Discover what IBAN is and why it matters in global banking. Simplify cross border payments with this essential guide and learn how Decentro can help you get started.

What is IBAN? How Does It Work?

Avi is a full-stack marketer on a mission to transform the Indian fintech landscape.

Table of Contents

An IBAN becomes essential for businesses working with international partners and suppliers. But what exactly is an IBAN, and how is it structured? Read this guide to learn more about IBAN’s structure, uses, and benefits.

What is an IBAN

So, what’s an IBAN? It’s like a global ID for your bank account, standing for “International Bank Account Number.” Think of it as your account’s passport number that can be used worldwide. If you need to open a bank account in countries like Germany, you’ll need an IBAN. If you’re sending or receiving money internationally, your IBAN can be crucial for smooth transactions, including most e-commerce payouts.

Over 70 countries use IBANs today, except the US, Canada, and Australia. When you use an IBAN for payments, banks check its format to ensure the transaction’s legitimacy, making transactions quick—often within minutes. IBANs are key for direct debits and instant transfers, though funds might take a day or two to appear in the recipient’s account.

Purpose of an IBAN

European union countries employed disparate bank account numbering systems before introducing International Bank Account Numbers (IBAN). This inconsistency often led to errors during cross-border financial transactions, resulting in funds being erroneously transferred to incorrect accounts. Resolving such errors necessitated additional fees and considerable time.

In response to these challenges, the International Organization for Standardization (ISO) proposed a standardised system for global financial transfers in 1997, which is today recognised under the standard ISO 13616-2:2007.

Since then, implementing the IBAN system has significantly reduced the incidence of errors in international wire transfers and other financial operations. Harmonising account number formats across participating countries has facilitated easier and more reliable international transfers. Thanks to the implementation of IBANs, the errors during international money transfers have reduced to under 0.1% of total payments.

Despite these improvements, the IBAN system cannot address specific issues, such as the variability of foreign exchange rates.

