Understand penny testing, penny drop verification, and how businesses verify bank accounts instantly to prevent fraud and payout failures.

Received ₹1 from Decfin? Here’s How Penny Drop Actually Works

A true blue millennial trying to engineer her full time-career around the world of content. How cliché is that?

Table of Contents

Summary

If you recently noticed a small credit of ₹1 — or even ₹0.01 — from “Decfin Tech Private Limited” in your bank account, there’s no need to panic. You haven’t been hacked, and no, it isn’t a glitch. You are on the receiving end of one of India’s most widely used, and least understood bank verification methods: penny drop verification.

This article explains what penny testing is, why businesses use it, how the process works end-to-end, and why it has become a foundational layer of India’s digital financial infrastructure. Whether you’re a consumer who received an unexpected credit or a founder building a FinTech product, this guide breaks it all down simply.

Setting the Stage: India’s Digital Finance Boom

India’s digital payments ecosystem is growing at a pace few could have anticipated a decade ago. The country now processes over 14 billion UPI transactions per month, and digital lending, neo-banking, and investment platforms are onboarding millions of new users every year.

With this scale comes a critical question: how do you verify that a bank account actually belongs to the person who claims it does?

Getting this wrong is costly. A misrouted payout, a fraudulent account, or a failed disbursement can mean money sent to the wrong place — and often, no way to get it back. In FY2024, India reported over ₹1.75 lakh crore in digital payment fraud attempts. The stakes are high.

Penny drop verification is one of the most reliable, real-time answers to this problem.

What Is Penny Drop Verification?

