In-depth guide on integrating payment gateways in 2023. We go into the basics of payment gateways, how they work, and how to pick one that works for you.

How To Do A Payment Gateway Integration In 2024

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

The dizzying rate at which the payments landscape has been evolving makes it imperative to keep track of where we are now.

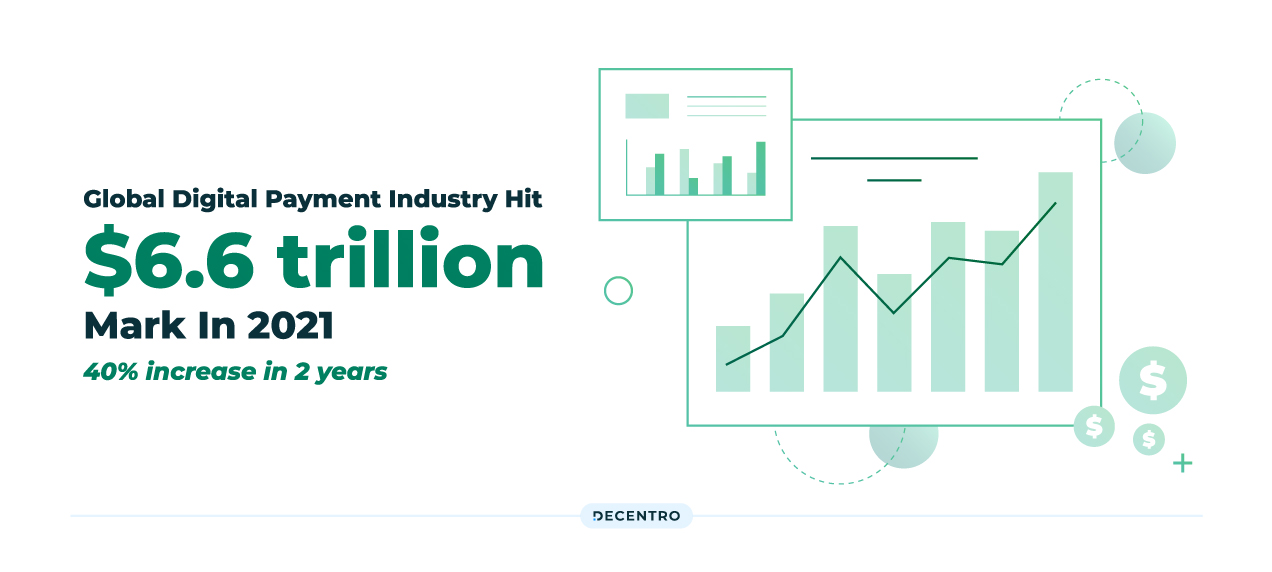

The global digital payment industry hit the USD 6.6 trillion mark in 2021, registering around a 40% jump in two years.

We have witnessed major shifts, ranging from the dawn of the plastic economy to the push towards a cashless one. We are in an era where one-tap payments have been competing fiercely against one-click payments, making us the poster child of innovation.

Even with customer experience, innovation has found itself having the front-row seats, driving efficiency, convenience, and the need to prevent fraudulent transactions.

But if we focus on payment gateways, the need has primarily come from the e-commerce boom that the economy witnessed in the early and mid-90s.

- The global payment gateway market was valued at USD 26.79 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 22.2% from 2023 to 2030.

- Speaking strictly for the Indian Market, the India payment gateway market size reached US $1,459.7 Million in 2022. IMARC Group expects the market to reach US$ 2,897.6 Million by 2028, exhibiting a growth rate (CAGR) of 11.6% during 2023-2028.

In 1996, ICICI Bank started internet banking services for its customers for the first time. With the platform for online banking set up, Billdesk set up the first payment gateway in India in 1999.

In 2007, a startup called Flipkart opened online for business. Flipkart changed how people shopped online by giving all products and services in one place, which also presented the need for integrating a secure and reliable payment gateway on the website.

But before we go any further, let’s define a payment gateway.

What is a payment gateway?