Structure of an IBAN

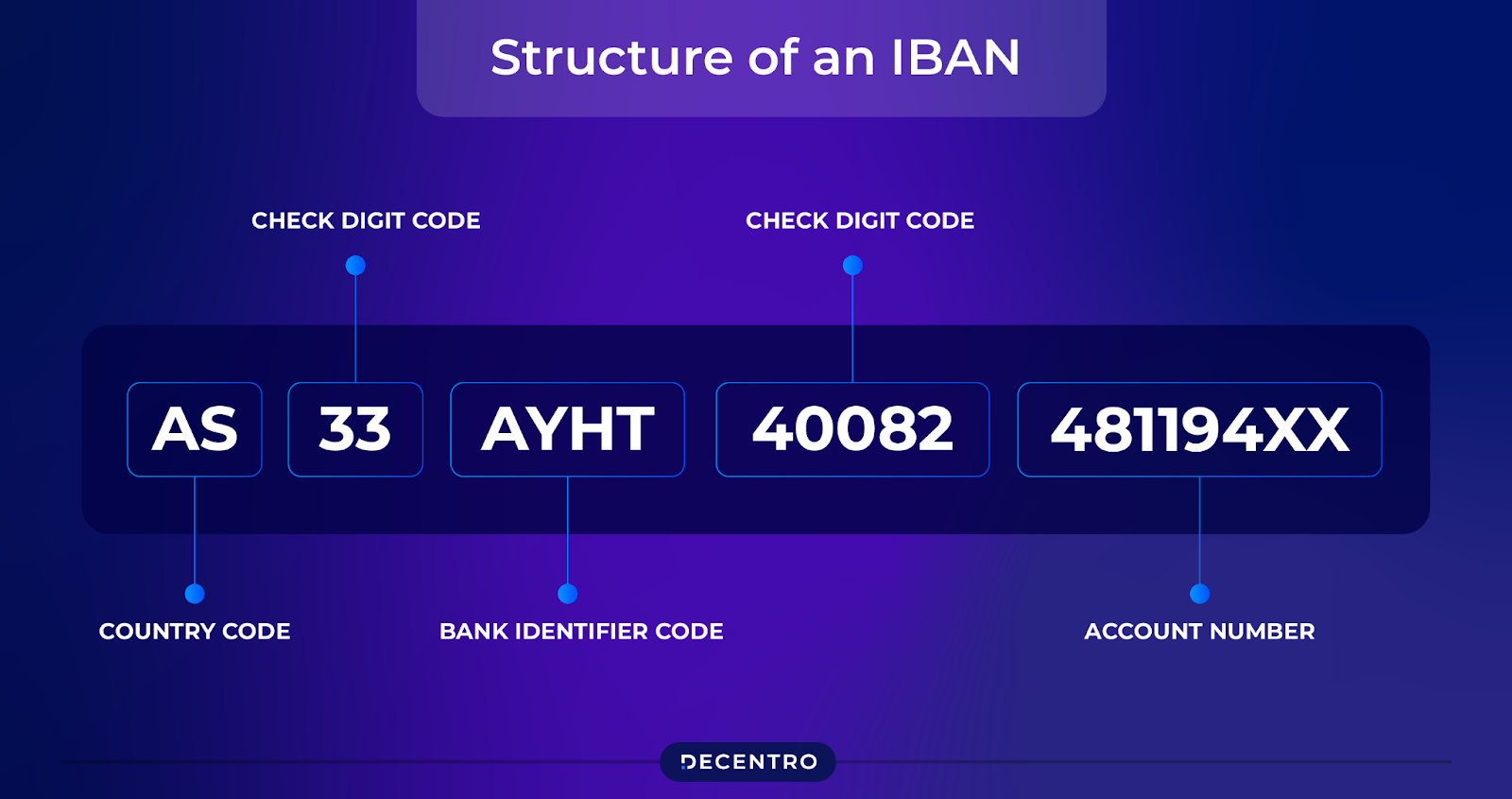

An IBAN, which can contain up to 34 alphanumeric characters, adheres to a specific format. In the UK, IBANs are 22 digits long and include the country code, check digits, bank code, sort code, and account number.

- Country code (2 letters): These letters show which country your bank is in, like “GB” for the United Kingdom.

- Check digits (2 numbers): These numbers, created by a special formula, help check if the IBAN is right.

- Bank code (4 characters): This code points out your bank.

- Bank branch (6 numbers): This sort code tells us which branch of the bank you use.

- Account number (8 numbers): This is your bank account number. If it’s shorter than 8 numbers, we add zeros in front to make it 8 digits long.

Example of an IBAN

Each country has its own IBAN format. For example, let’s look at an IBAN for Germany. An IBAN in Germany consists of 22 digits: 2-letter country code, 2 digit check number, 8 digits for the bank code and 10 digits for the bank account number.

Therefore, an IBAN example in Germany would be DE89370400440532013000. Here, the country code is DE, the check digits are 89, the bank code is 37040044, and the bank account number is 0532013000.

The format of an IBAN remains consistent, though its length differs by country. For instance, an IBAN may extend up to 36 characters, including the country code and an additional 34 digits in certain countries. Specifically, an IBAN consists of 22 characters in Germany and the UK, while France includes 27 digits, and Spain includes 24. Regardless of these variations, an IBAN is universally accepted.

