senior citizens, and persons with disabilities

- Customized used car financing with pre-approved offers for creditworthy customers

Pros

- 70 years of vehicle financing expertise — unmatched trust and stability

- Strong ethics and transparency — very low NPA track record

- Customized products for niche customer segments

Cons

- Geographic concentration in South India limits the Pan-India scale

- Less aggressive in digital lending compared to newer fintech rivals

Market Share

Among the top 5 NBFC vehicle lenders in South India, the total loan book is well above ₹40,000 crore.

HDFC Bank (Vehicle Loans)

Founded: 1994

Headquarters: Mumbai, India

HDFC Bank is India’s largest private sector bank and a dominant player in the vehicle financing segment. Non-captive banks held 51.72% of India’s auto loan market share in 2025, and HDFC Bank commands the largest chunk of that. It offers car loans, two-wheeler loans, and commercial vehicle loans with the biggest pool of pre-approved customers, competitive interest rates, and rapid digital processing. Its October 2023 expansion of auto loan offerings targeted first-time and younger buyers.

Top Features

- Largest pre-approved customer pool among all banks for instant car loans

- Up to 90% on-road price financing with income document waivers for salary account holders

- Real-time digital approvals and sub-24-hour disbursements for pre-approved customers

- Co-lending partnerships with NBFCs for heavy truck and commercial vehicle segments

- Embedded EV financing for brands like Tesla India (Kotak Mahindra Prime integration)

Pros

- Lowest cost of funds among vehicle lenders — translates to competitive interest rates

- Massive branch and ATM network for customer servicing

- Digital lending journeys tightly integrated into the HDFC Bank app

Cons

- Stricter credit norms mean thin-file or informal income borrowers may not qualify

- Not as specialized in used commercial vehicles as NBFCs like Shriram or Chola

Market Share

India’s largest private bank, a dominant contributor to the 51.72% bank share of the auto loan market.

TVS Credit Services

Founded: 2008

Headquarters: Chennai, India

TVS Credit Services, part of the TVS Group, is a specialist lender for two-wheelers and three-wheelers across India. It works closely with TVS Motor Company dealerships and has expanded into used vehicles and personal loans. The company has consistently run promotional EMI schemes, and with over 13,000 channel partners, it has one of the widest dealer-integrated distribution networks for two-wheeler loans.

Top Features

- Specialised two-wheeler and three-wheeler loan products

- 13,000+ channel partners, including TVS Motor dealerships

- Quick sanction — typically within the same day at the dealership

- Used vehicle financing and personal loan products

- Digital loan servicing through app and web portal

Pros

- Deep OEM integration at the point of sale ensures high conversion

- Strong Tier III and rural presence alongside the TVS dealer network

- Promotional schemes with zero down payment on select models

Cons

- Limited diversification beyond two/three-wheelers

- Dependent on TVS Motor Company’s sales performance

Market Share

Among the top 5 two-wheeler financing NBFCs in India; over 13,000 channel partners.

CarWale Finance

Founded: 2005 (CarWale); loan marketplace active

Headquarters: Mumbai, India

CarWale, owned by CarTrade Tech, is India’s leading auto portal and also operates a vehicle loan marketplace that connects buyers to leading bank and NBFC lenders. By filling out one form, users receive custom-fit loan quotes from multiple lenders with up to 100% financing on select vehicles. CarWale’s strength lies in its massive organic traffic of millions of car researchers who naturally convert into loan applicants.

Top Features

- Single-form multi-lender loan comparison and application

- Up to 100% financing on select vehicles from top bank and NBFC partners

- Integrated with vehicle discovery — users can find a car and apply for a loan in the same session

- Pocket-friendly EMI quotes customised to user’s income and credit profile

- EMI calculator and eligibility checker built into the platform

Pros

- Strong consumer-facing brand with millions of monthly users

- No paperwork submission required upfront — banks process after receiving the form

- Covers both new and used car financing

Cons

- Acts as a marketplace only — no proprietary lending book

- Loan approval and rates ultimately depend on partnered lenders

Droom Credit (Droom Technology)

Founded: 2014 (Droom Credit launched subsequently)

Headquarters: Gurugram, India

Droom is India’s first data-driven online automobile marketplace and one of the pioneers of digital used vehicle financing through its Droom Credit arm. Leveraging OBV (Orange Book Value) — a proprietary algorithmic pricing engine for used vehicles — Droom Credit offers vehicle-linked loans where pricing, valuation, and financing are all handled on one platform. This makes it particularly useful for buyers who are uncertain about fair pricing before committing to a loan.

