Learn what CKYCRR means, how the Central KYC Records Registry works, the latest CKYCRR 2.0 updates, and why it matters for financial institutions and fintech startups in India.

What is CKYCRR? Full Form, Meaning & How It Works

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

| Summary Every time you open a new bank account, apply for a mutual fund, or get insurance in India, you’re asked to submit the same stack of documents. PAN card. Aadhaar. Address proof. Photo. Again and again. CKYCRR — the Central Know Your Customer Records Registry — was built specifically to fix this. It’s India’s centralised framework that lets customers complete KYC verification once and reuse that verified identity across every financial institution they ever deal with. For financial institutions and fintech startups, it’s not just about customer convenience. It’s a compliance mandate, an operational upgrade, and increasingly, a competitive advantage. This article breaks down what CKYCRR means, exactly how it works, the major CKYCRR 2.0 update and what changed, and why getting this right matters more than ever in 2026. |

Setting the Context: Why KYC Needs an Overhaul

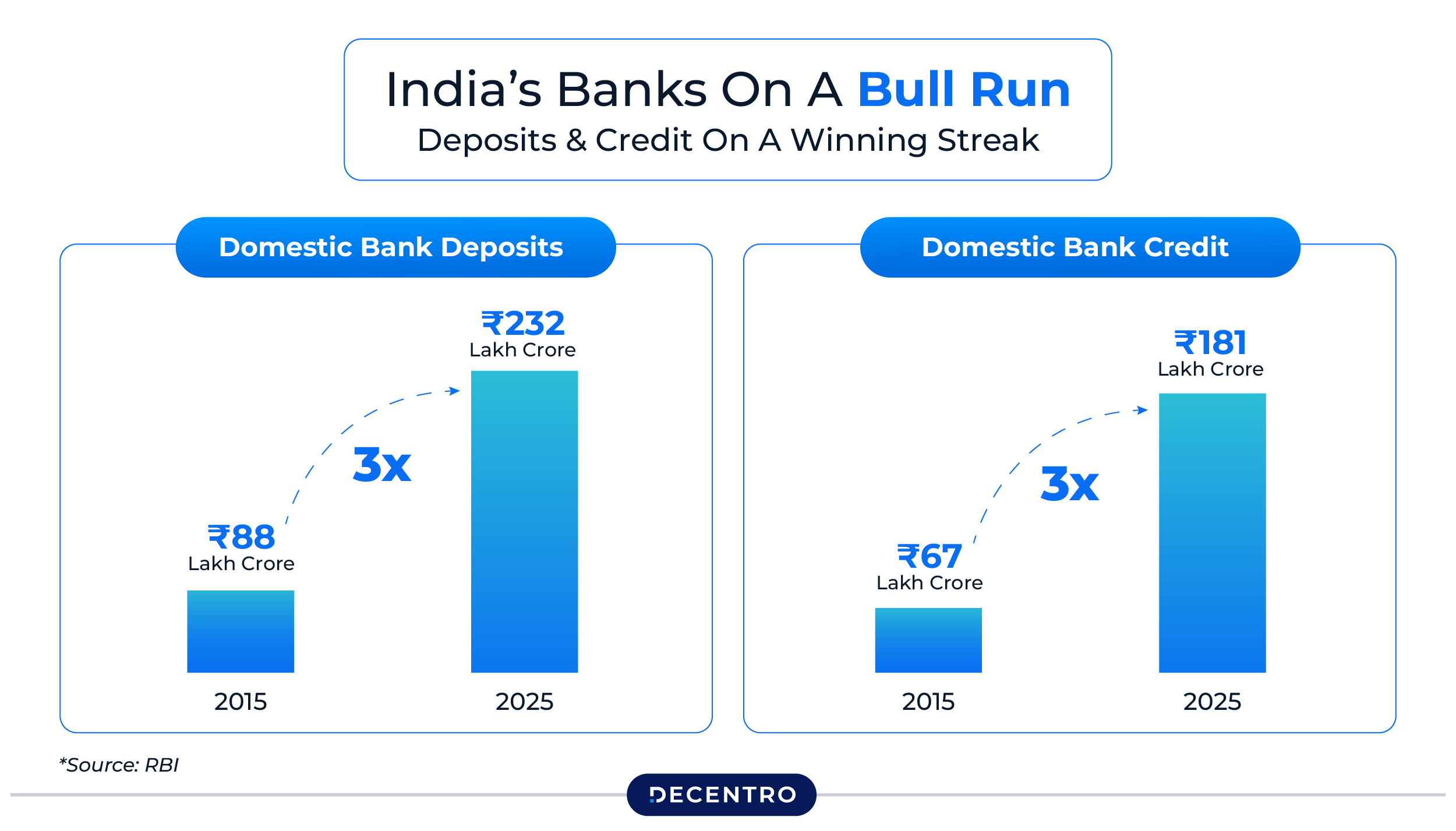

India’s financial sector has grown explosively. As of 2024, the country has over 750 million bank account holders, more than 150 million active mutual fund investors, and the Unified Payments Interface processed 228.3 billion transactions worth USD 3.4 trillion in calendar year 2025. Every single one of those customers needed to complete KYC verification at some point — and most had to do it multiple times, across multiple institutions.

Think about what that costs. A single manual KYC verification costs a financial institution between ₹200 and ₹500. Multiply that across millions of customers, factoring in document storage, retrieval, and re-verification, and the number becomes staggering.

Meanwhile, over 7,166 reporting entities regulated by RBI, SEBI, IRDAI, and PFRDA are now required to comply with India’s centralised KYC framework. The regulatory pressure is real. So is the opportunity to streamline.

That’s exactly the problem CKYCRR solves.