How to find my IBAN

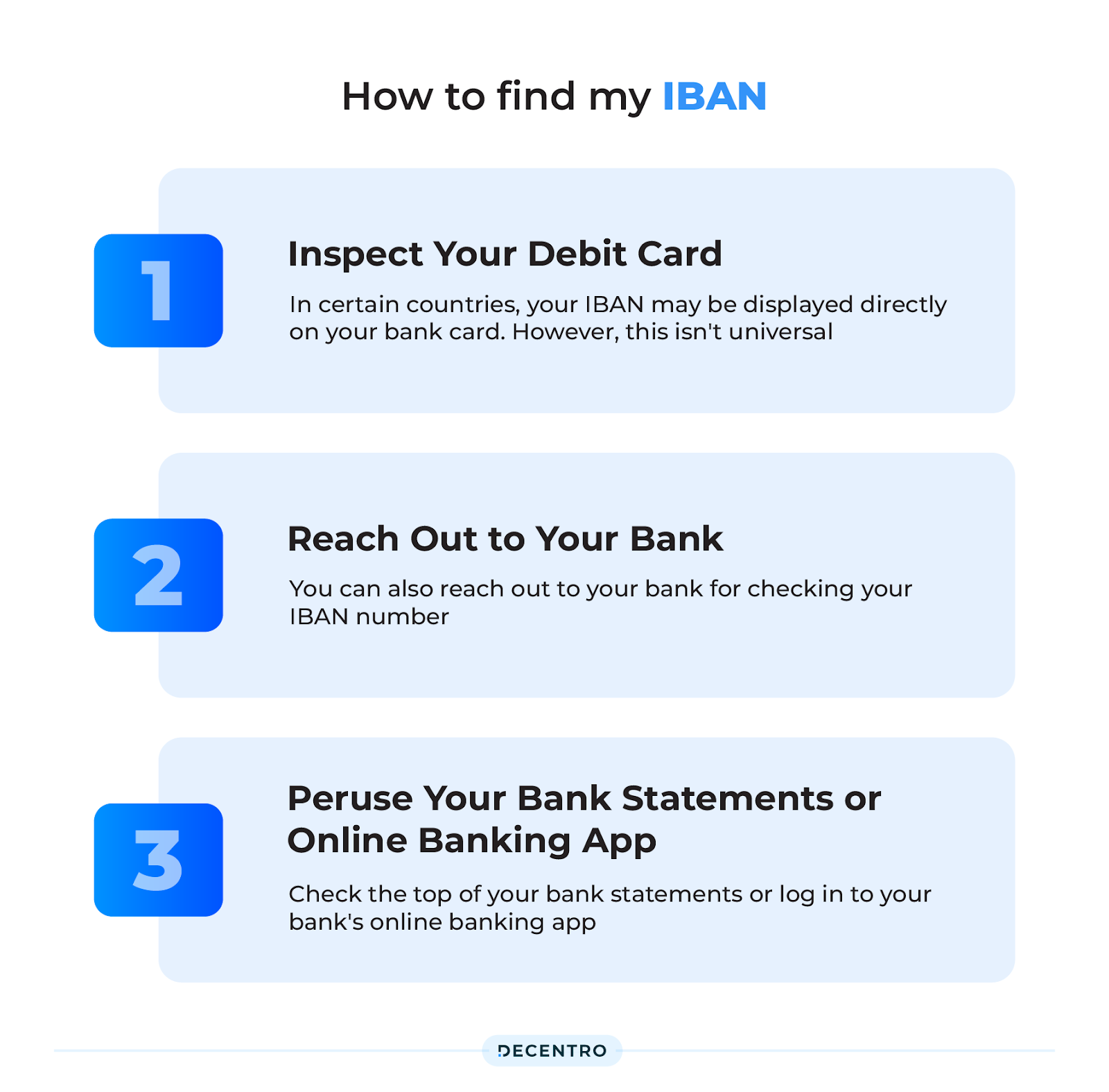

Discovering your IBAN can sometimes feel like finding a needle in a haystack, but you can discover your IBAN with these helpful tips:

- Inspect Your Debit Card: In certain countries, your IBAN number may be displayed directly on your bank card. However, this isn’t universal.

- Reach Out to Your Bank: You can also reach out to your bank for checking your IBAN number.

- Peruse Your Bank Statements or Online Banking App: Check the top of your bank statements or log in to your bank’s online banking app.

Alternatively, You can use the IBAN registry or an IBAN calculator to find your IBAN.

IBAN – Safety and Security

From the consumer’s perspective, utilising an IBAN (International Bank Account Number) introduces an added layer of security, safeguarding their funds effectively. This security measure facilitates the validation of bank account details, significantly minimising the likelihood of fraudulent activities and unauthorised fund access. Moreover, IBAN allows consumers to confirm the receipt of payments into their accounts, offering transparency and reassurance regarding their financial transactions.

Therefore, IBAN is a crucial instrument in enhancing payment security and efficiency. It offers a robust layer of protection against fraud and unauthorised fund access for businesses and consumers, streamlining payment transactions and curtailing error-related costs.

What is the IBAN Registry?

The IBAN (International Bank Account Number) registry is a comprehensive directory that contains important information on the national bank account numbering systems of countries that participate in the IBAN standard. Managed by SWIFT (the Society for Worldwide Interbank Financial Telecommunication), the registry aims to support implementing and using the IBAN standard globally.

The IBAN registry provides details such as the structure of the bank account number for each country, the length of the IBAN, bank identifier positions within the IBAN, and examples of the national bank account numbering formats compliant with the IBAN standard. This information is crucial for banks, financial institutions, and businesses involved in international transactions, as it helps ensure that cross-border payments are processed smoothly, accurately, and securely.

The registry is regularly updated to reflect national banking system changes or include new countries adopting the IBAN standard.

Which countries use IBAN?

IBANs are used in most European Union countries and a number of non-European countries. The table below details the countries represented in the IBAN, alongside the account number length specific to each country.