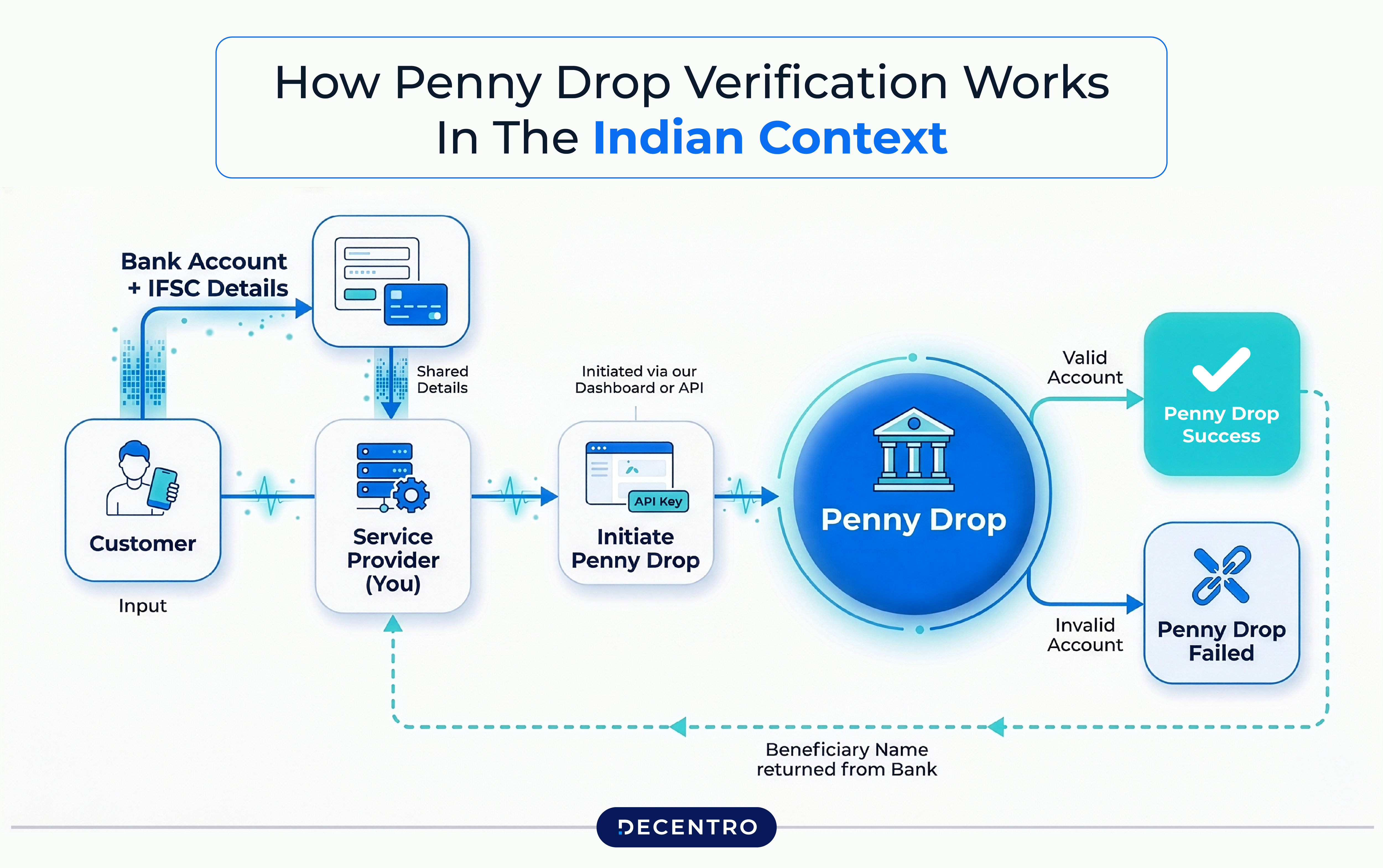

Think of penny drop verification as a “live handshake” between a business and your bank account.

Here’s the simplest way to understand it: when a financial platform needs to confirm that the bank account number and IFSC code you provided are real, active, and actually belong to you, they send a tiny amount, typically ₹1, or sometimes even ₹0.01, to that account via IMPS (Immediate Payment Service).

If the money lands successfully and the account holder’s name returned by the bank matches the name you provided during onboarding, the account is verified. It’s that simple.