Top Features

- OBV (Orange Book Value): AI-based fair price discovery for 50 million+ vehicle configurations

- End-to-end digital used vehicle financing integrated with vehicle listing

- Full-stack marketplace: buy, sell, insure, and finance used vehicles in one place

- Droom History report for vehicle background checks

- Coverage of cars, bikes, scooters, and commercial vehicles

Pros

- Unique pricing transparency through OBV makes financing decisions more informed

- First-in-class integration of vehicle history, pricing, and financing

- Strong digital-native audience of used vehicle buyers

Cons

- Smaller scale compared to CARS24 and CarDekho in used car transactions

- Droom’s overall GMV has faced competitive pressure from well-funded rivals

Emerging Trends Reshaping Vehicle Financing in 2026

The vehicle financing landscape in India is undergoing its most significant transformation in decades. A few key trends are worth calling out:

EV Financing Goes Mainstream:

With India’s EV financing market expected to grow at a 51.62% CAGR to reach USD 28.79 billion by 2031, almost every lender from Bajaj Finance to RevFin is building EV-specific products. OEM-subsidized rates and government-backed incentives are compressing costs.

Account Aggregator & Digital KYC:

RBI’s Account Aggregator framework and Digital Lending Directions 2025 mandate standardized e-KYC and transparent pricing, making it easier for lenders to underwrite borrowers with non-traditional income without sacrificing compliance.

Co-Lending Proliferation:

Banks and NBFCs are increasingly co-lending — with HDFC Bank and Axis Bank providing low-cost funds alongside NBFCs that contribute field origination and last-mile servicing.

Online Direct Lending Boom:

While dealership point-of-sale dominated 67.58% of India’s auto loan market in 2025, online direct lending is growing at an 8.78% CAGR through 2031, driven by instant approvals and rate transparency.