| Abbreviation | Sepa | Length | Example | |

| Albania | WQ | No | 28 | AL35202111090000000001234567 |

| Andorra | AD | Yes | 24 | AD1400080001001234567890 |

| Austria | WP | Yes | 20 | AT483200000012345864 |

| Azerbaijan | AZ | No | 28 | AZ96AZEJ00000000001234567890 |

| Bahrain | BH | No | 22 | BH02CITI00001077181611 |

| Belarus | CITY | No | 28 | BY86AKBB10100000002966000000 |

| Belgium | BE | Yes | 16 | BE71096123456769 |

| Bosnia and Herzegovina | BA | No | 20 | BA393385804800211234 |

| Brazil | BR | No | 29 | BR1500000000000010932840814P2 |

| Bulgaria | BG | Yes | 22 | BG18RZBB91550123456789 |

| Costa Rica | CR | No | 22 | CR23015108410026012345 |

| Croatia | HR | Yes | 21 | HR1723600001101234565 |

| Cyprus | CY | Yes | 28 | CY21002001950000357001234567 |

| Czech Republic | CZ | Yes | 24 | CZ5508000000001234567899 |

| Denmark | DK | Yes | 18 | DK9520000123456789 |

| Dominican Republic | DO | No | 28 | DO22ACAU00000000000123456789 |

| Egypt | EC | No | 29 | EG800002000156789012345180002 |

| El Salvador | SV | No | 28 | SV43ACAT00000000000000123123 |

| Estonia | EE | Yes | 20 | EE471000001020145685 |

| Faroe Islands | FO | No | 18 | FO9264600123456789 |

| Finland | FI | Yes | 18 | FI1410093000123458 |

| France | FR | Yes | 27 | FR7630006000011234567890189 |

| Georgia | GE | No | 22 | GE60NB0000000123456789 |

| Germany | DE | Yes | 22 | DE75512108001245126199 |

| Gibraltar | GI | Yes | 23 | GI04BARC000001234567890 |

| Greece | GR | Yes | 27 | GR9608100010000001234567890 |

| Greenland | GL | No | 18 | GL8964710123456789 |

| Guatemala | GT | No | 28 | GT20AGRO00000000001234567890 |

| Holy See (the) | VA | Yes | 22 | GT20AGRO00000000001234567890 |

| Hungary | HU | Yes | 28 | HU93116000060000000012345676 |

| Iceland | IS | Yes | 26 | IS750001121234563108962099 |

| Iraq | IQ | No | 23 | IQ20CBIQ861800101010500 |

| Ireland | IE | Yes | 22 | IE64IRCE92050112345678 |

| Israel | IL | No | 23 | IL170108000000012612345 |

| Italy | IT | Yes | 27 | IT60X0542811101000000123456 |

| Jordan | JO | No | 30 | JO71CBJO0000000000001234567890 |

| Kazakhstan | KZ | No | 20 | KZ563190000012344567 |

| Kosovo | XK | No | 20 | XK051212012345678906 |

| Kuwait | KW | No | 30 | KW81CBKU0000000000001234560101 |

| Latvia | LV | Yes | 21 | LV97HABA0012345678910 |