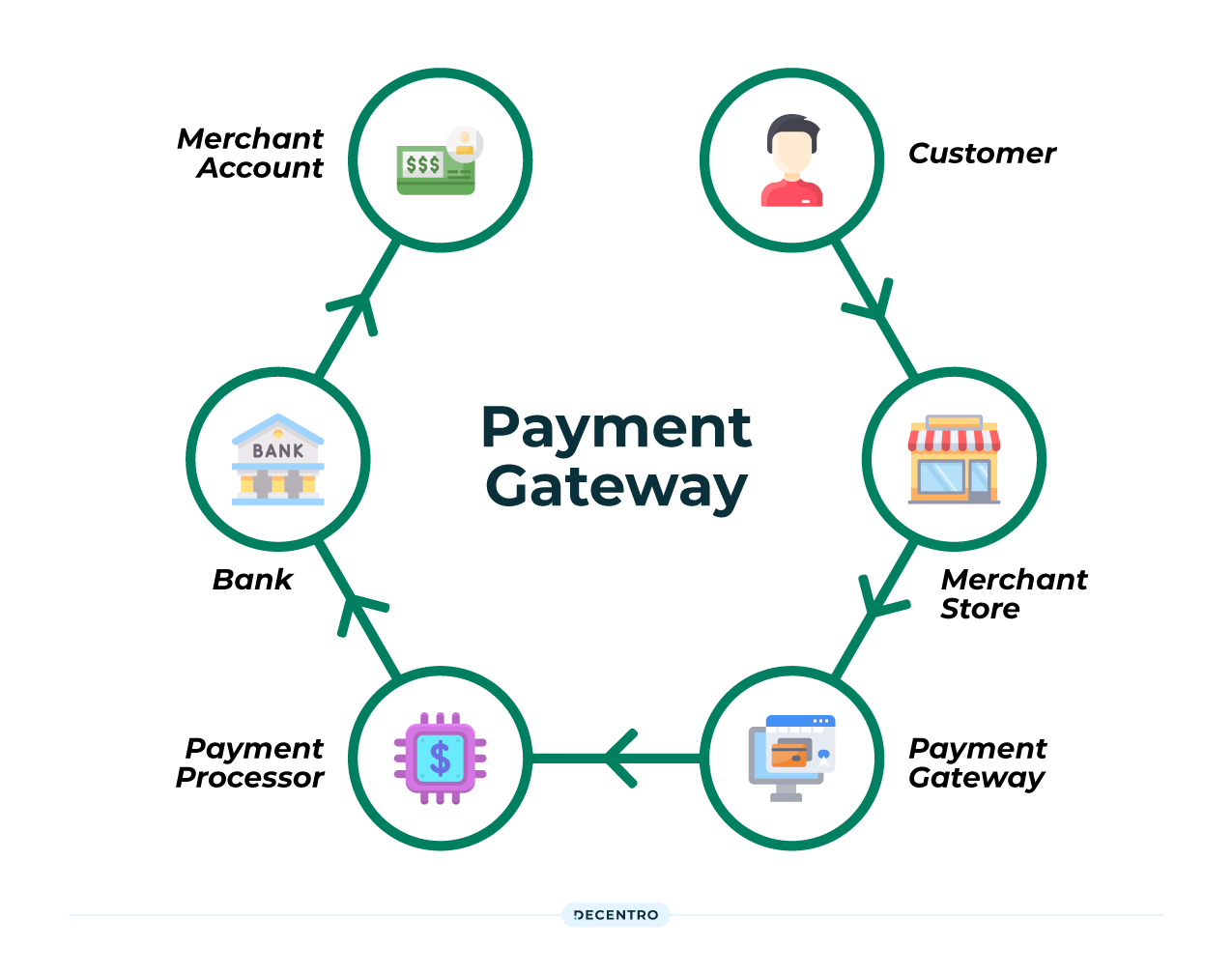

A payment gateway is a “middleman” between clients and merchants. They help in transactions between merchants and their consumers quickly and safely.

First, it verifies that the customer has the funds on his card (a digital wallet or any other payment method) to cover the purchase.

Then it ensures full protection of sensitive data processed inside the system by encryption and a wide array of security measures such as firewalls and fraud detection systems. These systems, which run on the back of KYC checks, transaction pattern monitoring, and effective transaction thresholds, help merchants avoid payment fraud.