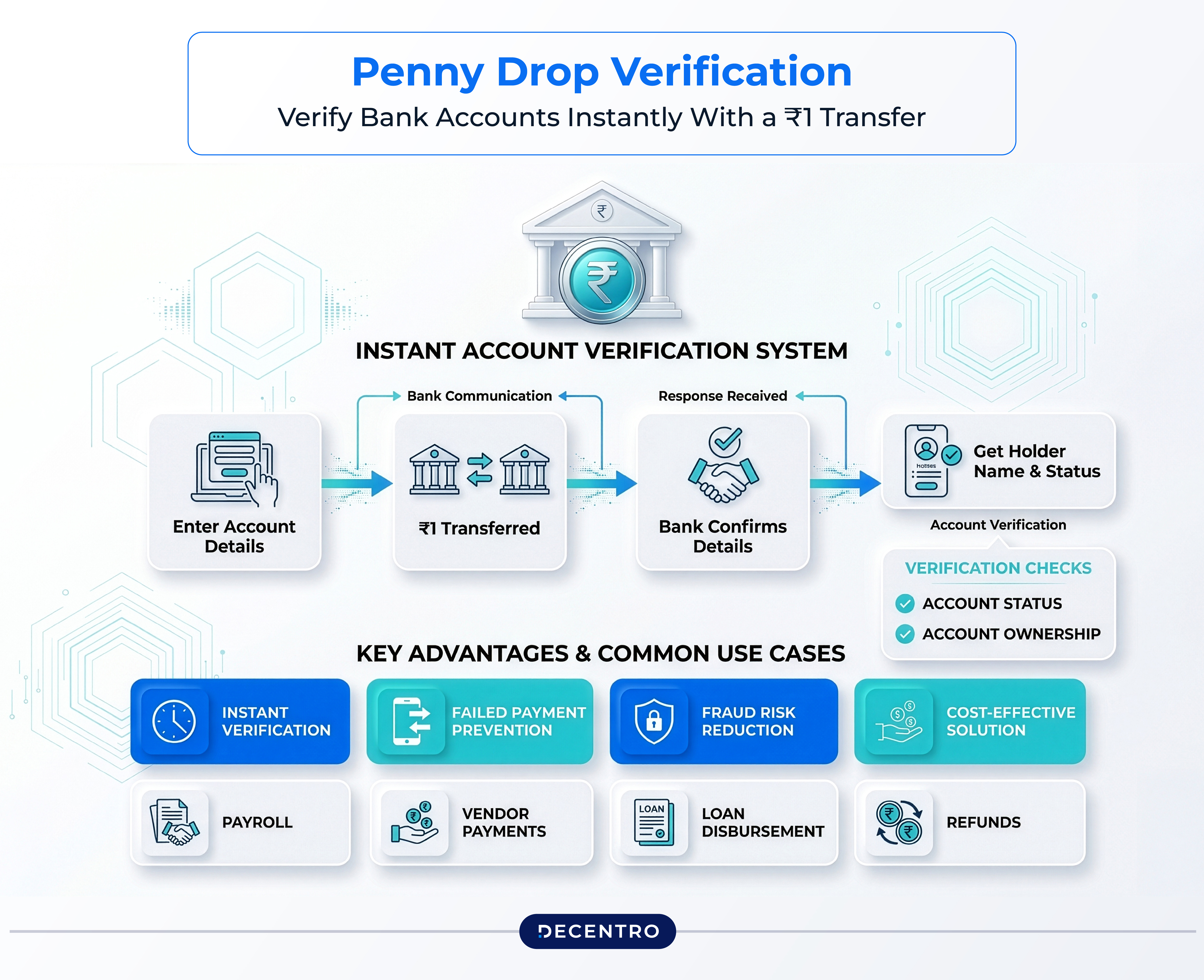

Penny drop verification confirms three things at once:

- The bank account number and IFSC code are valid

- The account is active and capable of receiving funds

- The registered account holder’s name matches the person being onboarded

Unlike manual document checks or database lookups, penny drop gives you a real-time, live confirmation straight from the banking network — not just a record in some registry.

Why Did You Receive ₹1 from Decentro?

Decentro is a banking infrastructure and API platform that enables businesses, lenders, investment apps, payment platforms, and insurers to embed financial services directly into their products.

When you signed up on a financial app (for a loan, investment account, digital wallet, or insurance policy), that platform likely asked for your bank account details. Before they disburse any money to you or link your account, they need to verify it. That app uses Decentro’s Penny Drop Verification API to send ₹1 to your account and confirm the details in real time.

So the ₹1 credit from Decentro in your statement isn’t a mistake — it’s proof the system is working exactly as it should.

What about the ₹0.01 credit?

Some platforms use a sub-rupee micro-deposit (1 paisa) instead of a full rupee for verification. This is functionally identical to a penny drop and is processed the same way through Decentro’s KYC infrastructure.