| Lebanon | LB | No | 25 | LB92000700000000123123456123 |

| Libya | LY | No | 25 | LY38021001000000123456789 |

| Liechtenstein | LI | Yes | 21 | LI7408806123456789012 |

| Lithuania | LT | Yes | 20 | LT601010012345678901 |

| Luxembourg | LU | Yes | 20 | LU120010001234567891 |

| Malta | MA | Yes | 31 | MT31MALT01100000000000000000123 |

| Mauritania | MR | No | 27 | MR1300020001010000123456753 |

| Mauritius | MU | No | 30 | MU43BOMM0101123456789101000MUR |

| Moldova | MD | No | 24 | MD21EX000000000001234567 |

| Monaco | MC | Yes | 27 | MC5810096180790123456789085 |

| Montenegro | ME | No | 22 | ME25505000012345678951 |

| Netherlands | NL | Yes | 18 | NL02ABNA0123456789 |

| North Macedonia | MK | No | 19 | MK07200002785123453 |

| Norway | NO | Yes | 15 | NO8330001234567 |

| Pakistan | PK | No | 24 | PK36SCBL0000001123456702 |

| Palestine | PS | No | 29 | PS92PALS000000000400123456702 |

| Poland | PL | Yes | 28 | PL10105000997603123456789123 |

| Portugal | PT | Yes | 25 | PT50002700000001234567833 |

| Qatar | QA | No | 29 | QA54QNBA000000000000693123456 |

| Romania | RO | No | 24 | RO09BCYP0000001234567890 |

| St. Lucia | LC | No | 32 | LC14BOSL123456789012345678901234 |

| San Marino | ST | Yes | 27 | SM76P0854009812123456789123 |

| Sao Tome and Principe | ST | No | 25 | ST23000200000289355710148 |

| Saudi Arabia | SA | No | 24 | ST23000200000289355710148 |

| Serbia | RS | No | 22 | RS35105008123123123173 |

| Seychelles | SC | No | 31 | SC52BAHL01031234567890123456USD |

| Slovak Republic | SK | Yes | 24 | SK8975000000000012345671 |

| Slovenia | SI | Yes | 19 | SI56192001234567892 |

| Spain | ES | Yes | 24 | ES7921000813610123456789 |

| Sudan | SD | No | 18 | SD8811123456789012 |

| Sweden | SE | Yes | 24 | SE7280000810340009783242 |

| Switzerland | CH | Yes | 21 | CH5604835012345678009 |

| Timor-Leste | TL | No | 23 | TL380010012345678910106 |

| Tunisia | TN | No | 24 | TN5904018104004942712345 |

| Turkey | TR | No | 26 | TR320010009999901234567890 |

| Ukraine | USA | No | 29 | UA903052992990004149123456789 |

| United Arab Emirates | AE | No | 23 | AE460090000000123456789 |

| United Kingdom | GB | Yes | 22 | GB33BUKB20201555555555 |

| Virgin Islands, British | VG | No | 24 | VG21PACG0000000123456789 |

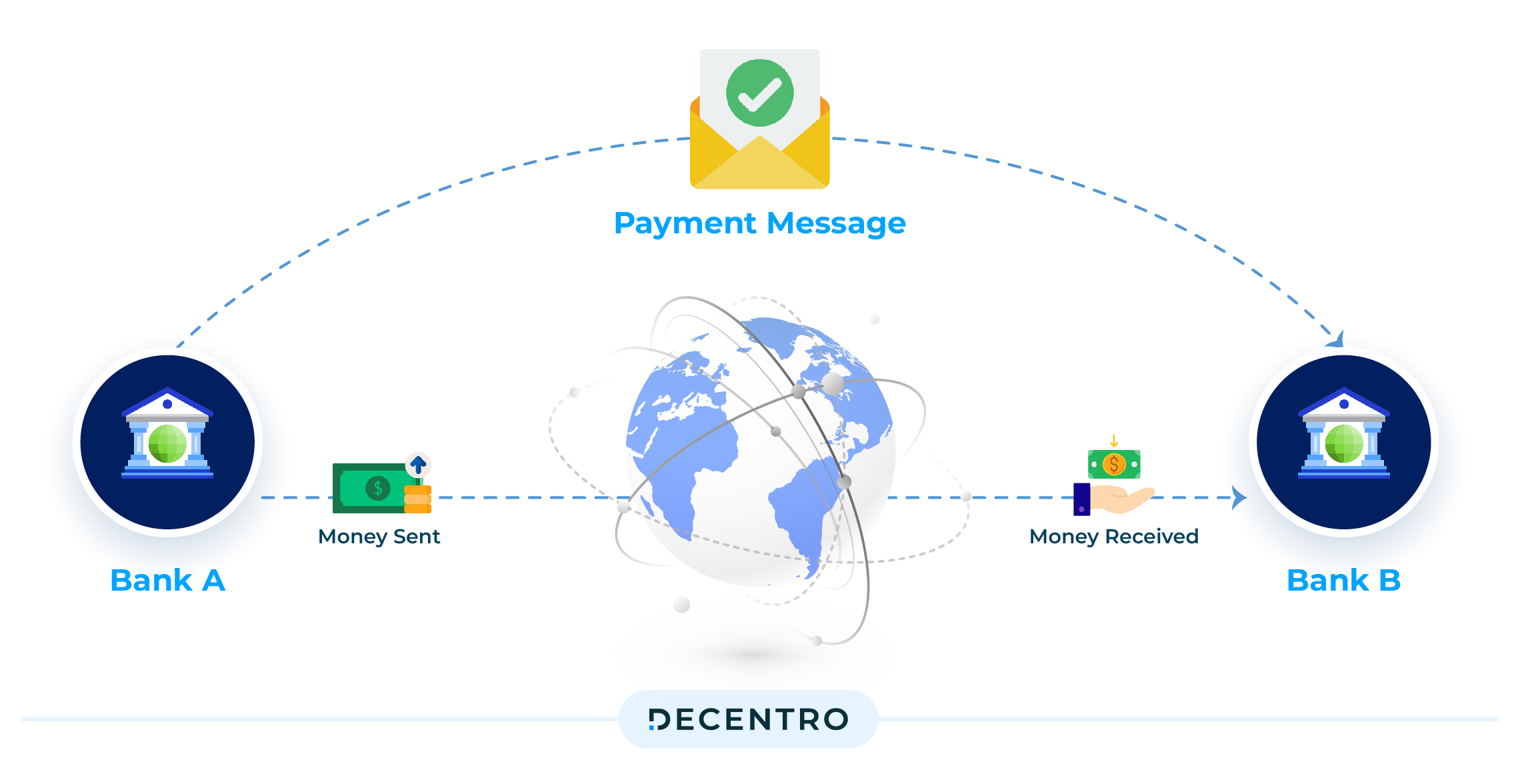

How does an IBAN work?