What is CKYCRR? Full Form and Meaning

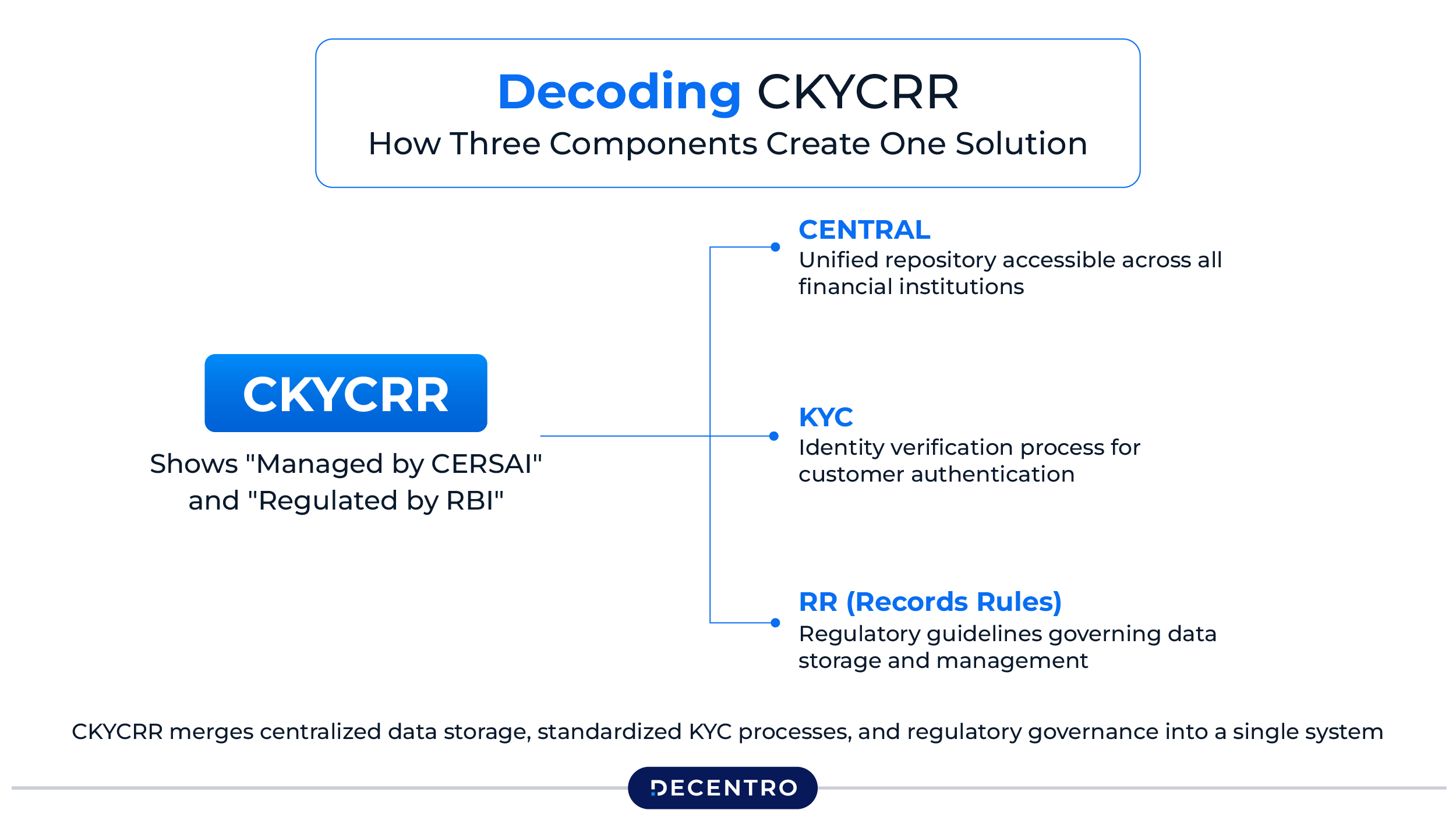

CKYCRR stands for Central Know Your Customer Records Rules.

Let’s unpack that:

- Central → A unified, single-source system

- Know Your Customer → The identity verification process is mandated for all financial institutions

- Records Rules → The regulatory guidelines that govern how this information is stored, accessed, and maintained

Simply put, CKYCRR is the regulatory rulebook that governs India’s centralised KYC system. The actual repository where customer KYC data lives is called the CKYC Registry (CKYCR), managed by CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest of India) under the authority of the Reserve Bank of India.

Think of it this way: if CKYCRR is the law, the CKYC Registry is the system built to follow that law.