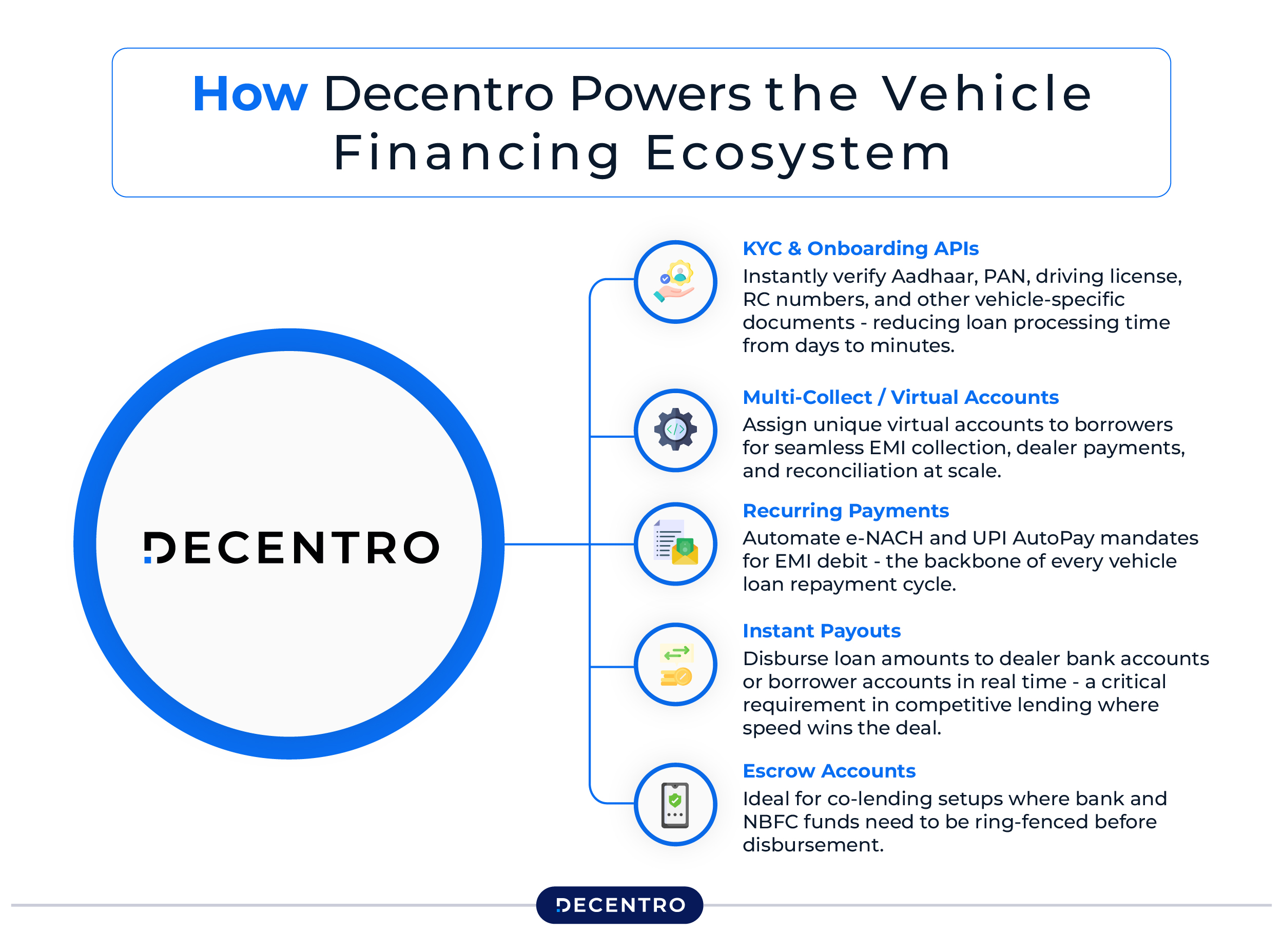

How Decentro Powers the Vehicle Financing Ecosystem

Building or scaling a vehicle financing platform is not just about lending capital — it’s about the rails on which the entire process runs. From loan application to KYC verification, from EMI collection to instant disbursement to dealers and borrowers, every step needs robust financial infrastructure.

That’s where Decentro comes in.

For vehicle financing platforms, Decentro’s stack addresses some of the most operationally painful workflows:

- KYC & Onboarding APIs: Instantly verify Aadhaar, PAN, driving license, RC numbers, and other vehicle-specific documents — reducing loan processing time from days to minutes.

- Multi-Collect / Virtual Accounts: Assign unique virtual accounts to borrowers for seamless EMI collection, dealer payments, and reconciliation at scale.

- Recurring Payments: Automate e-NACH and UPI AutoPay mandates for EMI debit — the backbone of every vehicle loan repayment cycle.

- Instant Payouts: Disburse loan amounts to dealer bank accounts or borrower accounts in real time — a critical requirement in competitive lending where speed wins the deal.

- Escrow Accounts: Ideal for co-lending setups where bank and NBFC funds need to be ring-fenced before disbursement.

Whether you’re a fintech startup building India’s next Rupyy, an NBFC digitizing your vehicle loan origination, or an OEM deploying embedded financing at the dealership — Decentro’s API infrastructure is the connective tissue that makes it all work.

Frequently Asked Questions

What is a vehicle financing platform?

A vehicle financing platform is a digital or hybrid lender, marketplace, or NBFC that provides loans, leases, or credit facilities to help individuals or businesses purchase vehicles — including cars, bikes, trucks, and EVs.

Which is the best vehicle financing platform in India in 2026?

Rupyy, CARS24 Financial Services, Shriram Finance, and Mahindra Finance are among the best vehicle financing platforms in India, each excelling in different segments — digital used car loans, commercial vehicles, and rural markets respectively.

What is the size of the vehicle financing market in India?

The India auto loan market is valued at approximately USD 46.33 billion in 2026 and is projected to grow to USD 63.82 billion by 2031 at a CAGR of 6.62%.

How are NBFCs different from banks in vehicle financing?

NBFCs typically offer more flexible credit assessment criteria, faster processing, and better service in Tier II/III markets. Banks offer lower interest rates but have stricter eligibility requirements.

Are there dedicated EV financing platforms in India?

Yes. RevFin, Ecofy, and lending arms of Bajaj Finance and Mahindra Finance are actively building EV-specific financing products, supported by government subsidies and green financing facilities.