When you make a cross-border payment transaction, your bank processes your IBAN. The bank’s payment system looks at your IBAN, checking each letter and number against its records. It’s like a digital handshake, confirming both your and the recipient’s accounts. In the background, specific algorithms verify your account details, ensuring everything adds up. If all checks out, your payment transaction is approved and sent to its destination.

Cross-Border Payment Methods

In international finance, cross-border payments are pivotal, facilitating global trade and personal transactions across countries. Among the myriad methods available, three stand out for their reliability, widespread use, and regulatory compliance: SEPA, SWIFT, and BIC. Understanding these systems is essential for navigating the complex landscape of international payments.

SEPA (Single Euro Payments Area)

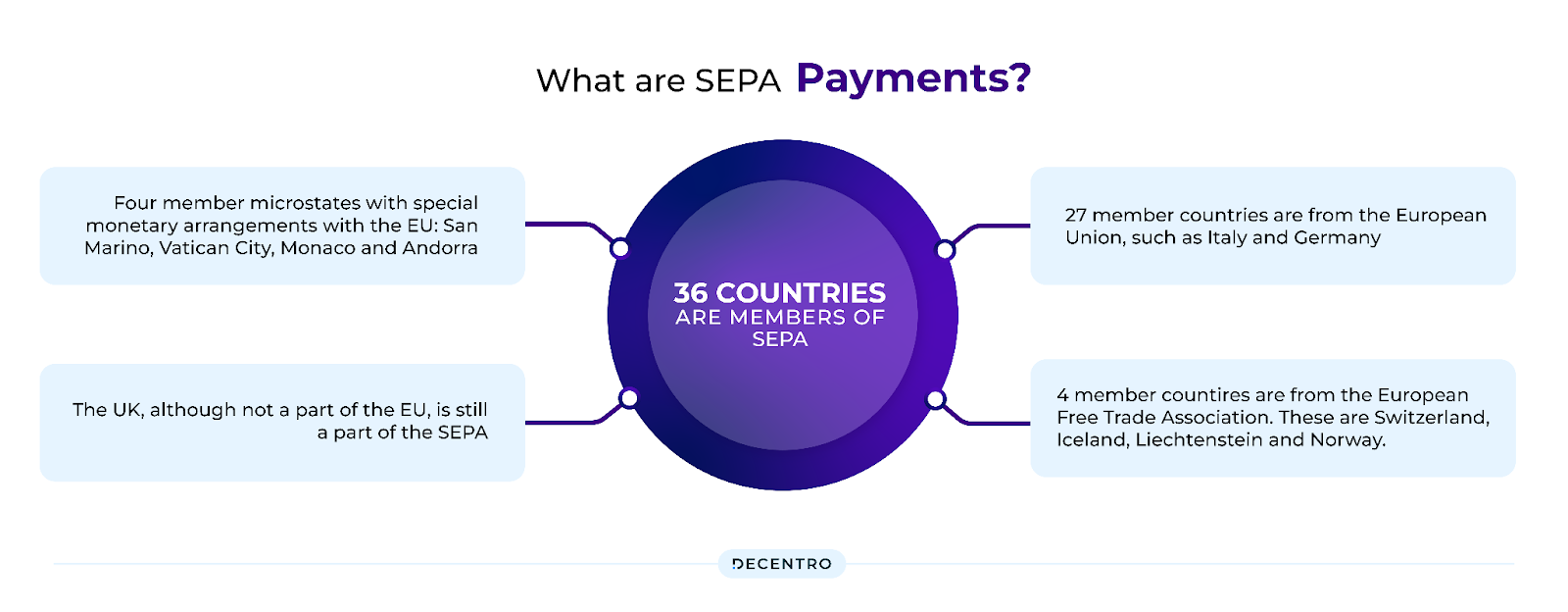

SEPA is an initiative by the European Union to simplify bank transfers denominated in euros. It encompasses 36 countries and allows for efficient, low-cost transfers within this zone, akin to domestic payments. SEPA aims to enhance the efficiency of cross-border payments, including credit transfers, direct debits, and card payments. SEPA processes over 46 billion electronic payments annually, signifying its pivotal role in European transactions.

SWIFT (Society for Worldwide Interbank Financial Telecommunication)

SWIFT is a vast messaging network that financial institutions use to transmit information and instructions through a standardised code system securely. It facilitates various financial transactions, including cross-border payments, by providing a reliable and secure communication mechanism rather than directly handling funds transfer. As of December 2022, SWIFT had recorded an average of 44.8 million FIN messages (payments and securities transactions) per day, a year on year rise of 6.6%.