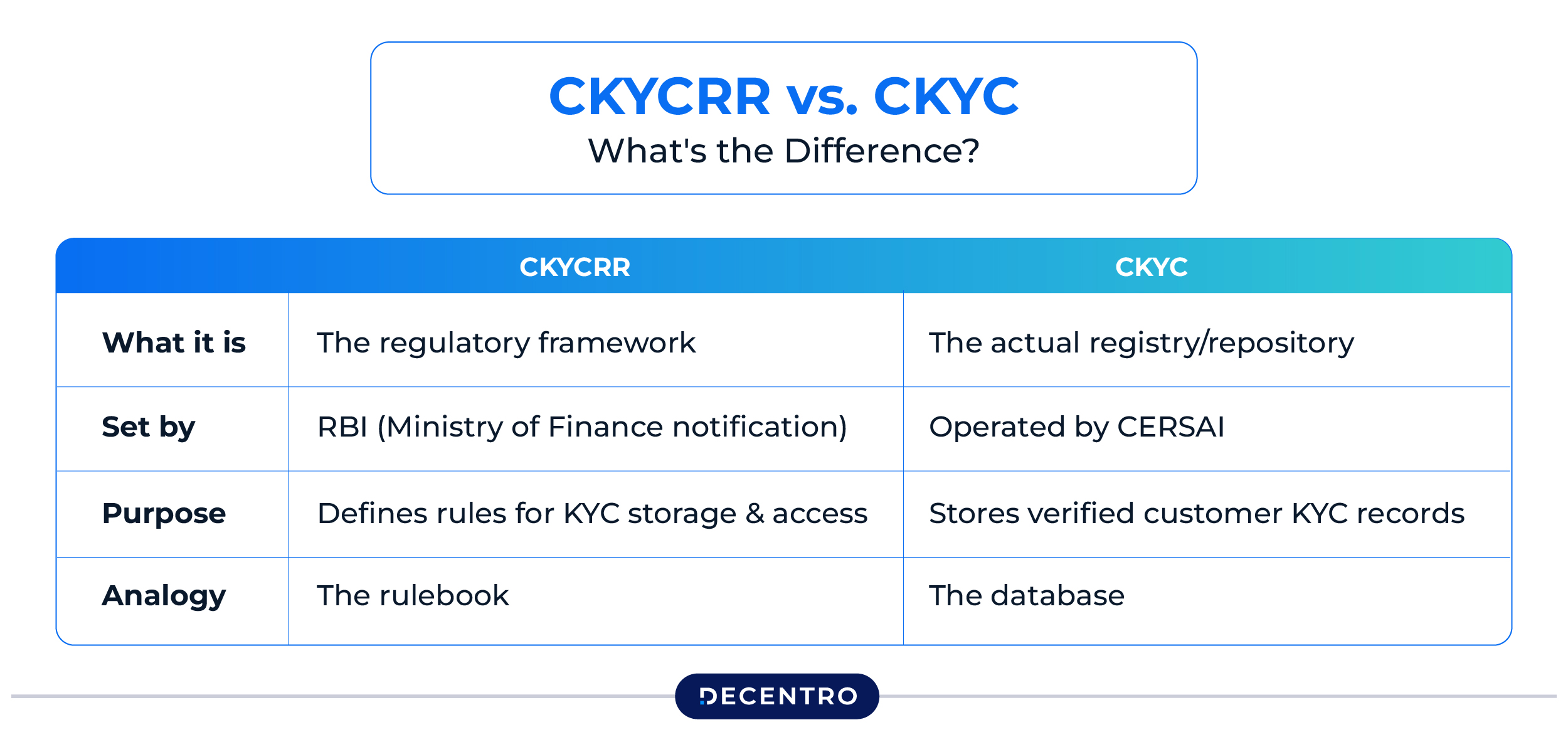

CKYCRR vs. CKYC: What’s the Difference?

| CKYCRR | CKYC | |

| What it is | The regulatory framework | The actual registry/repository |

| Set by | RBI (Ministry of Finance notification) | Operated by CERSAI |

| Purpose | Defines rules for KYC storage and access | Stores verified customer KYC records |

| Analogy | The rulebook | The database |

Legal Foundation: Where Does CKYCRR Come From?

CKYCRR operates within a solid legal structure built on two major pillars:

1. Prevention of Money Laundering Act, 2002 (PMLA): This makes KYC mandatory for all financial institutions and establishes anti-money laundering requirements. It came into force in 2005 and is the reason every Indian with a bank account has submitted identity documents.

2. SARFAESI Act, 2002: This provides the legal backing for CERSAI’s existence as the central registry administrator. Section 20 of the Act authorised CERSAI’s creation.

Key regulatory milestones to know:

- January 2017: Ministry of Finance officially authorized CERSAI as the CKYC Records Registry

- April 2021: CKYCRR requirements extended to legal entities (companies, trusts, partnerships)

- November 2024: RBI amendments aligned CKYCRR procedures with updated PMLA rules

- 2025: CKYCRR 2.0 announced in Union Budget — a full platform upgrade with AI-based matching, real-time APIs, and facial de-duplication