How Penny Drop Verification Works: Step by Step

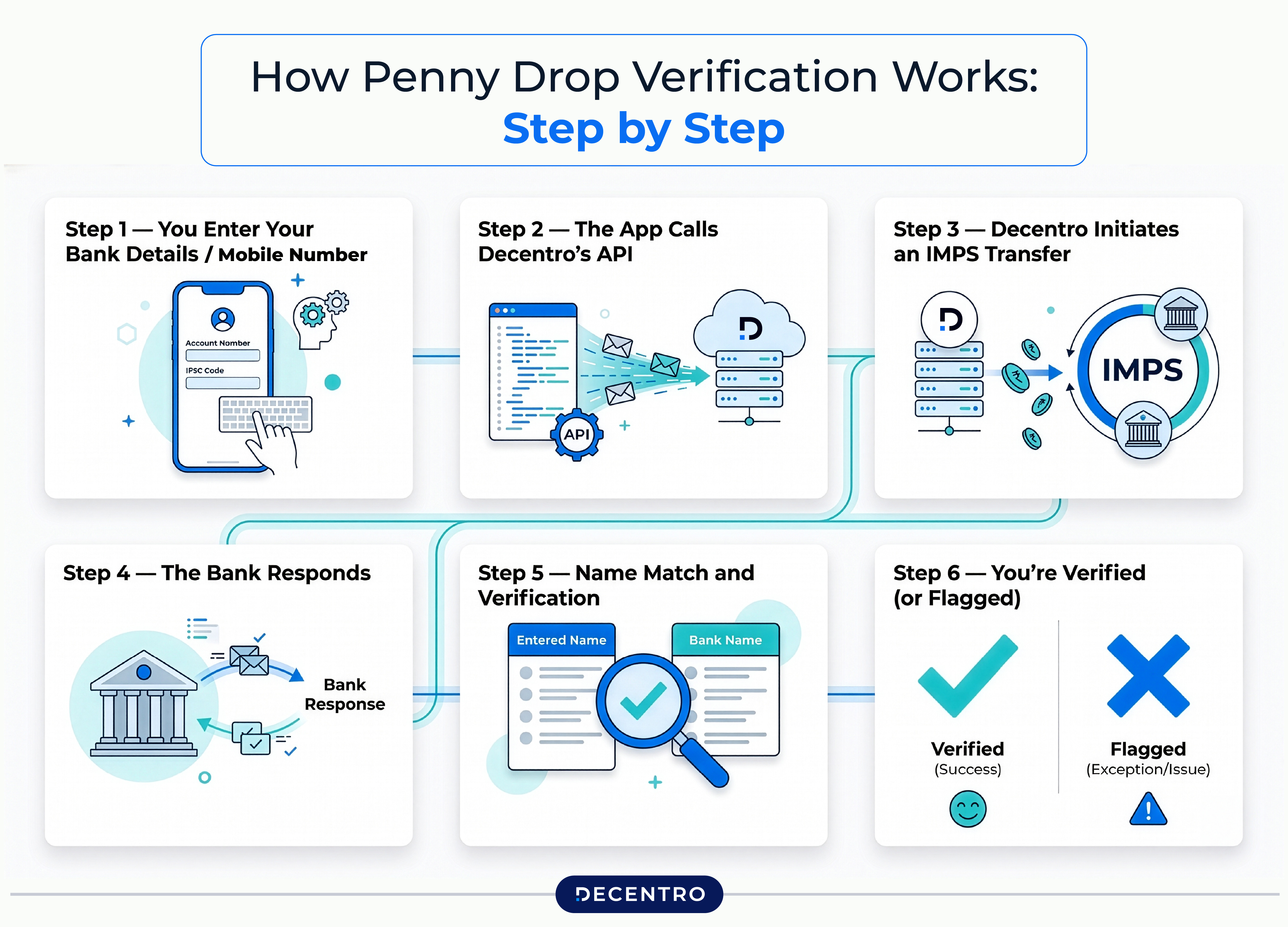

The process is fast, often completing in under 10 seconds. Here’s what happens behind the scenes:

Step 1 — You Enter Your Bank Details/ Mobile Number During onboarding on a financial app, you provide your account number and IFSC code (or link your UPI ID).

Step 2 — The App Calls Decentro’s API The platform sends a verification request to Decentro’s Validate Bank Account API with the account details you provided.

Step 3 — Decentro Initiates an IMPS Transfer Decentro triggers a ₹1 IMPS credit to your bank account. IMPS is used because it works 24/7, including weekends and holidays, and returns structured response data from the bank.

Step 4 — The Bank Responds. Your bank processes the credit and returns key details: account status (active/inactive/frozen/closed), and the registered account holder’s name.

Step 5 — Name Match and Verification Decentro’s system compares the returned name against the name you provided. A proprietary name match score flags close matches, partial matches, or mismatches, giving the platform the signal it needs to approve, flag, or reject the account.

Step 6 — You’re Verified (or Flagged). If everything checks out, your account is verified, and the onboarding flow continues. The ₹1 typically stays in your account; most platforms don’t reverse it.

The entire process, from API call to verified status, usually takes 5–15 seconds.