BIC (Business Identifier Code)

BIC, also known as SWIFT codes, are unique identifiers for banks and financial institutions globally, playing a crucial role in international transactions. While often mentioned in conjunction with SWIFT, BICs are specifically the codes used to identify the specific banks involved in a transaction, ensuring that payments reach the correct institution. More than 11,000 banks, payment, securities and treasury market infrastructures, broker/dealers, custodians, investment managers, fund participants, and corporates are part of the SWIFT/BIX network currently.

Difference between IBAN and SEPA

The Single Euro Payments Area (SEPA) is an initiative designed to facilitate digital financial transactions across the European Union. It encompasses member states such as Spain, Ireland, Hungary, and the United Kingdom and non-EU countries such as Norway, Iceland, Switzerland, and Liechtenstein.

SEPA is distinguished by its exclusive use of the Euro for transactions, in contrast to the International Bank Account Number (IBAN) system, which is utilised by over 60 countries and permits transactions in multiple currencies.

IBAN vs SWIFT vs BIC

A SWIFT code is a unique identifier that directs bank messages across the Society for Worldwide Interbank Financial Telecommunication (SWIFT) network. These codes range from 11 to 18 characters, blending letters and numbers, and adhere to the ISO 9362 standard for formatting.

BICs are essentially the same as SWIFT codes. The terms are interchangeable, meaning the codes provide identical information regardless of the label. In banking contexts, “SWIFT code” and “BIC code” are used synonymously to refer to this standard.