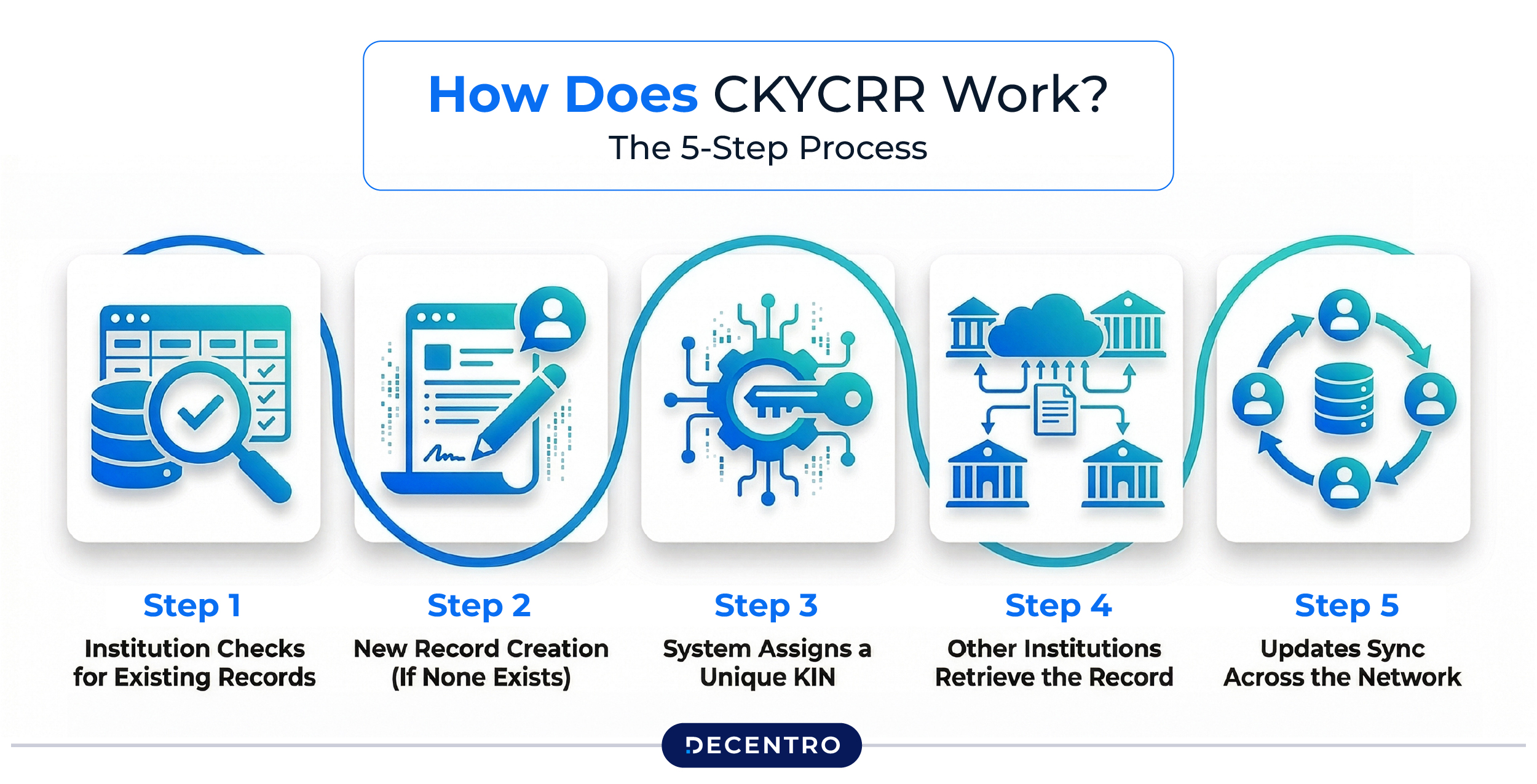

How Does CKYCRR Work? The 5-Step Process

Here’s how the system actually functions, step by step:

Step 1: Institution Checks for Existing Records

When a customer wants to open an account or access financial services, the institution first searches the CKYC Registry using the customer’s PAN, Aadhaar, or mobile number. If a verified record already exists, there’s no need to collect documents again.

Step 2: New Record Creation (If None Exists)

If no record is found, the institution collects standard KYC documents: identity proof, address proof, and a photograph, verifies them against official databases, and uploads the verified data to CERSAI.

Step 3: System Assigns a Unique KIN

CKYCRR processes the uploaded data and generates a 14-digit KYC Identifier Number (KIN), the customer’s permanent ID within the system. CERSAI sends this KIN via SMS and email to the customer’s registered contacts.

This number works across every financial institution in India, for life.

Step 4: Other Institutions Retrieve the Record

The next time the customer approaches a different bank or insurer, they simply provide their KIN with consent. The new institution retrieves the full, verified record in seconds — no paperwork required.

Step 5: Updates Sync Across the Network

If the customer updates their address or phone number at one institution, that change is uploaded to CERSAI, which pushes notifications to all other institutions where the customer holds accounts. Everyone stays in sync.

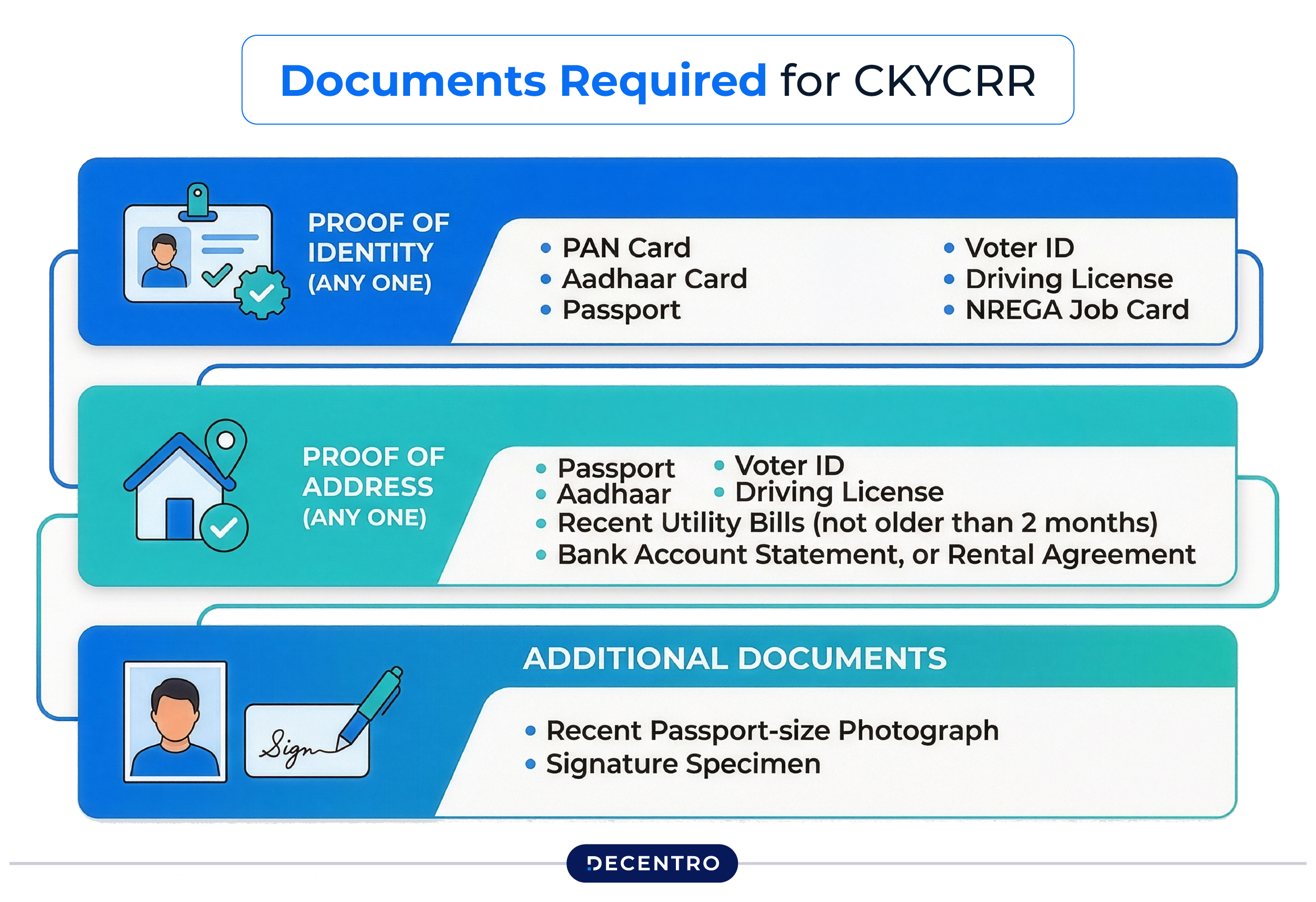

Documents Required for CKYCRR

To create a CKYCRR record, customers need to submit:

Proof of Identity (any one): PAN card, Aadhaar card, Passport, Voter ID, Driving License, NREGA Job Card

Proof of Address (any one): Passport, Voter ID, Driving License, Aadhaar, recent utility bills (not older than 2 months), Bank account statement, or rental agreement

Additional: Recent passport-size photograph and signature specimen

Once submitted and verified at any one institution, the customer never has to produce these again when approaching another regulated entity.

Key Benefits of CKYCRR

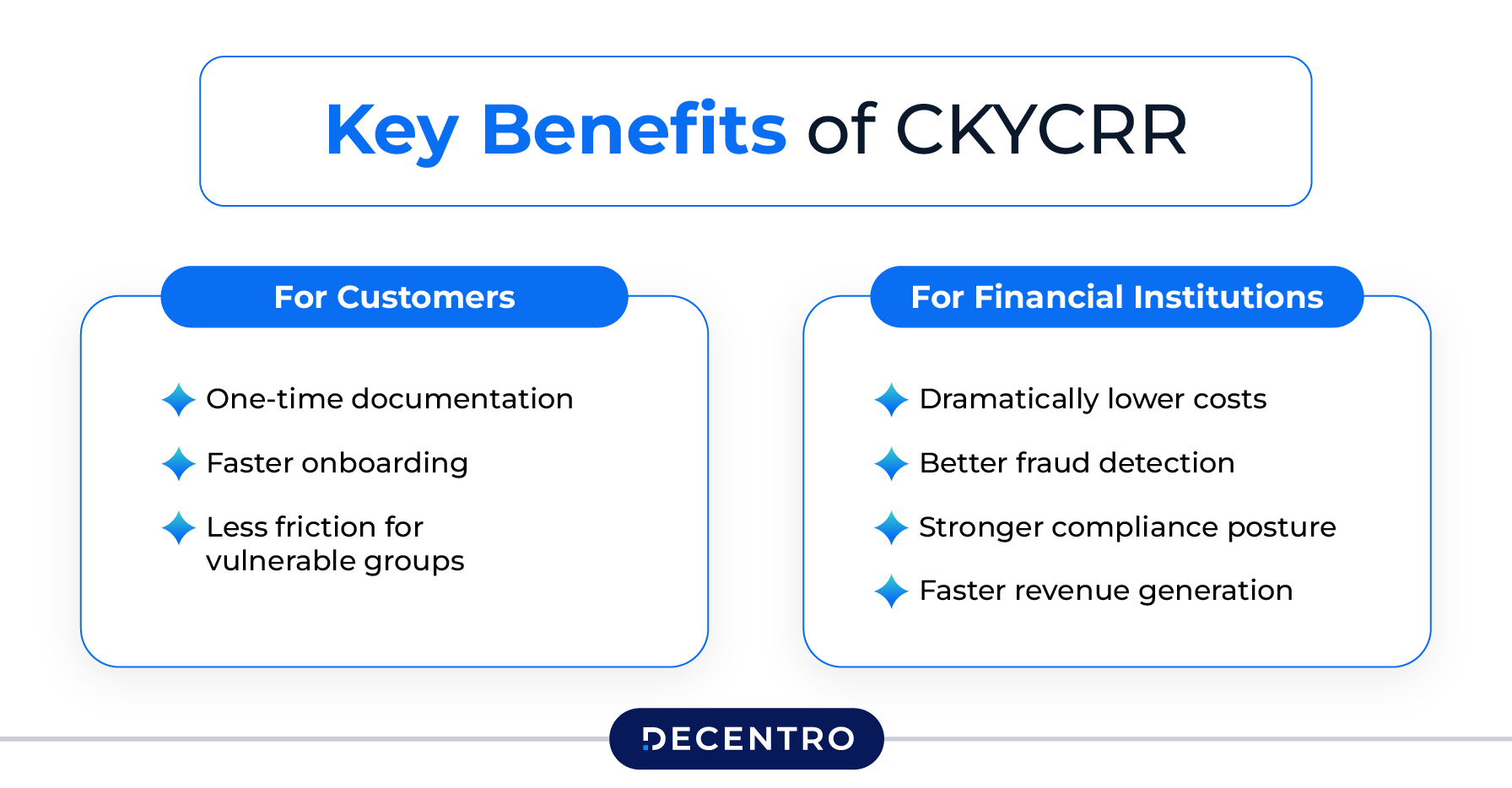

For Customers

One-time documentation. Submit your KYC details once, and that’s it. Your verified identity follows you across banks, insurers, mutual funds, and NBFCs without any repetition.

Faster onboarding. What used to take 3–5 business days can now be completed in minutes. Customers moving cities or switching financial providers don’t have to start from scratch.

Less friction for vulnerable groups. Senior citizens and rural customers who find it difficult to travel to branches and carry documents repeatedly benefit enormously from this system.

For Financial Institutions

Dramatically lower costs. No more maintaining physical document archives or running in-house verification for every new customer. Institutions access pre-verified data directly from the central registry.

Better fraud detection. The centralised nature of the system means discrepancies become visible across institutions. If someone attempts to register different addresses at multiple banks simultaneously, the system flags it.

Stronger compliance posture. A single centralised record reduces the risk of data inconsistencies, reliance on expired documents, or human error in manual verification.

Faster revenue generation. Quicker customer onboarding means faster account activation, which means the institution can start serving — and earning from — the customer sooner.