Components of Payment Gateway

As the gateway transactions are between a merchant and clients, a Merchant account and a Payment service provider are needed.

Merchant Account

A merchant account is a designated account specifically for online transactions. One can open it via a payment service provider, a payment gateway vendor, or a financial institution. When a merchant receives a merchant account, he also receives a Merchant ID required for processing your transactions.

Payment Service Provider

When a business charges a customer for a purchase, the payment service provider authorizes the customer’s card details to ensure that there are enough funds in the account to pay.

Issuing Bank

The issuing bank is the bank that is in charge of the customer’s account.

Acquiring Bank

The acquiring bank is the bank that is in charge of the seller’s account. The seller’s account receives money from the customer’s account through a payment gateway transfer.

If they do, the payment processor authorizes the transaction, and the payment is sent to the business’ account. If not, the transaction is rejected.

How do payments work with an online payment gateway?

The steps below explain how payments work with an online payment gateway:

Step 1 – Payment Initiation

The first step is to set up your payment gateway, and the customer enters the payment details on the merchant’s website.

Step 2 – Encryption

With sensitive details entered during the initiation process, the payment gateway encrypts payment information, such as credit card details, to ensure security.

Step 3 – Authorisation and Verification

The payment gateway sends the encrypted payment information to the acquiring bank for authorization. The payment gateway verifies your customer’s card details and checks for the transaction’s legitimacy.

Step 4 – Approval or Decline

The payment is approved if the transaction checks the boxes above and sufficient funds are available. The acquiring bank sends an approval message to the payment gateway, confirming the merchant to complete the transaction.

If any criteria, from authorization to verification to lack of funds, are involved, the customer is notified of the unsuccessful transaction.

Step 5: Settlement

The transaction status will be sent as a notification to the merchant. The payment gateway you use determines how long it takes to confirm your payment.

Most payments, such as UPI and card payments, are confirmed in real time, almost immediately after the transaction is complete, but some may take as long as 7 days if processing errors occur.

Types of Payment Gateways

Multiple payment systems are available for businesses to decide on based on their needs, functionality, and differences. A few of the most prominent ones are mentioned down below,