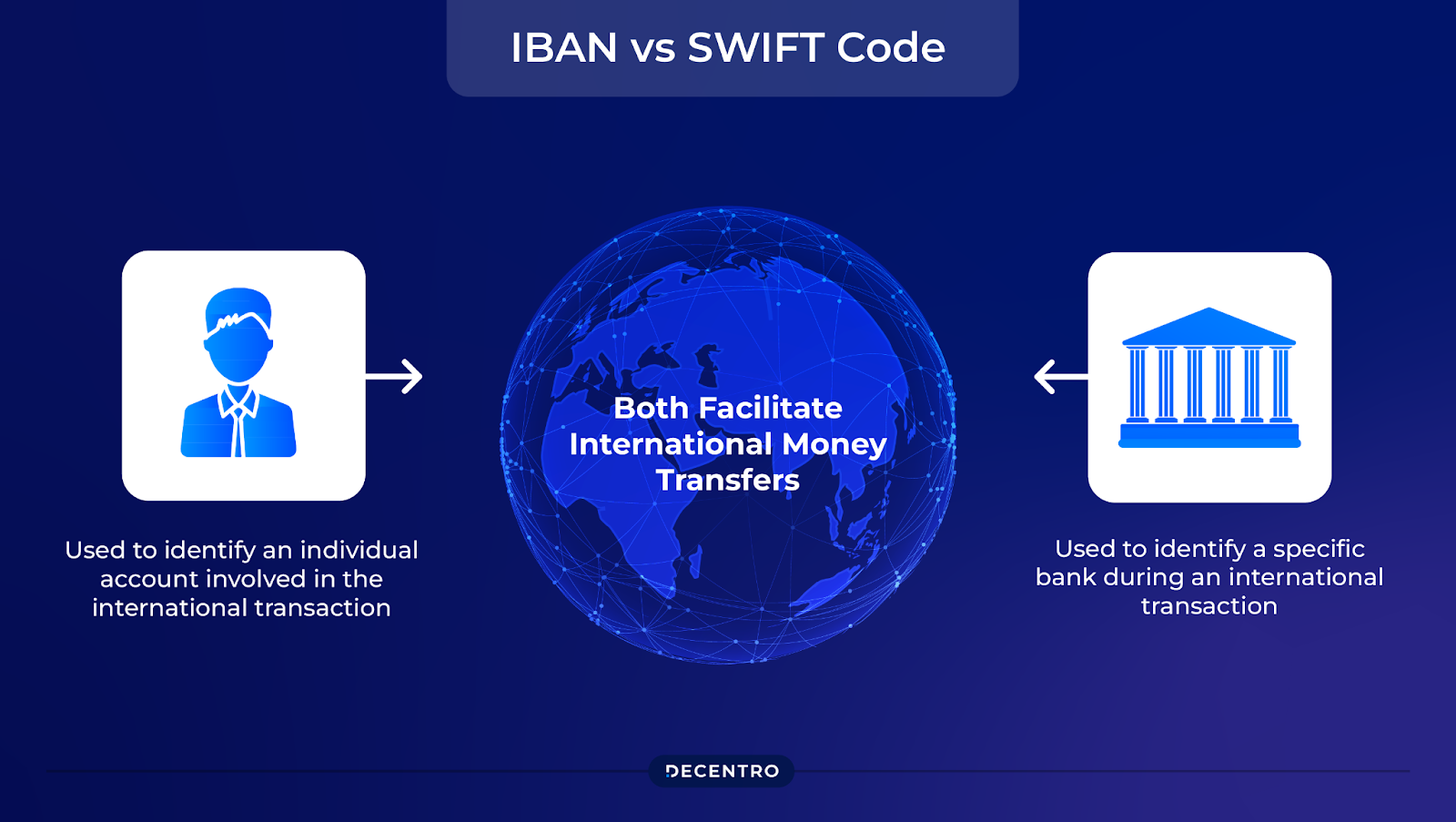

A SWIFT code is used to identify a specific bank during an international transaction. In contrast, an IBAN is used to identify an individual account involved in international transactions. Additionally, SWIFT codes facilitate the exchange of messages between banks, while IBANs ensure transactions reach the correct banks and specific accounts.

Though IBANs play a crucial role, their usage is less widespread than SWIFT codes. Primarily used in Europe and the Middle East, IBANs are less common in the Americas and Asia. When sending money to countries outside the IBAN system, a combination of a SWIFT code and a different account numbering system akin to IBAN may be required.

While it’s sometimes possible to process a bank transaction with just an IBAN or a SWIFT code, these two pieces of information are frequently used together. This dual approach provides comprehensive routing details and allows for cross-verification, ensuring smooth and accurate transactions.

Conclusion

How do you, as a business, venture into seamless international banking?

The resilience and adaptability of the IBAN system, essential for streamlining international payments and banking interactions, are evident. As a universal standard, IBAN facilitates the efficient processing of cross-border transactions, making it an invaluable tool for businesses aiming to penetrate the global market.

Understanding the intricacies of international banking, including the IBAN system, its regulatory environment, and the technical infrastructure that underpins it, is crucial for businesses looking to expand their global operations.

Navigating the complexities of global payments independently can be daunting. Hence, partnering with a knowledgeable and reliable entity ensures compliance, efficiency, and smoothness in your international financial transactions.

Decentro offers a robust solution for businesses embracing global payments. With Decentro’s integration, companies can effortlessly manage both domestic and international transactions, including those requiring IBAN for countries where it is applicable. This encompasses leveraging Decentro’s capabilities for cross-border payments in various countries and currencies, thus simplifying the payment process across borders. You can also use Decentro’s Global Payouts offering to disburse funds across 160+ countries.

Utilise Decentro’s capabilities to unlock the full potential of your business’s international payment processes.

How can Decentro facilitate your journey into global payments with IBAN integration?

Frequently Asked Questions

What is the full form of IBAN?

IBAN is International Bank Account Number, which can be used when making or receiving international payments.

How many digits does an IBAN have?

An IBAN number contains up to 34 alphanumeric characters. It is prefaced by a two-character country code, two check digits, and a Basic Bank Account Number (BBAN) that contains specific bank and account details. The format of the BBAN portion varies from country to country.

What happens if I put in the wrong IBAN?

If the IBAN is wrong, transactions may be rejected or delayed. The transfer may not reach the intended recipient, and the funds could be returned to the sender after a delay. It’s important to double-check the accuracy of the IBAN before initiating any international transfers to avoid potential problems.

Do all banks have IBAN?

Not all banks carry an IBAN number. IBANs are most commonly used in Europe, but some countries outside Europe also use IBANs.

How can you identify a bank from an IBAN?

You can use the bank code contained within the IBAN to identify a given bank. You can find the bank code after the two-letter country code and the two control digits in the IBAN’s fifth section. The bank code length may vary from country to country.

Is it possible to find the SWIFT code from the IBAN?

IBAN (International Bank Account Number) does not contain a BIC (Bank Identifier Code) or SWIFT code it. These are two separate and distinct pieces of information used in international banking transactions.

Can I change my IBAN?

IBAN can be changed but only for specific circumstances, including bank reorganization, bank branch change, bank account reopening, etc.

Can I share my IBAN with others?

Generally, yes. You can share your IBAN with others to accept payments. They would need several more details to withdraw money from your account depending on which bank you are using.

Do I need both BIC and IBAN?

Often, alongside the IBAN, you’ll also require the recipient’s SWIFT code. Combining these identifiers enables banks to locate your recipient’s bank and their exact account precisely. For transactions with countries not adopting the IBAN system, the SWIFT code becomes the sole requisite for identifying the receiving bank.