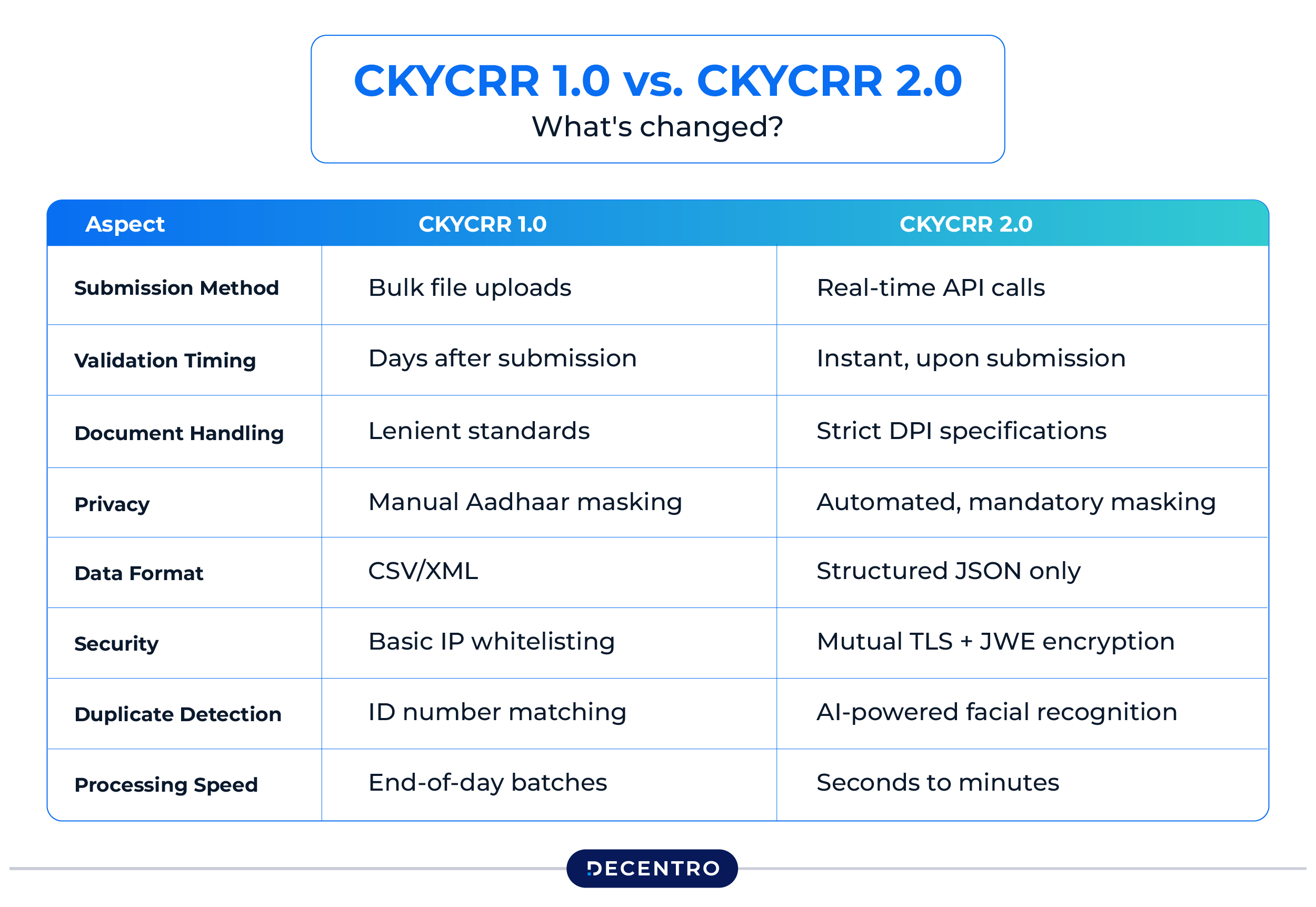

CKYCRR 2.0: What Changed and Why It Matters

The most significant development in the CKYCRR landscape in recent years is CKYCRR 2.0, announced in India’s Union Budget 2025. And it’s not a minor upgrade, it’s a complete platform replacement. With the total number of CKYC records crossing 100 crore (1 billion) in 2025, the new system was designed to handle this scale without delays or errors.

Here’s a quick comparison of what changed:

| Aspect | CKYCRR 1.0 | CKYCRR 2.0 |

| Submission method | Bulk file uploads | Real-time API calls |

| Validation timing | Days after submission | Instant, upon submission |

| Document handling | Lenient standards | Strict DPI specifications |

| Privacy | Manual Aadhaar masking | Automated, mandatory masking |

| Data format | CSV/XML | Structured JSON only |

| Security | Basic IP whitelisting | Mutual TLS + JWE encryption |

| Duplicate detection | ID number matching | AI-powered facial recognition |

| Processing speed | End-of-day batches | Seconds to minutes |

The shift from batch file uploads to real-time API calls is significant. Under the old system, a submission error might not surface until the next day’s batch processing, by which time a customer had already walked away frustrated. Under CKYCRR 2.0, validation is instant, and rejections happen at the point of submission, giving institutions the chance to correct issues on the spot.

The DigiLocker Integration: India’s Identity Stack, Finally Connected

One of the most consequential additions in CKYCRR 2.0 is its integration with DigiLocker, the government’s secure cloud platform where citizens store verified, government-issued documents like Aadhaar, PAN, and driving licences.

Previously, even if a customer had all their documents digitally available, financial institutions still had to collect, verify, and upload them manually. With the DigiLocker-CKYCRR integration now live, that entire step is automated. Institutions can pull verified documents directly from DigiLocker via API, with customer consent, and cross-check them against the CKYC Registry in a single flow.

