A deep dive into how UPI and PPI are impacting the new age companies in India. We go into the limitations, benefits and the boost to the payments ecosystem.

How UPI And PPI Are Impacting The New Age Companies In India

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

India registered over 23 billion digital transactions worth INR 38.3 lakh crore in the third quarter of 2022-23.

The total online transactions include payments made by the Unified Payments Interface (UPI), debit and credit cards, mobile wallets, Prepaid Payment Instruments (PPIs), etc. UPI-specific transactions also have been recorded over 19.65 billion times, amounting to over INR 32.5 trillion.

What are UPI and PPI?

Unified Payments Interface (UPI) and Prepaid Payment Instruments (PPIs) are two crucial digital payment mechanisms.

UPI allows convenient, secure transactions between two parties. On the other hand, PPI is the interface that enables merchants to accept payments from customers securely. It is a payment protocol integrated with merchant websites and mobile applications.

UPI and PPI have been instrumental in driving India’s digital payments revolution. They have enabled individuals and businesses to make transactions on the go, reducing the need for cash and making payments more secure and convenient.

PPIs permitted in India are divided into closed-system, semi-closed-system, and open-system PPIs.

Closed-System PPIs

Closed-System PPIs are only allowed to facilitate purchases of goods and services from the issuing agency and do not allow cash withdrawals. This category is not considered payment systems that require permission or authorization by the RBI since they cannot intermediate for others.

Semi-Closed PPIs

Semi-Closed PPIs are licensed by banks (permitted by RBI) and non-banks (authorized by RBI). For usage at a group of clearly identified merchant locations/establishments with a unique agreement with the issuer (or issuance through payment aggregators to accept the PPIs as payment instruments). The financial services under this segment include remittance infrastructure, overseas transactions, etc. Whether banks or non-banking institutions permit these PPIs, they do not allow cash withdrawals.

Open-System PPIs

This category of PPIs is licensed by banks with RBI approval and is used by any retailer to pay for services and products, including payment services, remittance services, etc. They also allow cash withdrawals from Business Correspondents (BCs), Point of Sale terminals, and bank ATMs.

Adoption of Virtual Cards in the Payments Ecosystem

The adoption of virtual cards in the payments ecosystem has strengthened the UPI and PPI models. Virtual cards are digital cards offered by banks, financial institutions, and fintech. They are primarily used for making payments online and are linked to the customer’s bank account or wallet. This allows customers to transact without entering their debit/credit card details. Virtual cards are also integrated with UPI and PPI, accelerating payment operations flawlessly. This reduces the need for cash and makes the payment process more secure and convenient for customers and merchants.

How Do New Age Companies Benefit from UPI and PPI

The UPI and PPI model has several benefits for new-age companies in India.

- It enables them to securely store and protect customer data, reducing the risk of data leakage and fraudulent activities.

- Furthermore, the UPI and PPI model allows companies to offer customers convenient payment options.

New-age companies in India are now leveraging the UPI and PPI models to provide customers with a better payment experience. They also implement secure payment processes to offer customers convenient payment options such as virtual cards.

Here are some examples of how new-age startups can unleash the potential of UPI and PPI:

- To use an “Ask” request, companies and individuals may make money requests to others. Payers are informed and must agree to the request for the transfer to proceed.

- For short-term loans, digital wallets can provide speedy lending by completing due diligence through electronic documents. The traditional financial ecosystem lacks this significant aspect that UPI-backed fintech companies can address.

- Companies such as Paytm, PhonePe, Google Pay, Amazon Pay, and Mobikwik have utilized the UPI and PPI models to provide customers with a faster settlement of payments.

- Businesses must integrate PPIs to reach India’s massive smartphone user base of 760 million people, who are likely to purchase online and make payments via mobile wallets and applications.

- Prepaid instruments make it possible to make local and international payments similar to those made through banks but with increased efficiency, flexibility, and security.

Limitations of the Existing Model

Despite their advantages, the existing model has their limitations.

One of the major limitations is that UPI and PPI are not integrated. Customers have to switch between UPI and PPI for transactions, which can be time-consuming and inconvenient.

Plus, existing UPI and PPI models do not provide merchants with a secure way of collecting payments. This means that the customer’s payment information is not protected, which can lead to data leakage and fraudulent activities.

RBI Intervention

RBI’s intervention has enabled new-age companies in India to benefit from UPI and PPI. The following key actions, which became effective on March 31, 2022, were announced at the 2021 RBI monetary policy review:

- PPIs can provide users with Real-Time Gross Settlement (RTGS) and National Electronic Funds Transfer (NEFT) options.

- The entire KYC PPIs must be interoperable.

- For a PPI license, companies must have a positive net worth of ₹ 5 Cr at the time of approval registration, up from INR 2 Cr before. This must be ₹ 15 Cr during the third fiscal year of gaining RBI approval.