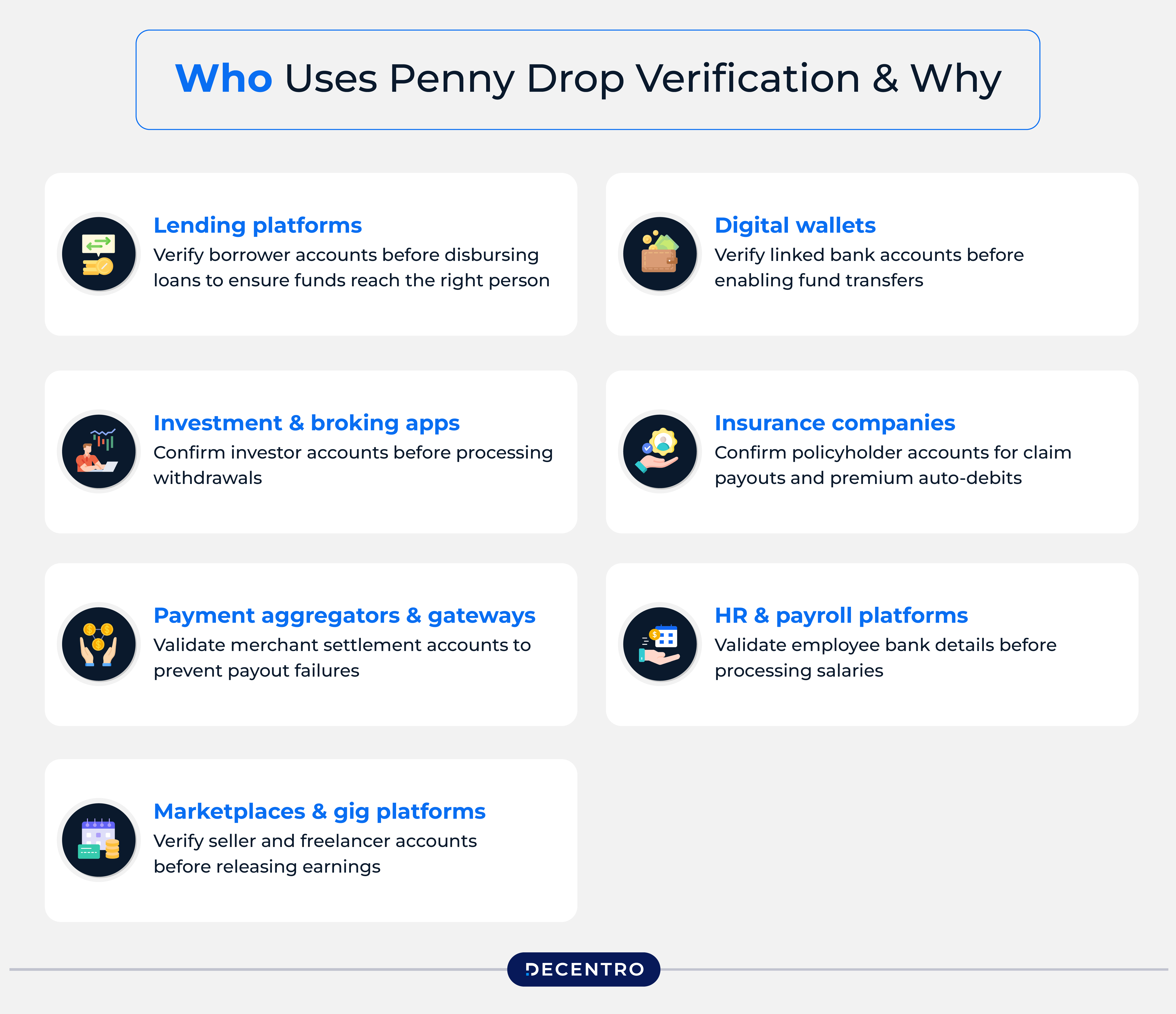

Who Uses Penny Drop Verification — and Why

Penny drop verification is not niche. Across India’s financial ecosystem, it’s used by virtually every category of regulated and digital-first business:

- Lending platforms verify borrower accounts before disbursing loans to ensure funds reach the right person

- Investment and broking apps confirm investor accounts before processing withdrawals

- Payment aggregators and gateways validate merchant settlement accounts to prevent payout failures

- Digital wallets verify linked bank accounts before enabling fund transfers

- Insurance companies confirm policyholder accounts for claim payouts and premium auto-debits

- HR and payroll platforms validate employee bank details before processing salaries

- Marketplaces and gig platforms verify seller and freelancer accounts before releasing earnings

In each case, the core motivation is the same: send money to the right account, the first time, every time.

Is This Legal? And Is Your Data Safe?

Yes — penny drop verification is entirely legal and operates within India’s regulatory framework. Decentro works as a licensed infrastructure provider on behalf of regulated financial institutions. The verification is conducted solely to validate account ownership as part of a KYC or onboarding process.