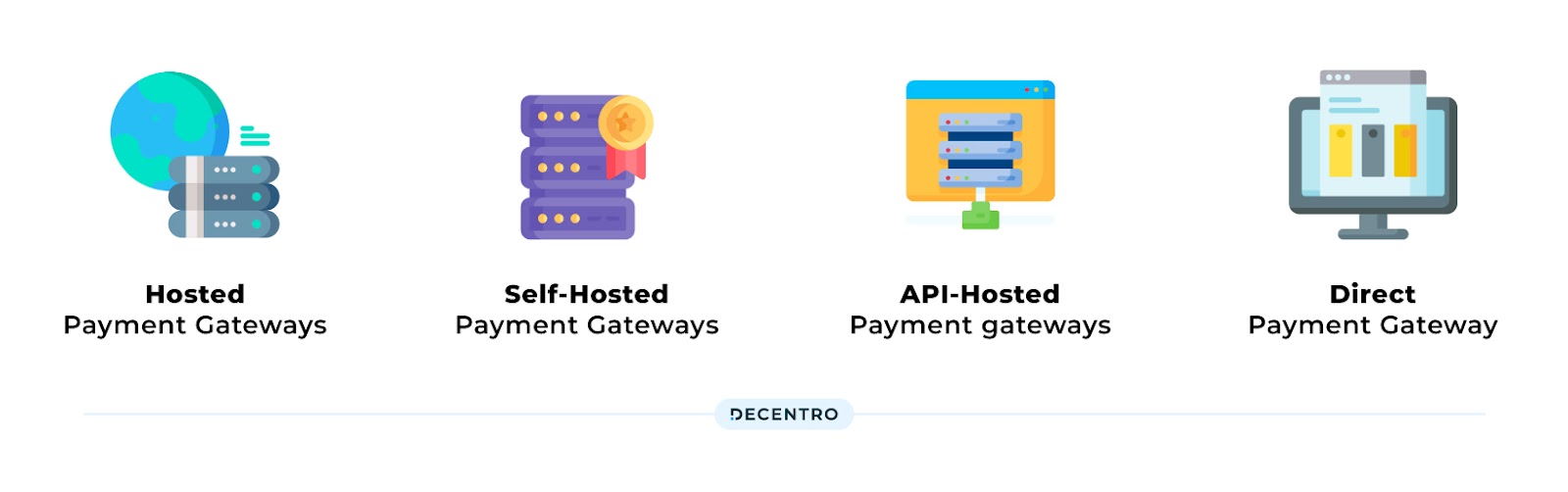

Hosted payment gateway

These gateways mean customers will be redirected from their website’s checkout page to the payment service provider page. Once the payment has been made, the customer is redirected to your website. The hosted segment dominated the market in 2022 and accounted for more than 57.0% share of the global revenue. PayPal globally is one of the most well-known examples where merchants can customize the system to suit their needs. Today, India has numerous hosted payment gateways, from Paytm and Razorpay to Cashfree.

Self-hosted payment gateway

No third party is involved with payment service providers in self-hosted and non-hosted gateways. The eCommerce website owner collects all payment information. All payment details are then collected directly by the eCommerce website owner. These gateways often require customers to enter a secret code to complete the transaction. Shopify Payments is one example of a self-hosted payment gateway.

API-hosted payment gateway

Customers can enter their payment information directly on the merchant’s checkout page. After that, the payment is processed via API or HTTPS queries. This payment method is more user-friendly as customers can use it on their mobile devices. This is the area where players like Decentro thrive.

Direct payment gateway

This type is also known as local bank integration. It redirects customers from your site to the bank’s website, where they can complete the payment process. Customers will receive an email notification from the merchant once payment has been made.

Why should you be looking to integrate a payment gateway?

Consumers are becoming more confident about going completely cashless when making online purchases, even for big-ticket transactions. This trend has grown by 90% over the last few years — surpassing $1.6 trillion by the end of 2022. From accepting credit and debit cards to processing cardless transactions and in-store payments, the best payment gateways can help you maximize conversion rates and deliver the best customer experience, making it an obvious choice for you as a business to jump onto the wagon.

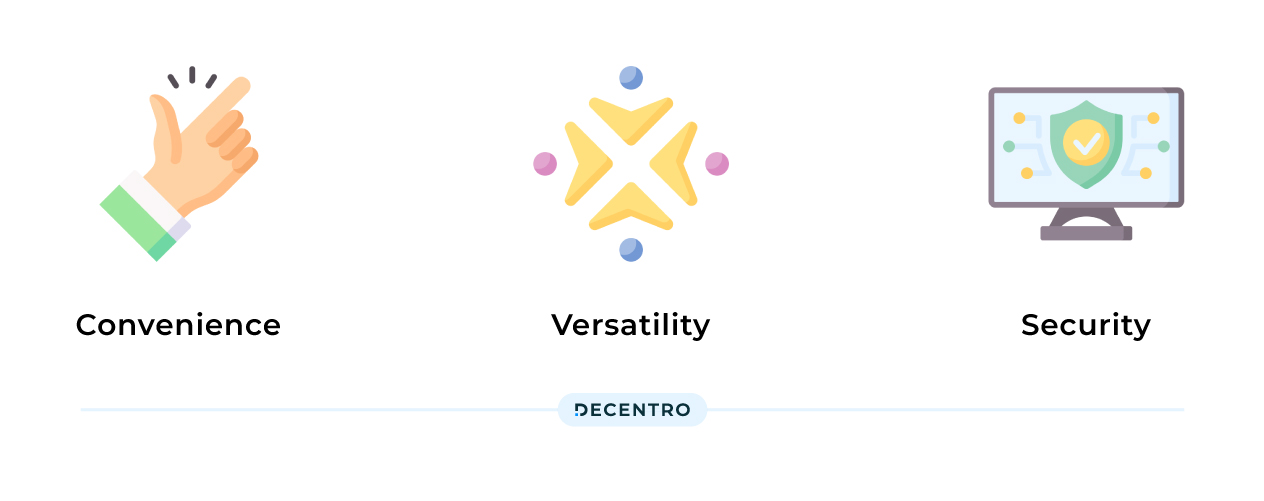

Convenience

There is the expectation of convenience for any consumer of your platform. Payment Gateway Integration means your customers can make purchases anytime. As a business, you have the convenience of tracking expenses and staying on top of your financial records. You get a ready-made solution that starts with your authorization request and ends with the transaction.