What this looks like in practice:

- A bank searches the CKYC Registry using the customer’s mobile number

- If no record exists, it pulls authenticated Aadhaar and PAN directly from DigiLocker

- The data is verified against source databases (UIDAI, Income Tax) in real time

- The verified record is uploaded to CERSAI, and a KIN is assigned — all within minutes

The practical impact is hard to overstate. Data from institutions using CKYC sync shows onboarding times dropping by over 43%, with median verification time falling from nearly 5 minutes to under 3 minutes per customer. Rejection rates due to incomplete records also fell from 1.4% to under 0.1%.

There’s also a fraud-prevention dimension. Document forgery, editing a utility bill or scanning a manipulated PAN becomes effectively impossible when verification happens through a cryptographic handshake between government servers rather than a human reviewing a photocopy.

Additionally, CKYCRR 2.0 now gives customers a view-only dashboard to see which institutions have accessed their KYC record, and the ability to revoke access in real time, a meaningful step toward user data sovereignty.

Why does this create urgency?

Legacy Core Banking Systems weren’t built for real-time JSON API connectivity, DigiLocker pull requests, facial de-duplication, or automated Aadhaar masking. Institutions that haven’t upgraded their infrastructure are essentially running a system that CKYCRR 2.0 no longer accommodates.

CKYCRR Updates to Track in 2025–26

Staying compliant means staying current. Here are the key regulatory developments:

- Risk-based re-verification timelines: High-risk customers must update KYC every 2 years; medium-risk every 8 years; low-risk every 10 years

- Extended timelines for low-risk customers (June 2025 circular): New structured reminder systems were introduced to prevent account inoperability

- Legal entity mandate (since April 2021): Companies, trusts, partnerships, and other legal entities are now fully within the CKYCRR compliance net

- 7-day update rule: Any change in customer information must be submitted to CKYCRR within 7 days of receiving it

What Happens If a Financial Institution Is Non-Compliant?

Non-compliance with CKYCRR isn’t a grey area. Regulators have made enforcement a priority, and the numbers tell that story clearly.

In FY 2024–25 alone, the RBI imposed penalties totalling ₹54.78 crore on 353 regulated entities, including major private banks, foreign banks, NBFCs, and co-operative banks, for violations ranging from KYC lapses to exposure reporting failures. That’s not a rounding error. It’s a signal.

This follows an 88% increase in enforcement actions between 2021 and 2024, much of it tied to gaps in AML and KYC compliance. The regulator has shifted from occasional course-correction to systematic scrutiny.

The Four Levels of Consequence

1. Monetary Penalties

RBI can impose financial penalties under the Banking Regulation Act and the PMLA. These aren’t token fines. ICICI Bank was fined ₹75 lakh in August 2025 for operational compliance breaches, including gaps in the KYC process. Manappuram Finance was fined for failing to adhere to KYC guidelines, specifically for not verifying PAN details from official databases. No institution is considered too large or too established to be penalised.

2. Operational Restrictions

Penalties can go beyond fines. A high-profile example is Paytm Payments Bank, in 2024, the RBI barred it from accepting fresh deposits, facilitating credit transactions, and allowing top-ups, citing “persistent non-compliances and material supervisory concerns.” The result: operational disruption, reputational damage, and a sharp drop in its parent company’s share price. This is what regulatory non-compliance looks like at scale.

3. Licence Cancellation

In extreme cases of repeated or wilful non-compliance, RBI can cancel a financial institution’s Certificate of Registration (CoR). This was the penalty imposed on X10 Financial Services Limited in January 2025 for, among other violations, outsourcing core KYC decision-making functions to a third party without proper due diligence.

4. Legal Liability

The consequences extend beyond regulatory penalties. India’s Supreme Court recently flagged bank laxity in KYC as a “deficiency of service” — and emphasised that if a bank’s failure to follow KYC norms leads to cyber fraud, the bank can be held liable for the customer’s loss. That’s a civil liability exposure that regulatory fines don’t even begin to capture.

The Most Common KYC Violations

The pattern of enforcement in recent years reveals a consistent set of failure points:

- Allotting more than one Unique Customer Identification Code (UCIC) to the same customer, due to poor integration between core banking systems and onboarding platforms

- Failing to update KYC data based on risk category timelines periodically

- Delegating core KYC decision-making to third-party agents without maintaining institutional ownership over compliance

- Not masking Aadhaar data in stored records

- Missing the 7-day window to upload customer information updates to CERSAI

The uncomfortable truth is that most of these aren’t complex breaches. They’re process failures, systems built for speed that skipped regulatory accuracy. As RBI’s enforcement trend makes clear, compliance can no longer be treated as a back-office function; it is a leadership priority.