RBI permits PPIs and approves them with minimal hassles, known as a Small PPI. These are designed for minimum implementation and require the customer to offer simple details like cellular and e-KYC identity ranges. An in-depth procedure like biometric or Video KYC converts a wallet into a complete KYC-ed PPI, unlocking a digital wallet’s actual strength.

With the revolutionary PPI rules introduced by the Reserve Bank of India (RBI), the idea is for all businesses in India to embrace PPI to maximize profits. It has also strengthened the UPI and PPI models by enabling banks, financial institutions, and fintech to store and securely protect customer data. This has minimized the risk of data leakage and fraudulent activities and has made the payments ecosystem more secure.

Impact of UPI and PPI on the Payments Ecosystem

The Payments Council of India (PCI) has forecast that digital payments in the nation might expand by 30%–40% over the next five years in response to RBI’s announcement related to PPI.

Digital transactions in India have expanded rapidly in recent years as smartphones have become more easily available. The introduction of digital stacks like UPI and PPIs has increased domestic remittance restrictions and the acceptance of international inward remittances. As a result, participants in the industry have been able to digitize retail payments, which were previously done largely with cash.

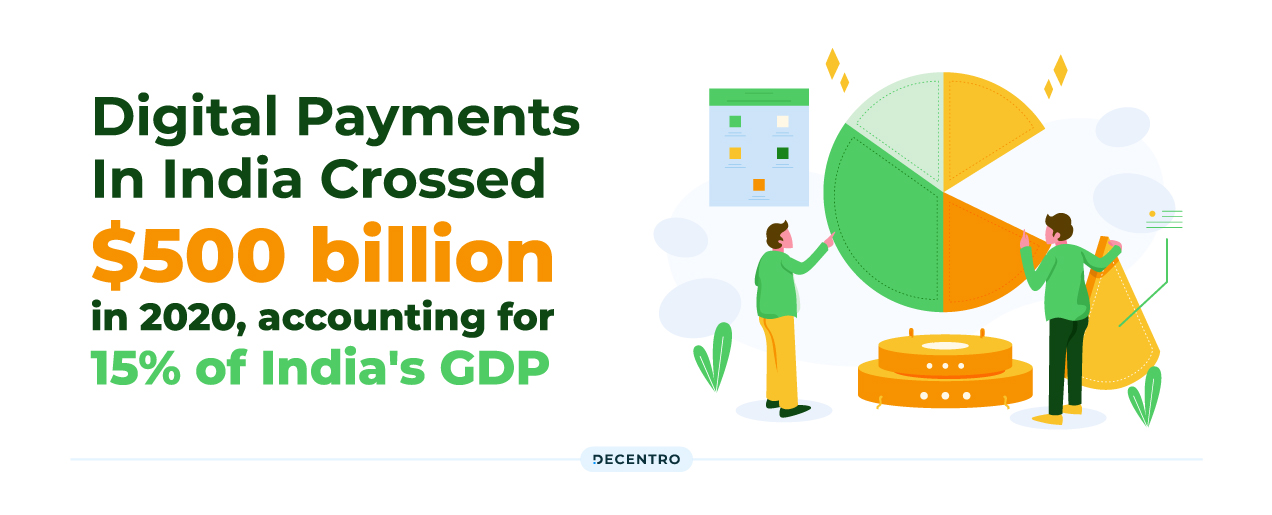

According to recent research by Google and Boston Consulting Group, the digital payments sector in India is expected to reach $500 billion by 2020, accounting for 15% of India’s GDP. The newly established criteria for interoperability across different PPIs seek to strengthen the industry even further by making digital transactions a quick, easy, and feasible choice for users.

Data reveal a more than 500% rise in businesses taking digital means of payment during the first half of the fiscal year 2021 vis-a-vis the second half of the fiscal year 2019; UPI alone exhibits a more than 1200% growth over the same period. Payment tap point deployment has also increased significantly. With the paradigm shift in consumer attitude toward adopting digital and touchless ways of payment, owing in part to COVID-19, there has been a 50% rise in mobile banking users, showing the incorporation of first-time users into the digital fold.

RBI’s Payments Vision 2025 presents five targets: Integrity, Inclusion, Innovation, Institutionalisation, and Internationalisation. Resilience to operational and security concerns would continue to be at heart to withstand and recover from the evolving threat landscape. These aspects will positively impact UPI and PPI operations.

Conclusion

Businesses anticipate being selective in their approach, which might result in consolidation soon, given the regulatory burden still placed on fintech and the Reserve Bank of India’s (RBI) efforts to regulate different aspects of the payment industry.

However, the bottom line is that the UPI and PPI model has facilitated companies with technical synchronization and efficient payment system. It has also enabled them to leverage the latest technologies, such as virtual cards, to strengthen the payments ecosystem further. Companies may use the advanced payment infrastructure to achieve broader objectives like financial inclusion.

This is where an organization like Decentro becomes your go-to partner with its extensive product suite, developed in tandem with the dynamic nature of the regulatory body in India.

An extensive and compliant lending stack, an entire payment solution, KYC onboarding stack, all available in simple plug-and-play APIs. Curious to explore more?