A few important points:

- You implicitly consented when you provided your bank details on a financial platform and agreed to their terms of service, which typically include a bank account verification step

- No sensitive data is retained beyond what is required for the verification itself

- NPCI and RBI guidelines govern the use of IMPS and bank account verification APIs in India

If you ever receive a ₹1 credit and cannot trace it to a financial platform you recently signed up with, you can email Decentro directly at pgsupport@decentro.tech for clarification.

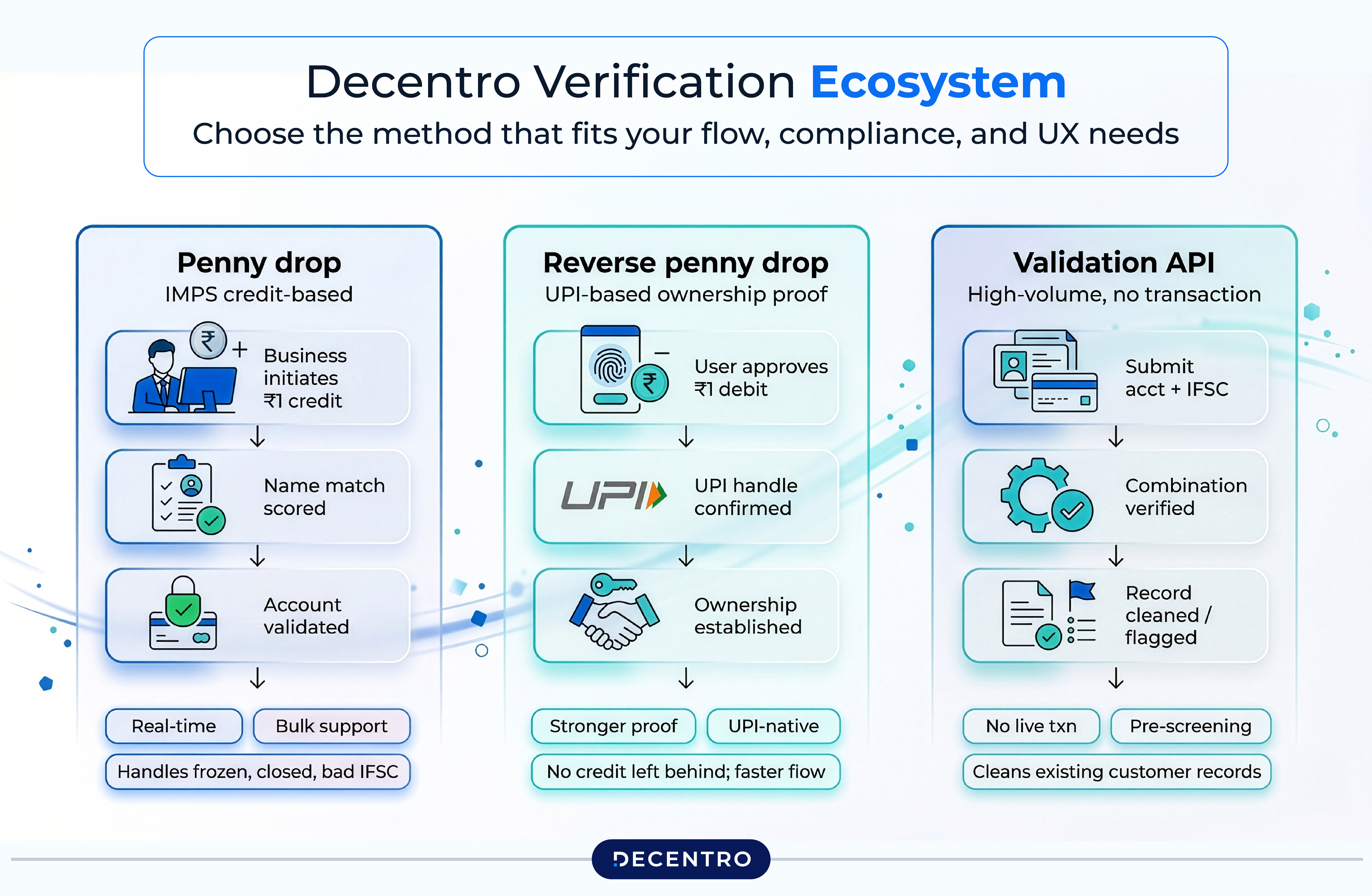

Beyond Penny Drop: Decentro’s Verification Ecosystem

While traditional penny drop remains widely used, the verification landscape is evolving. Decentro offers a broader suite of bank account validation capabilities designed for modern fintech needs:

Penny Drop Verification: The classic method — real-time IMPS-based credit with name match scoring, intelligent failure handling (frozen accounts, closed accounts, incorrect IFSC), and bulk verification support for onboarding at scale.