Versatility

Different types of transactions are supported by different APIs. With payment gateway integration, customers can pay with more than a bank card. It’s convenient and far-sighted.

Security

Payment gateway integrations severely reduce the risk of fraud, as the customer’s information is securely transmitted to the payment gateway. Many payment gateways provide fraud screening tools to reduce the risk of losing information. These tools include the Card Code Value (CCV), Card Verification Value (CVV), or even the Address Verification Service (AVS). These tools ensure that there are no fraudulent transactions

Characteristics of a payment gateway suitable for you

1. Flexibility

When choosing the right payment gateway provider for your offering, flexibility is a critical feature that both merchants and customers want. If more options are available from your payment gateway integrations, you will require less tweaking.

You should also consider the cost and technical skills required to manage your digital enterprise.

2. Security

Customers demand the highest level of data protection from their payment gateway porviders. High-security gateways are the winners of this race. Encrypted channels allow for the secure transmission of personal information over public channels. Payment gateways must be 3D secure and compliant with PCI data security standards, which is the highest level of security.

3. Fees and Other Charges

Payment gateways charge a fee for every transaction on your site. Fees depend on the volume of transactions, frequency of transactions, and many other factors. You may be charged additional fees for implementing a payment gateway. These fees could include account management costs, withdrawal fees from the bank fees, and fees for setting up an account.

4. Supported currencies

A higher number of supported currencies translates into more customers who transact with you in their native currency without incurring high conversion charges. As a payment gateway provider, this is a differentiator for you.

5. Easy integration

It is the era of custom payment gateways. Look for a payment gateway that allows plugins to integrate with your existing platform seamlessly. With payment integration enabled, you save on the effort of manually updating your records, which also reduces the scope of errors.

Where does Decentro Fit?

It’s no easy feat to blend the convenience of making payments with fraud protection. Nor is it to bring your multiple bank accounts under a single umbrella to make transactions smooth.

Decentro’s banking APIs answer this use case, enabling your business vertical to launch a new product.

Reconcile Payments in Real-time

Reconcile all transactions on your platform in real time with virtual accounts. Enable the same for your customers and help them identify the source of transactions, even failed ones. Automate the reconciliation process to enable your customers to save crucial business hours.

Diversify & Simplify Payments

Offer diverse payment options on your platform for your customers to deploy—for instance, seamless bank transfers such as RTGS, IMPS, and NEFT. In addition, provide customers to share white-label UPI IDs for collecting payments and reinforcing branding.

Launch your BNPL Product

Equip your merchants to offer lending services to their customers. Launch your own Buy Now Pay Later Product to provide credit options for customers in a matter of weeks. Leverage Decentro’s entire lending stack for your platform- manage loans easily, simplify disbursals, and make repayments instant.

Onboard Merchants Digitally in Real-time

Onboard your customers only after running comprehensive Know Your Customer verifications. Run identity verification using PAN, Aadhaar, income checks, and behavioral assessments: multiple data verification points with a single KYC API end-point.

Offer Neobanking Services

Merchants can link their business accounts to your platform and start initiating transactions, thus enabling your customers to bank on your platform. Ride the neobanking wave without spending months running behind compliance and licenses.

Operate your Business Uninterrupted

Put your business on autopilot by leveraging Decentro’s multi-bank architecture. Our backend is superpowered by some of the best banks in the country, such as ICICI bank. This feature is thoughtfully engineered to handle any spikes in volume and balance the load swiftly to enable the same for your business.

The next phase for Payment gateways?

With the need to enhance both the development and end-user experiences, driving any product journey in the organization, the next wave lies in implementing both via a good-quality SDK [Software Development Kit].

The only segue that matters now is how you can access Decentro’s SDKs. With Fintech lenders, gig economy, marketplaces, and wealth managers already leveraging Decentro’s banking APIs to solve their financial woes, there is scope for them to incorporate a more comprehensive devkit in the form of SDKs for their evolving business use cases. Even after integrating, our platform takes care of all upcoming fixes & iterations without any breakage on the workflows.

Is it an investment you are ready to make for your business?