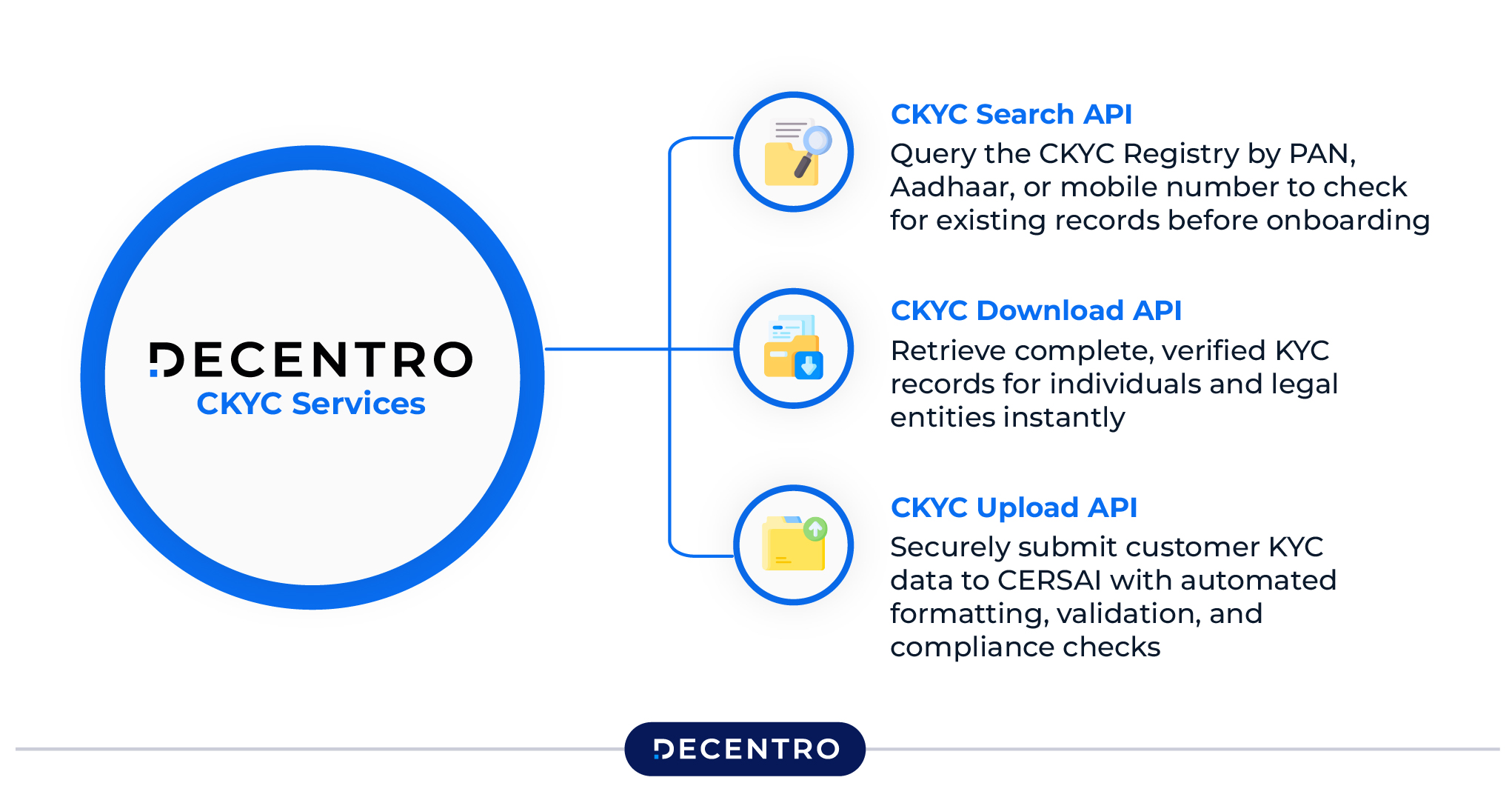

How Decentro Makes CKYCRR Seamless

For fintechs, NBFCs, and digital-first financial platforms navigating CKYCRR compliance, the technical overhead can be considerable — especially with CKYCRR 2.0’s real-time API requirements.

Decentro’s CKYC Services offer a comprehensive API suite that handles this end-to-end:

- CKYC Search API: Query the CKYC Registry by PAN, Aadhaar, or mobile number to check for existing records before onboarding

- CKYC Download API: Retrieve complete, verified KYC records for individuals and legal entities instantly

- CKYC Upload API: Securely submit customer KYC data to CERSAI with automated formatting, validation, and compliance checks

Rather than building and maintaining direct CERSAI connectivity in-house, which involves complex security protocols, data transformation, and ongoing maintenance, teams can integrate Decentro’s APIs and have CKYC-ready infrastructure running in days, not months.

For platforms focused on growth and user experience, this is the difference between spending engineering cycles on compliance plumbing vs. building the actual product. Explore Decentro’s CKYC Services documentation to see what’s possible.

Conclusion

CKYCRR isn’t just a compliance checkbox. It’s a foundational infrastructure upgrade for India’s financial sector, one that reduces friction for customers, cuts costs for institutions, and significantly hardens fraud prevention.

With CKYCRR 2.0 now in motion, the bar has been raised further. Real-time APIs, AI-based de-duplication, mandatory Aadhaar masking, and instant validation are no longer optional capabilities; they’re the baseline.

For startups and digital financial platforms building in India, the question isn’t whether to get CKYCRR-compliant. It’s how to do it efficiently, without it becoming a bottleneck to growth. Getting the infrastructure right, whether through in-house builds or platforms like Decentro, is what separates institutions that onboard customers in seconds from those still stuck in the 3-day verification queue.

Looking for a solution?

Frequently Asked Questions

Q1. Is CKYCRR mandatory for all financial institutions in India?

Yes. All entities regulated by RBI, SEBI, IRDAI, and PFRDA are required to comply with CKYCRR. This includes banks, NBFCs, mutual funds, insurance companies, and brokerages. For individual accounts, the mandate has been in effect since January 2017; for legal entities, since April 2021.

Q2. What is the KYC Identifier Number (KIN), and how long does it remain valid?

The KIN is a unique 14-digit number assigned to a customer when their KYC record is first registered in the CKYC Registry. It remains valid for the customer’s lifetime unless the record is deactivated. Customers can use this number with any regulated financial institution to avoid resubmitting KYC documents.

Q3. What happens if a customer’s information changes after their CKYCRR record is created?

When a customer updates any information — address, phone number, or identity documents — the institution receiving the update must upload the revised details to CERSAI within 7 days. CERSAI then pushes electronic notifications to all other institutions that hold accounts for that customer, ensuring records stay synchronised across the system.

Q4. What is the difference between CKYCRR 1.0 and CKYCRR 2.0?

CKYCRR 2.0 is a full platform replacement, not just an update. The key changes include a shift from batch file uploads to real-time API connectivity, instant data validation (vs. delayed batch rejections), AI-powered facial de-duplication, automated Aadhaar masking, structured JSON data formats, and stronger security via Mutual TLS authentication and JWE encryption.

Q5. Can a fintech startup or NBFC integrate CKYCRR compliance through a third-party API provider?

Yes. Rather than building direct CERSAI connectivity from scratch — which involves complex technical infrastructure and significant development time — financial platforms can use API providers like Decentro, which offer ready-to-integrate CKYC Search, Download, and Upload APIs. This approach allows platforms to become CKYCRR-compliant quickly while keeping engineering resources focused on product development.