Reverse Penny Drop (UPI-based): Instead of crediting the account, reverse penny drop asks the user to approve a ₹1 debit from their own UPI-linked account. This confirms not just that the account exists, but that the person initiating verification actually controls the UPI handle, making it a stronger proof of ownership. It’s faster, doesn’t leave a credit behind, and works entirely within the UPI ecosystem.

Bank Account Validation API: For businesses that need to validate account and IFSC combinations at high volume without always triggering a live transaction — useful for pre-screening databases or cleaning up existing customer records.

Together, these tools give businesses flexibility: use the method that best fits your product flow, compliance requirements, and user experience.

Why Penny Testing Matters More Than Ever in Banking

India’s financial landscape is moving toward real-time everything, instant loans, instant payouts, instant settlements. In this environment, the cost of a single failed or fraudulent transaction isn’t just financial; it’s reputational.

For founders and product teams building on financial rails, penny drop verification is a small investment with outsized returns:

- Reduces payout failures caused by incorrect or inactive account details

- Prevents fraud by confirming account ownership before any significant transfer

- Speeds up onboarding by replacing manual document checks with instant API-based verification

- Builds compliance confidence by creating an auditable trail of account verification

In a market where customer trust is hard-won and easily lost, getting the basics right — like knowing that the account you’re paying actually belongs to your customer — is non-negotiable.

Conclusion

That ₹1 credit from Decfin Tech Pvt Ltd in your bank statement is a small number with a big purpose. It represents a real-time, automated check that a business runs to protect you — and themselves — from the risks of financial fraud and misdirected payments.

For consumers, it’s a signal that the platform you signed up with takes verification seriously. For businesses and founders, it’s a reminder that trust in digital finance is built one verified account at a time.

Decentro’s Penny Drop Verification makes this process fast, accurate, and easy to integrate, whether you’re verifying 10 accounts a day or 10 million. As India’s digital economy scales, the infrastructure underneath it needs to be equally reliable.

So for all your verification needs and clarifications, reach out to us.

Frequently Asked Questions (FAQs)

1. I received ₹1 from Decfin Tech Pvt Ltd but haven’t signed up for any financial service recently. Should I be worried?

Not necessarily — but it’s worth checking. Think back to any app where you may have entered your bank details, even casually (a lending app you browsed, a wallet you tested, an investment platform you explored). If you genuinely cannot trace it to any activity, reach out to Decentro at pgsupport@decentro.tech with your account details for clarification. Penny drop credits are always initiated by a business that collected your account details, not randomly.

2. Will the ₹1 be debited from my account later?

No. The ₹1 credited to your account as part of penny drop verification is yours to keep. Most platforms do not reverse the micro-deposit after verification is complete.

3. Is penny drop verification the same as UPI penny drop or reverse penny drop?

They are related but different. Traditional penny drop sends a small credit via IMPS to your account. Reverse penny drop asks you to approve a small UPI debit from your account, which more actively confirms you control the account. UPI penny drop uses the UPI rails for the credit rather than IMPS. Decentro supports all three methods depending on the business’s use case.

4. Can a business verify my bank account without my knowledge?

Technically, a penny drop only requires your mobile number/account number and IFSC code — details you would have provided during signup. By sharing those details and agreeing to a platform’s terms of service (which typically include account verification), you have given implicit consent. Businesses are not permitted to verify strangers’ accounts without any prior interaction randomly.

5. I’m building a fintech product. How quickly can I integrate Decentro’s Penny Drop APIs?

Decentro’s APIs are designed for developer-first integration. Most teams complete a basic penny drop integration within a few hours using Decentro’s documentation and sandbox environment. For high-volume or enterprise use cases, Decentro also provides bulk verification, intelligent routing, and failure-reason analysis out of the box. Visit decentro.tech to explore the API documentation and request sandbox access.